Lakeland Financial Director Acquires 13% More Stock

Investors who take an interest in Lakeland Financial Corporation (NASDAQ:LKFN) should definitely note that the Director, Mindy Truex, recently paid US$60.11 per share to buy US$499k worth of the stock. That's a very decent purchase to our minds and it grew their holding by a solid 13%.

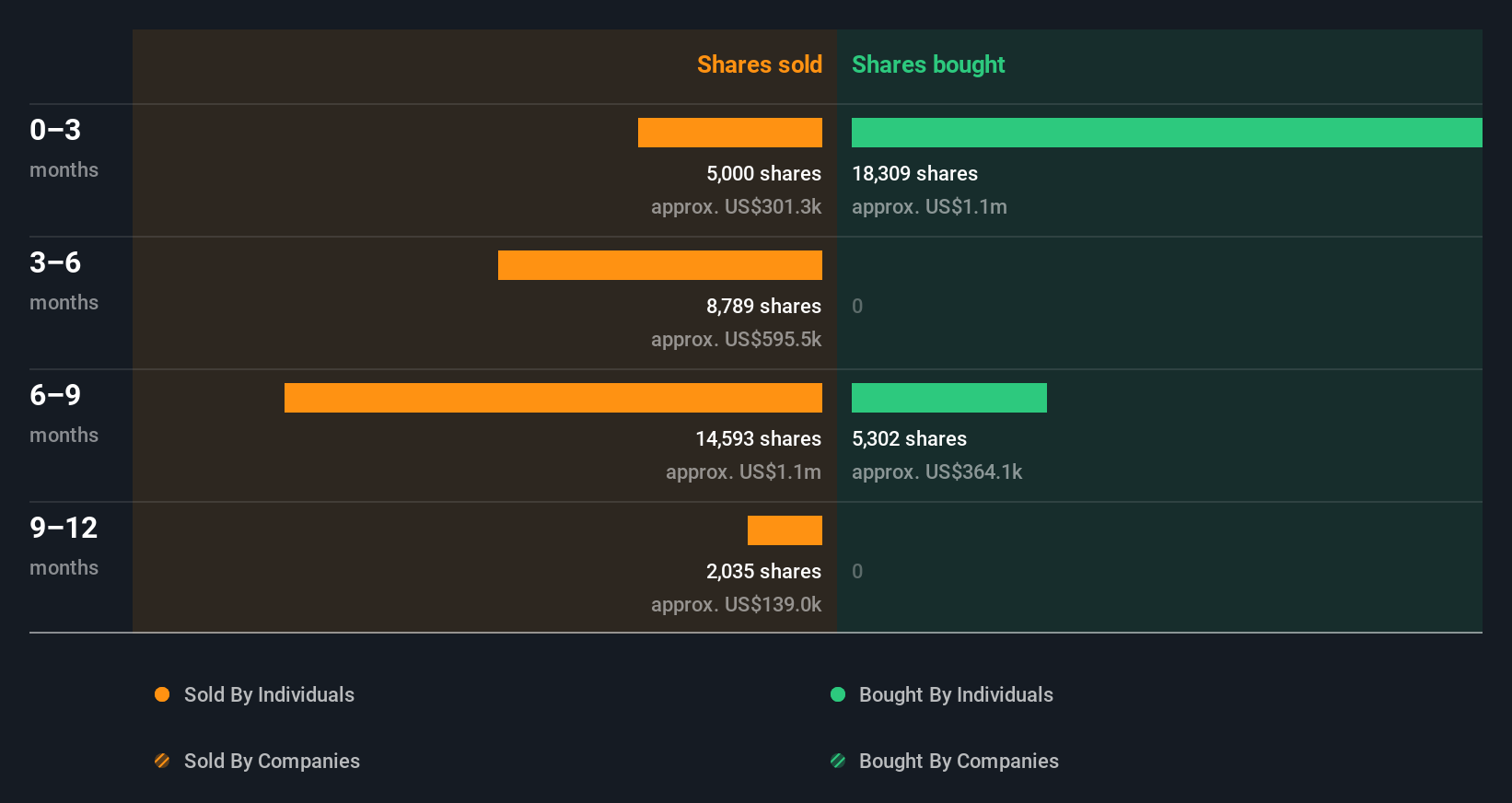

The Last 12 Months Of Insider Transactions At Lakeland Financial

Over the last year, we can see that the biggest insider sale was by the Chairman & CEO, David Findlay, for US$728k worth of shares, at about US$75.51 per share. While insider selling is a negative, to us, it is more negative if the shares are sold at a lower price. It's of some comfort that this sale was conducted at a price well above the current share price, which is US$59.99. So it may not tell us anything about how insiders feel about the current share price.

Over the last year, we can see that insiders have bought 23.61k shares worth US$1.5m. On the other hand they divested 30.42k shares, for US$2.1m. Over the last year we saw more insider selling of Lakeland Financial shares, than buying. You can see a visual depiction of insider transactions (by companies and individuals) over the last 12 months, below. By clicking on the graph below, you can see the precise details of each insider transaction!

Check out our latest analysis for Lakeland Financial

For those who like to find hidden gems this free list of small cap companies with recent insider purchasing, could be just the ticket.

Does Lakeland Financial Boast High Insider Ownership?

For a common shareholder, it is worth checking how many shares are held by company insiders. A high insider ownership often makes company leadership more mindful of shareholder interests. Insiders own 2.8% of Lakeland Financial shares, worth about US$42m. While this is a strong but not outstanding level of insider ownership, it's enough to indicate some alignment between management and smaller shareholders.

What Might The Insider Transactions At Lakeland Financial Tell Us?

The recent insider purchases are heartening. However, the longer term transactions are not so encouraging. We don't take much heart from transactions by Lakeland Financial insiders over the last year. But they own a reasonable amount of the company, and there was some buying recently. So they seem pretty well aligned, overall. If you are like me, you may want to think about whether this company will grow or shrink. Luckily, you can check this free report showing analyst forecasts for its future.

If you would prefer to check out another company -- one with potentially superior financials -- then do not miss this free list of interesting companies, that have HIGH return on equity and low debt.

For the purposes of this article, insiders are those individuals who report their transactions to the relevant regulatory body. We currently account for open market transactions and private dispositions of direct interests only, but not derivative transactions or indirect interests.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

① During the campaign period, US stocks, US stocks short selling, US stock options, Hong Kong stocks, and A-shares trading will maintain at $0 commission, and no subscription/redemption fees for mutual fund transactions. $0 fee offer has a time limit, until further notice. For more information, please visit: https://www.webull.hk/pricing

Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English