Read This Before Considering Nu Skin Enterprises, Inc. (NYSE:NUS) For Its Upcoming US$0.06 Dividend

Some investors rely on dividends for growing their wealth, and if you're one of those dividend sleuths, you might be intrigued to know that Nu Skin Enterprises, Inc. (NYSE:NUS) is about to go ex-dividend in just 4 days. The ex-dividend date occurs one day before the record date, which is the day on which shareholders need to be on the company's books in order to receive a dividend. The ex-dividend date is of consequence because whenever a stock is bought or sold, the trade takes at least one business day to settle. In other words, investors can purchase Nu Skin Enterprises' shares before the 29th of May in order to be eligible for the dividend, which will be paid on the 10th of June.

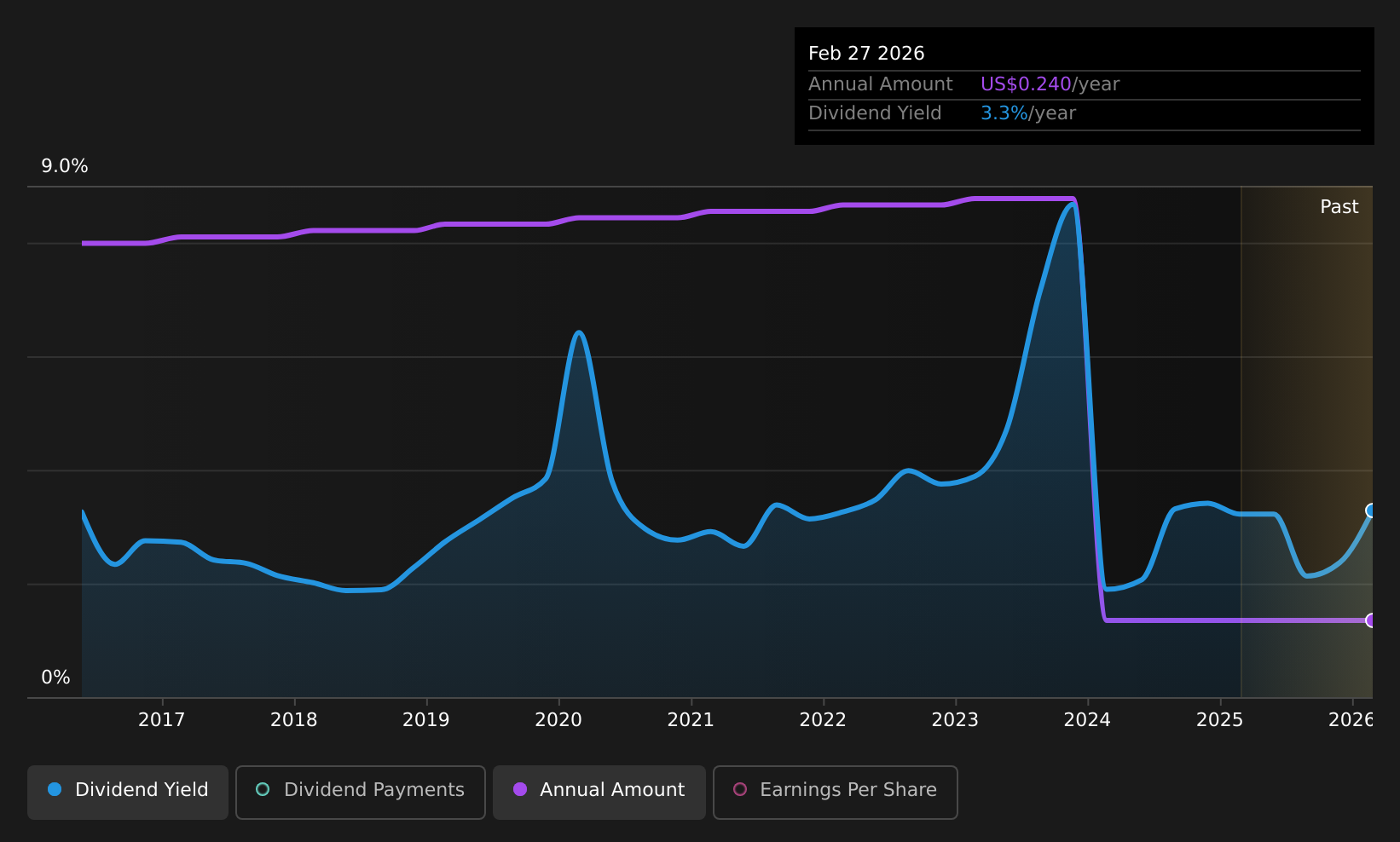

The company's upcoming dividend is US$0.06 a share, following on from the last 12 months, when the company distributed a total of US$0.24 per share to shareholders. Calculating the last year's worth of payments shows that Nu Skin Enterprises has a trailing yield of 4.0% on the current share price of US$5.93. Dividends are an important source of income to many shareholders, but the health of the business is crucial to maintaining those dividends. So we need to investigate whether Nu Skin Enterprises can afford its dividend, and if the dividend could grow.

Dividends are typically paid out of company income, so if a company pays out more than it earned, its dividend is usually at a higher risk of being cut. Nu Skin Enterprises paid out just 22% of its profit last year, which we think is conservatively low and leaves plenty of margin for unexpected circumstances. A useful secondary check can be to evaluate whether Nu Skin Enterprises generated enough free cash flow to afford its dividend. Thankfully its dividend payments took up just 28% of the free cash flow it generated, which is a comfortable payout ratio.

It's positive to see that Nu Skin Enterprises's dividend is covered by both profits and cash flow, since this is generally a sign that the dividend is sustainable, and a lower payout ratio usually suggests a greater margin of safety before the dividend gets cut.

View our latest analysis for Nu Skin Enterprises

Click here to see how much of its profit Nu Skin Enterprises paid out over the last 12 months.

Have Earnings And Dividends Been Growing?

When earnings decline, dividend companies become much harder to analyse and own safely. If earnings decline and the company is forced to cut its dividend, investors could watch the value of their investment go up in smoke. Readers will understand then, why we're concerned to see Nu Skin Enterprises's earnings per share have dropped 21% a year over the past five years. Ultimately, when earnings per share decline, the size of the pie from which dividends can be paid, shrinks.

The main way most investors will assess a company's dividend prospects is by checking the historical rate of dividend growth. Nu Skin Enterprises has seen its dividend decline 16% per annum on average over the past 10 years, which is not great to see. While it's not great that earnings and dividends per share have fallen in recent years, we're encouraged by the fact that management has trimmed the dividend rather than risk over-committing the company in a risky attempt to maintain yields to shareholders.

Final Takeaway

Should investors buy Nu Skin Enterprises for the upcoming dividend? Earnings per share are down meaningfully, although at least the company is paying out a low and conservative percentage of both its earnings and cash flow. It's definitely not great to see earnings falling, but at least there may be some buffer before the dividend needs to be cut. Overall, it's hard to get excited about Nu Skin Enterprises from a dividend perspective.

So while Nu Skin Enterprises looks good from a dividend perspective, it's always worthwhile being up to date with the risks involved in this stock. Our analysis shows 2 warning signs for Nu Skin Enterprises and you should be aware of them before buying any shares.

If you're in the market for strong dividend payers, we recommend checking our selection of top dividend stocks.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English