3 Stocks Estimated To Be Trading At Discounts Ranging From 24% To 49.9%

The United States market has shown robust performance, rising 1.6% over the last week and surging 28% over the past year, with earnings forecasted to grow by 17% annually. In this environment, identifying stocks trading at significant discounts can offer potential opportunities for investors looking to capitalize on undervaluation relative to market growth expectations.

Top 10 Undervalued Stocks Based On Cash Flows In The United States

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Robert Half (RHI) | $29.44 | $58.73 | 49.9% |

| Rayonier (RYN) | $20.89 | $40.26 | 48.1% |

| Merck (MRK) | $118.72 | $228.62 | 48.1% |

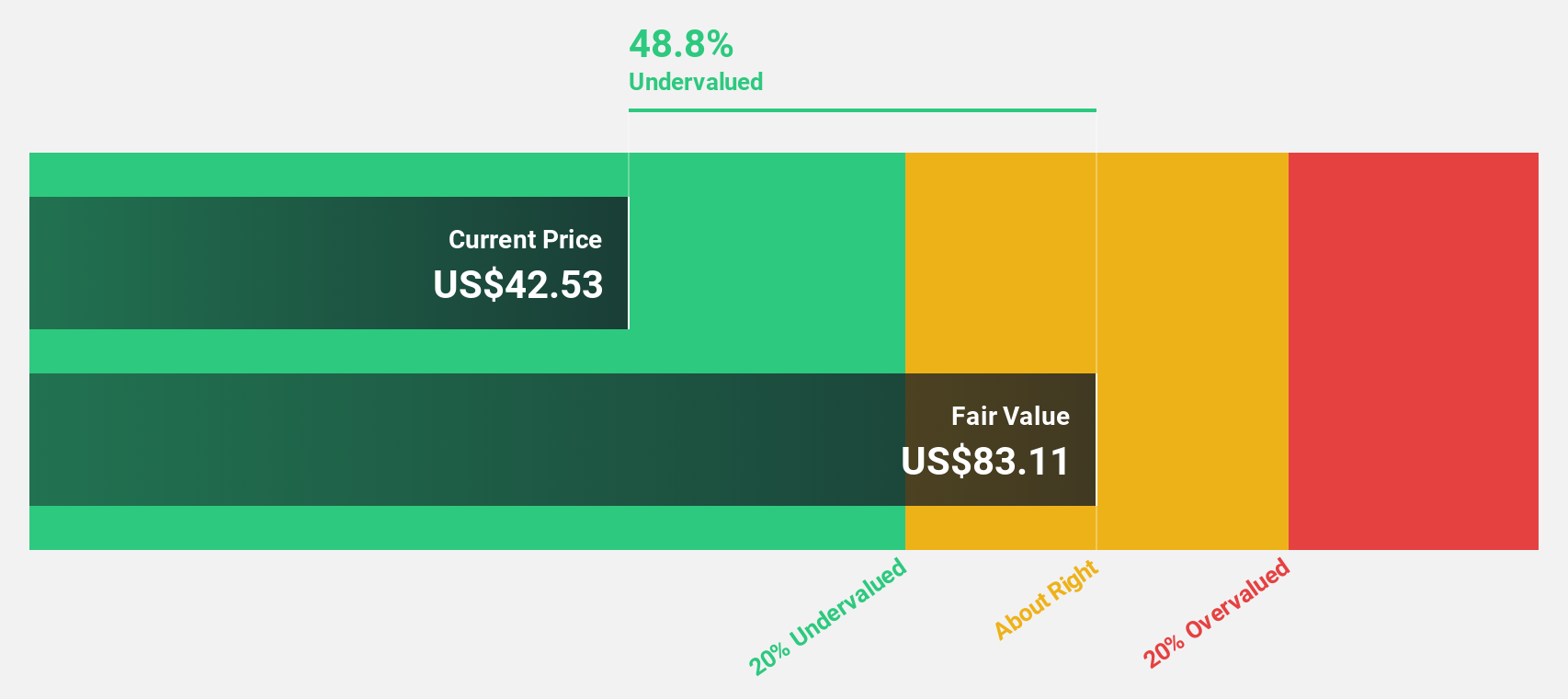

| Live Oak Bancshares (LOB) | $38.03 | $74.21 | 48.8% |

| Goosehead Insurance (GSHD) | $34.39 | $66.13 | 48% |

| Gilead Sciences (GILD) | $134.43 | $266.16 | 49.5% |

| FB Financial (FBK) | $52.69 | $101.61 | 48.1% |

| CoStar Group (CSGP) | $32.20 | $61.96 | 48% |

| Capstone Energy+ (CGEH) | $13.55 | $26.05 | 48% |

| Bowhead Specialty Holdings (BOW) | $26.62 | $52.60 | 49.4% |

We're going to check out a few of the best picks from our screener tool.

AvePoint (AVPT)

Overview: AvePoint, Inc. offers a cloud-native data management software platform across various regions including North America, Europe, the Middle East, Africa, and the Asia Pacific with a market cap of $2.31 billion.

Operations: The company's revenue is primarily derived from its Software & Programming segment, which generated $443.68 million.

Estimated Discount To Fair Value: 41%

AvePoint's current trading price of US$10.91 is significantly below its estimated future cash flow value of US$18.49, suggesting it is undervalued based on discounted cash flow analysis. The company has demonstrated strong earnings growth, with Q1 2026 net income rising to US$15.25 million from US$3.44 million a year earlier, and revenue guidance for 2026 indicates a 22% increase at the midpoint, bolstered by recent product advancements and strategic buybacks enhancing shareholder value.

- In light of our recent growth report, it seems possible that AvePoint's financial performance will exceed current levels.

- Take a closer look at AvePoint's balance sheet health here in our report.

