There's Reason For Concern Over Shenzhen Pagoda Industrial (Group) Corporation Limited's (HKG:2411) Massive 33% Price Jump

Shenzhen Pagoda Industrial (Group) Corporation Limited (HKG:2411) shares have had a really impressive month, gaining 33% after a shaky period beforehand. But the gains over the last month weren't enough to make shareholders whole, as the share price is still down 5.5% in the last twelve months.

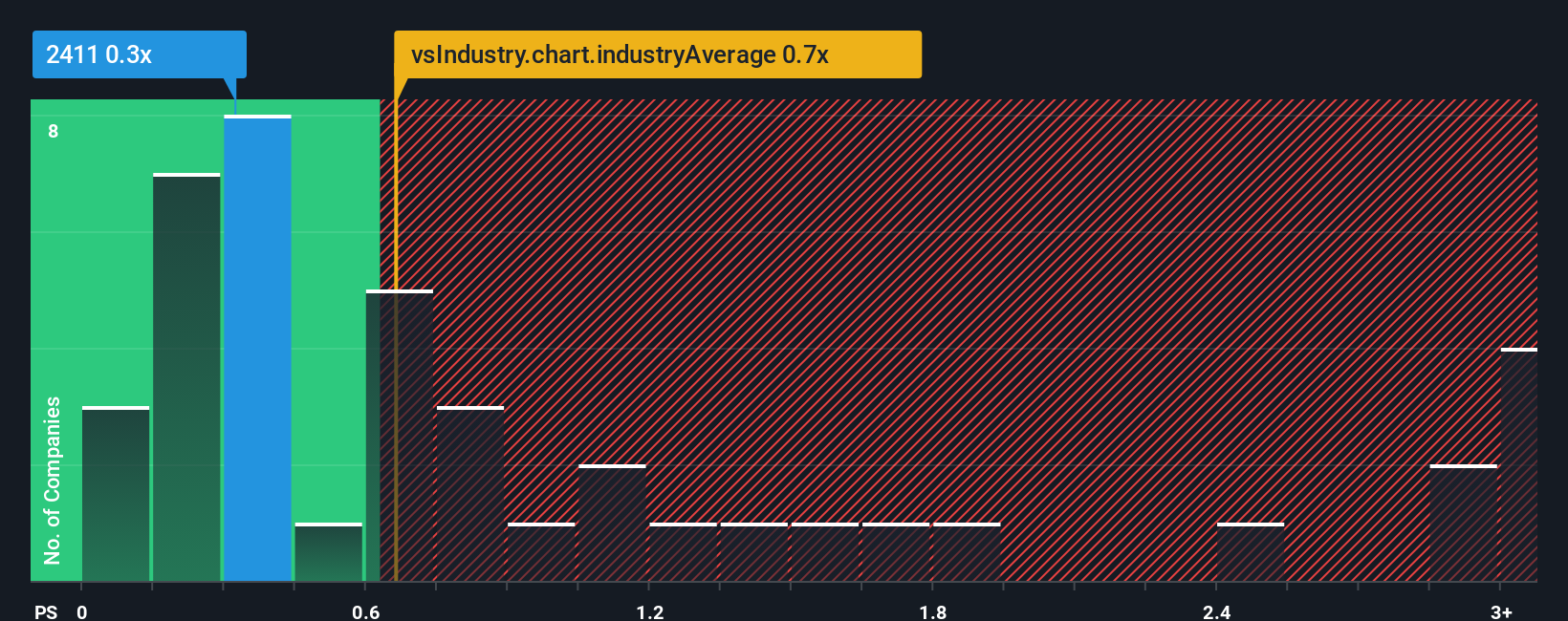

Although its price has surged higher, it's still not a stretch to say that Shenzhen Pagoda Industrial (Group)'s price-to-sales (or "P/S") ratio of 0.3x right now seems quite "middle-of-the-road" compared to the Consumer Retailing industry in Hong Kong, where the median P/S ratio is around 0.7x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/S.

See our latest analysis for Shenzhen Pagoda Industrial (Group)

What Does Shenzhen Pagoda Industrial (Group)'s Recent Performance Look Like?

Shenzhen Pagoda Industrial (Group) could be doing better as its revenue has been going backwards lately while most other companies have been seeing positive revenue growth. It might be that many expect the dour revenue performance to strengthen positively, which has kept the P/S from falling. However, if this isn't the case, investors might get caught out paying too much for the stock.

Want the full picture on analyst estimates for the company? Then our free report on Shenzhen Pagoda Industrial (Group) will help you uncover what's on the horizon.How Is Shenzhen Pagoda Industrial (Group)'s Revenue Growth Trending?

Shenzhen Pagoda Industrial (Group)'s P/S ratio would be typical for a company that's only expected to deliver moderate growth, and importantly, perform in line with the industry.

Taking a look back first, the company's revenue growth last year wasn't something to get excited about as it posted a disappointing decline of 15%. This means it has also seen a slide in revenue over the longer-term as revenue is down 15% in total over the last three years. Therefore, it's fair to say the revenue growth recently has been undesirable for the company.

Shifting to the future, estimates from the dual analysts covering the company suggest revenue should grow by 8.9% over the next year. With the industry predicted to deliver 15% growth, the company is positioned for a weaker revenue result.

In light of this, it's curious that Shenzhen Pagoda Industrial (Group)'s P/S sits in line with the majority of other companies. It seems most investors are ignoring the fairly limited growth expectations and are willing to pay up for exposure to the stock. These shareholders may be setting themselves up for future disappointment if the P/S falls to levels more in line with the growth outlook.

What Does Shenzhen Pagoda Industrial (Group)'s P/S Mean For Investors?

Shenzhen Pagoda Industrial (Group)'s stock has a lot of momentum behind it lately, which has brought its P/S level with the rest of the industry. It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

Our look at the analysts forecasts of Shenzhen Pagoda Industrial (Group)'s revenue prospects has shown that its inferior revenue outlook isn't negatively impacting its P/S as much as we would have predicted. At present, we aren't confident in the P/S as the predicted future revenues aren't likely to support a more positive sentiment for long. Circumstances like this present a risk to current and prospective investors who may see share prices fall if the low revenue growth impacts the sentiment.

The company's balance sheet is another key area for risk analysis. Take a look at our free balance sheet analysis for Shenzhen Pagoda Industrial (Group) with six simple checks on some of these key factors.

If you're unsure about the strength of Shenzhen Pagoda Industrial (Group)'s business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Contact Us

Contact Number : +852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English