The Beauty Farm Medical and Health Industry Inc. (HKG:2373) Full-Year Results Are Out And Analysts Have Published New Forecasts

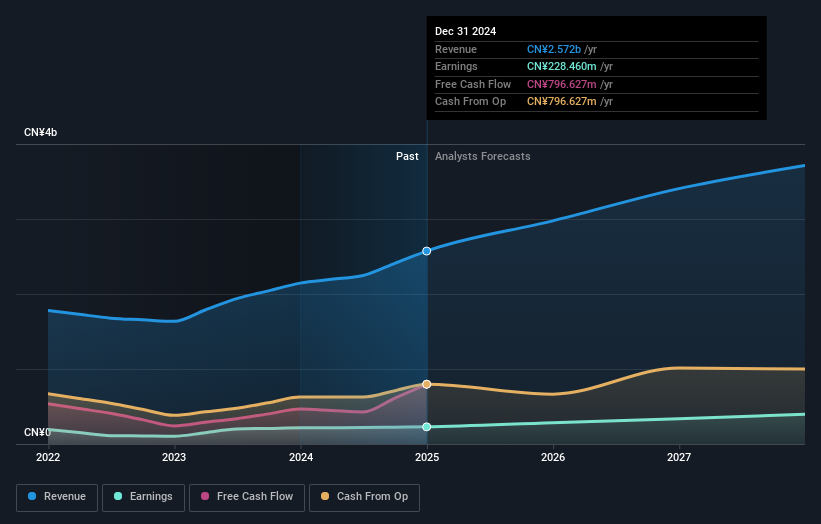

Shareholders might have noticed that Beauty Farm Medical and Health Industry Inc. (HKG:2373) filed its yearly result this time last week. The early response was not positive, with shares down 2.3% to HK$17.98 in the past week. It looks like the results were a bit of a negative overall. While revenues of CN¥2.6b were in line with analyst predictions, statutory earnings were less than expected, missing estimates by 3.6% to hit CN¥0.99 per share. Earnings are an important time for investors, as they can track a company's performance, look at what the analysts are forecasting for next year, and see if there's been a change in sentiment towards the company. With this in mind, we've gathered the latest statutory forecasts to see what the analysts are expecting for next year.

Taking into account the latest results, the current consensus from Beauty Farm Medical and Health Industry's four analysts is for revenues of CN¥2.98b in 2025. This would reflect a solid 16% increase on its revenue over the past 12 months. Statutory earnings per share are predicted to jump 26% to CN¥1.22. Yet prior to the latest earnings, the analysts had been anticipated revenues of CN¥3.12b and earnings per share (EPS) of CN¥1.26 in 2025. It's pretty clear that pessimism has reared its head after the latest results, leading to a weaker revenue outlook and a small dip in earnings per share estimates.

View our latest analysis for Beauty Farm Medical and Health Industry

The analysts made no major changes to their price target of HK$20.94, suggesting the downgrades are not expected to have a long-term impact on Beauty Farm Medical and Health Industry's valuation. Fixating on a single price target can be unwise though, since the consensus target is effectively the average of analyst price targets. As a result, some investors like to look at the range of estimates to see if there are any diverging opinions on the company's valuation. There are some variant perceptions on Beauty Farm Medical and Health Industry, with the most bullish analyst valuing it at HK$21.91 and the most bearish at HK$19.98 per share. Still, with such a tight range of estimates, it suggeststhe analysts have a pretty good idea of what they think the company is worth.

Another way we can view these estimates is in the context of the bigger picture, such as how the forecasts stack up against past performance, and whether forecasts are more or less bullish relative to other companies in the industry. The analysts are definitely expecting Beauty Farm Medical and Health Industry's growth to accelerate, with the forecast 16% annualised growth to the end of 2025 ranking favourably alongside historical growth of 12% per annum over the past five years. Compare this with other companies in the same industry, which are forecast to grow their revenue 10% annually. Factoring in the forecast acceleration in revenue, it's pretty clear that Beauty Farm Medical and Health Industry is expected to grow much faster than its industry.

The Bottom Line

The most important thing to take away is that the analysts downgraded their earnings per share estimates, showing that there has been a clear decline in sentiment following these results. They also downgraded Beauty Farm Medical and Health Industry's revenue estimates, but industry data suggests that it is expected to grow faster than the wider industry. The consensus price target held steady at HK$20.94, with the latest estimates not enough to have an impact on their price targets.

With that in mind, we wouldn't be too quick to come to a conclusion on Beauty Farm Medical and Health Industry. Long-term earnings power is much more important than next year's profits. We have estimates - from multiple Beauty Farm Medical and Health Industry analysts - going out to 2027, and you can see them free on our platform here.

Another thing to consider is whether management and directors have been buying or selling stock recently. We provide an overview of all open market stock trades for the last twelve months on our platform, here.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

① During the campaign period, US stocks, US stocks short selling, US stock options, Hong Kong stocks, and A-shares trading will maintain at $0 commission, and no subscription/redemption fees for mutual fund transactions. $0 fee offer has a time limit, until further notice. For more information, please visit: https://www.webull.hk/pricing

Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English