Brokers Are Upgrading Their Views On Pop Mart International Group Limited (HKG:9992) With These New Forecasts

Pop Mart International Group Limited (HKG:9992) shareholders will have a reason to smile today, with the analysts making substantial upgrades to this year's forecasts. The analysts greatly increased their revenue estimates, suggesting a stark improvement in business fundamentals. Investors have been pretty optimistic on Pop Mart International Group too, with the stock up 16% to HK$157 over the past week. It will be interesting to see if today's upgrade is enough to propel the stock even higher.

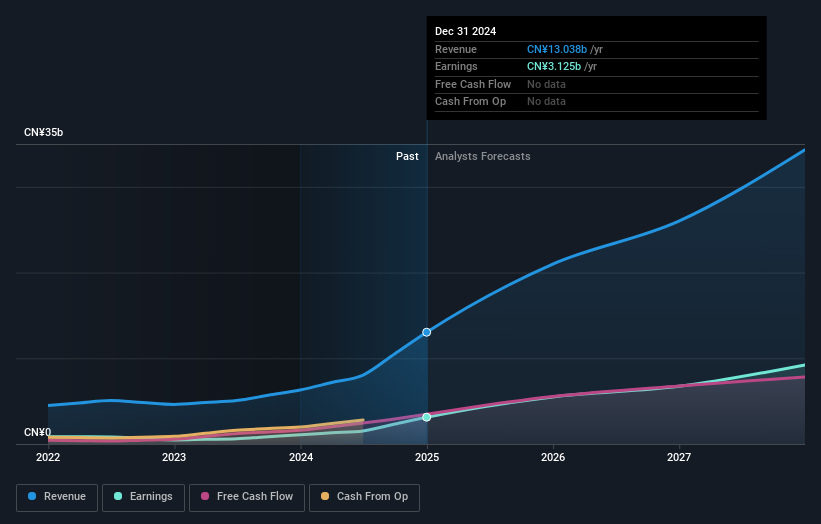

Following the upgrade, the current consensus from Pop Mart International Group's 23 analysts is for revenues of CN¥21b in 2025 which - if met - would reflect a huge 61% increase on its sales over the past 12 months. Per-share earnings are expected to bounce 72% to CN¥4.05. Previously, the analysts had been modelling revenues of CN¥17b and earnings per share (EPS) of CN¥2.93 in 2025. So we can see there's been a pretty clear increase in analyst sentiment in recent times, with both revenues and earnings per share receiving a decent lift in the latest estimates.

See our latest analysis for Pop Mart International Group

With these upgrades, we're not surprised to see that the analysts have lifted their price target 53% to CN¥159 per share. There's another way to think about price targets though, and that's to look at the range of price targets put forward by analysts, because a wide range of estimates could suggest a diverse view on possible outcomes for the business. Currently, the most bullish analyst values Pop Mart International Group at CN¥208 per share, while the most bearish prices it at CN¥103. Note the wide gap in analyst price targets? This implies to us that there is a fairly broad range of possible scenarios for the underlying business.

Taking a look at the bigger picture now, one of the ways we can understand these forecasts is to see how they compare to both past performance and industry growth estimates. It's clear from the latest estimates that Pop Mart International Group's rate of growth is expected to accelerate meaningfully, with the forecast 61% annualised revenue growth to the end of 2025 noticeably faster than its historical growth of 33% p.a. over the past five years. Compare this with other companies in the same industry, which are forecast to grow their revenue 16% annually. Factoring in the forecast acceleration in revenue, it's pretty clear that Pop Mart International Group is expected to grow much faster than its industry.

The Bottom Line

The most important thing to take away from this upgrade is that analysts upgraded their earnings per share estimates for this year, expecting improving business conditions. They also upgraded their revenue estimates for this year, and sales are expected to grow faster than the wider market. With a serious upgrade to expectations and a rising price target, it might be time to take another look at Pop Mart International Group.

Still, the long-term prospects of the business are much more relevant than next year's earnings. At Simply Wall St, we have a full range of analyst estimates for Pop Mart International Group going out to 2027, and you can see them free on our platform here..

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies backed by insiders.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

① During the campaign period, US stocks, US stocks short selling, US stock options, Hong Kong stocks, and A-shares trading will maintain at $0 commission, and no subscription/redemption fees for mutual fund transactions. $0 fee offer has a time limit, until further notice. For more information, please visit: https://www.webull.hk/pricing

Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English