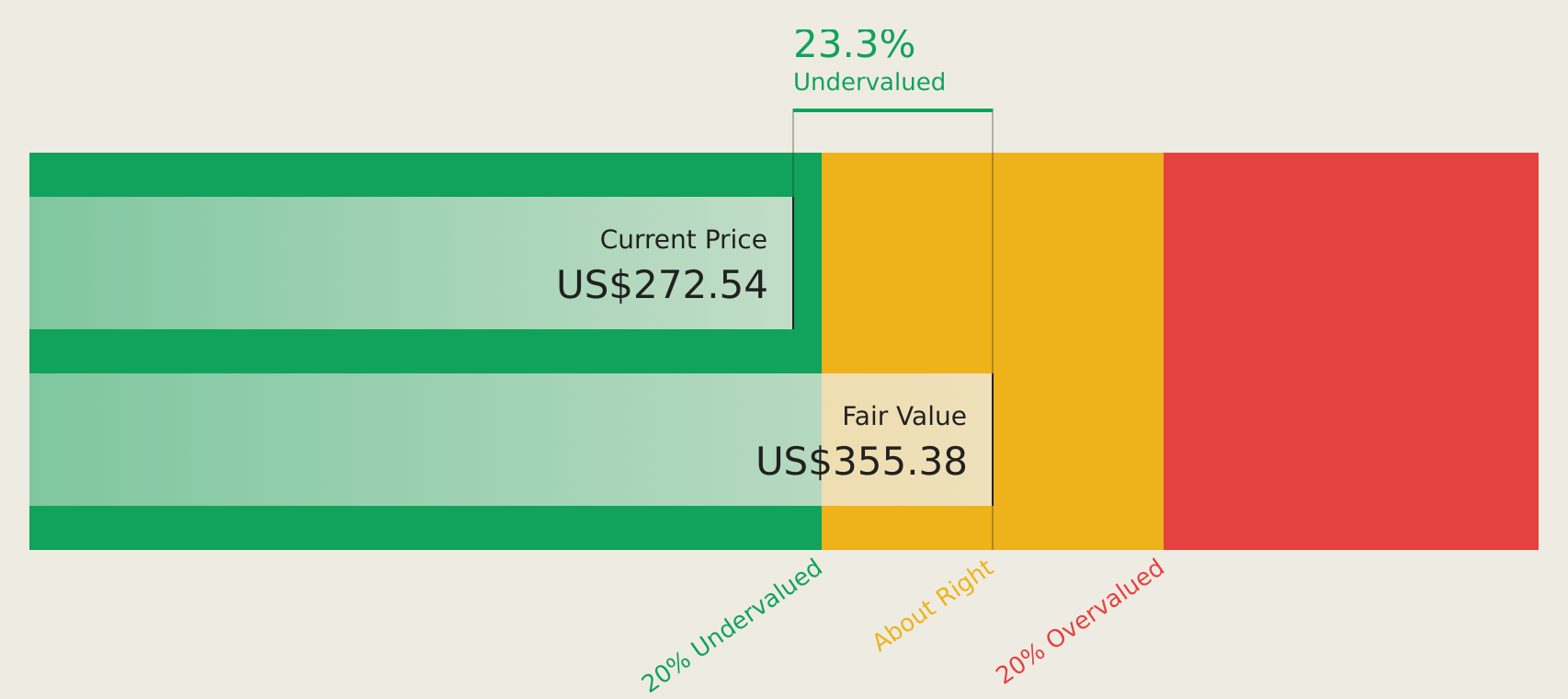

FTAI Aviation (FTAI)

Overview: FTAI Aviation Ltd. operates by owning, acquiring, and selling aviation equipment for global transportation, with a market cap of $26.71 billion.

Operations: The company's revenue is primarily derived from two segments: Aviation Leasing, which contributes $521.03 million, and Aerospace Products, which generates $2.31 billion.

Estimated Discount To Fair Value: 24%

FTAI Aviation's trading price of US$260.34 is below its estimated future cash flow value of US$342.45, indicating undervaluation based on discounted cash flow analysis. The company has reported a substantial increase in net income to US$137.9 million from the previous year's US$102.39 million, alongside a significant revenue boost to US$830.7 million from US$502.08 million, driven by strategic debt refinancing and preferred stock buybacks enhancing financial flexibility and growth potential despite insider selling concerns.

- Upon reviewing our latest growth report, FTAI Aviation's projected financial performance appears quite optimistic.

- Dive into the specifics of FTAI Aviation here with our thorough financial health report.

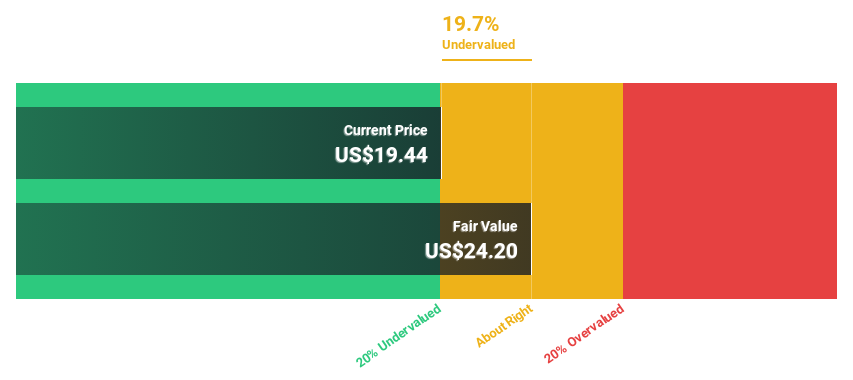

Robert Half (RHI)

Overview: Robert Half Inc. offers talent solutions and business consulting services both in the United States and internationally, with a market cap of approximately $2.96 billion.

Operations: Robert Half's revenue is primarily derived from its Contract Talent Solutions segment at $3.44 billion, followed by Protiviti at $1.94 billion, and Permanent Placement Talent Solutions at $436.41 million.

Estimated Discount To Fair Value: 49.9%

Robert Half is trading at US$29.44, significantly below its estimated future cash flow value of US$58.73, highlighting potential undervaluation based on discounted cash flow analysis. Despite a recent decline in profit margins to 2.4% from 3.6% last year and a quarterly net income drop to US$13.79 million, earnings are forecasted to grow substantially at 25.7% annually over the next three years, outpacing the broader U.S. market's growth expectations.

- Our comprehensive growth report raises the possibility that Robert Half is poised for substantial financial growth.

- Click here to discover the nuances of Robert Half with our detailed financial health report.

Summing It All Up

- Investigate our full lineup of 137 Undervalued US Stocks Based On Cash Flows right here.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English