How Investors Are Reacting To Clover Health (CLOV) First-Ever GAAP Profit And Tech-Driven Efficiency Gains

- Clover Health Investments recently reported its first-ever positive GAAP net income alongside strong Q1 2026 results, supported by rapid Medicare Advantage membership growth and disciplined cost management.

- The company also highlighted the growing impact of its Clover Assistant technology, with sustained improvements in medical cost ratios as member cohorts mature, underscoring the role of its software platform in driving operating performance.

- Next, we will examine how this milestone of positive GAAP profitability and technology-driven efficiency gains may reshape Clover Health’s investment narrative.

Capitalize on the AI infrastructure supercycle with our selection of the 46 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

Clover Health Investments Investment Narrative Recap

To own Clover Health, you need to believe its Medicare Advantage engine and Clover Assistant software can keep improving medical cost ratios enough to support sustainable profitability. The first-ever positive GAAP net income in Q1 2026 strengthens that case and directly addresses the previous concern around ongoing GAAP losses, while elevated utilization and reimbursement changes still look like the most important near term risk to the story.

Among recent developments, the Q1 2026 update on Clover Assistant’s impact is especially relevant: management cited medical cost ratio improvements of about 8% after one year of use, widening toward roughly 20% by year four. If those cohort trends persist at scale, they could be a key counterweight to rising medical and pharmacy costs and a meaningful driver of margin resilience around future Medicare rate shifts.

Yet even with this progress, investors should still pay close attention to the risk that elevated medical and pharmacy utilization could...

Read the full narrative on Clover Health Investments (it's free!)

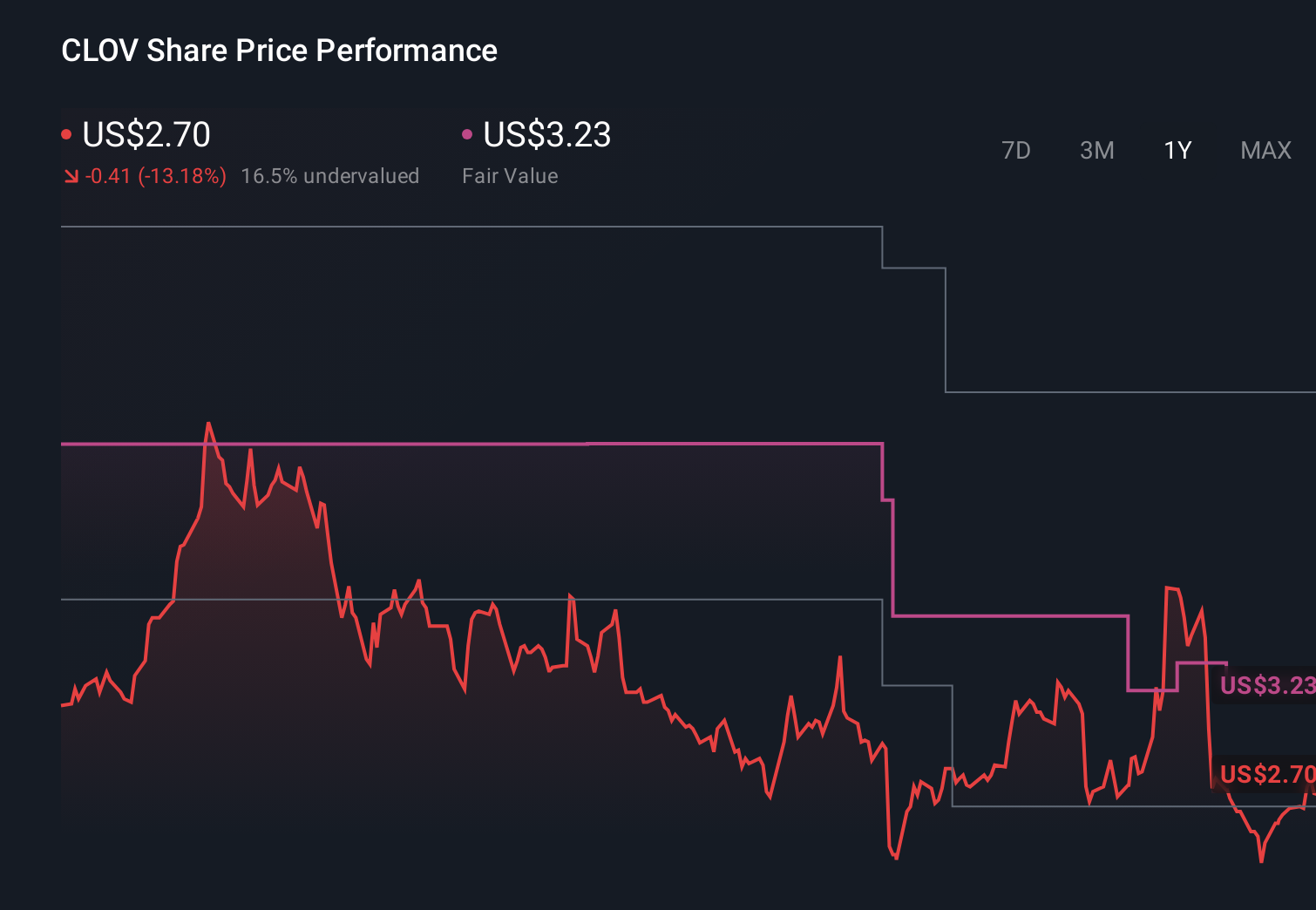

Clover Health Investments' narrative projects $3.7 billion revenue and $31.7 million earnings by 2029. This requires 24.4% yearly revenue growth and a $117.2 million earnings increase from -$85.5 million today.

Uncover how Clover Health Investments' forecasts yield a $2.82 fair value, a 22% downside to its current price.

Exploring Other Perspectives

Some of the lowest estimate analysts saw a tougher road ahead, assuming revenue of about US$2.8 billion by 2028 and questioning profitability, so if you are encouraged by Q1 2026’s positive GAAP net income, it is worth weighing how that might challenge views that rising medical costs and dependence on membership growth would keep Clover reliant on external funding and pressure future margins.

Explore 6 other fair value estimates on Clover Health Investments - why the stock might be worth over 9x more than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Clover Health Investments research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Clover Health Investments research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Clover Health Investments' overall financial health at a glance.

Looking For Alternative Opportunities?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- We've uncovered the 10 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English