AEON Credit Service (Asia) (HKG:900) Is Paying Out A Larger Dividend Than Last Year

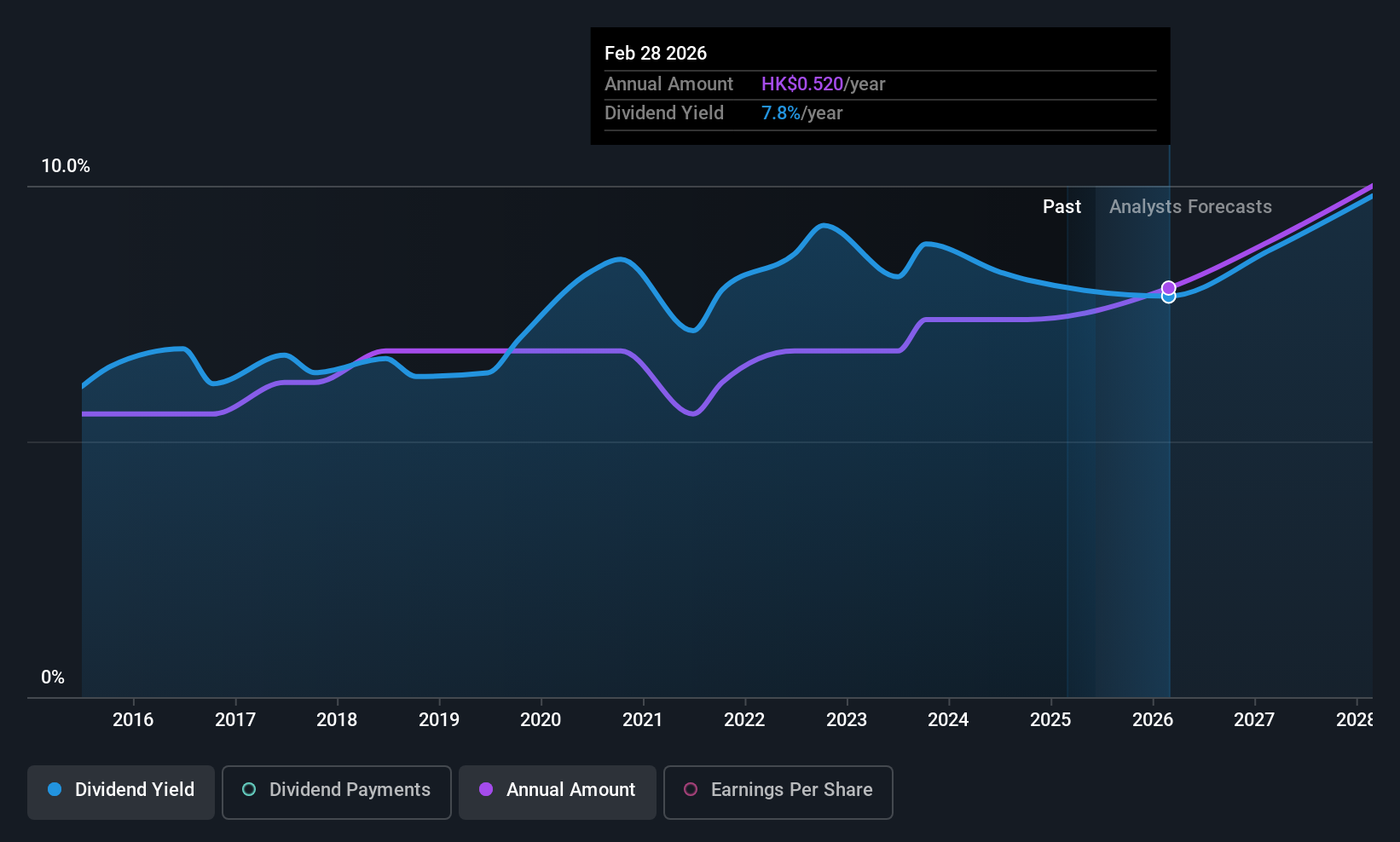

AEON Credit Service (Asia) Company Limited (HKG:900) has announced that it will be increasing its dividend from last year's comparable payment on the 31st of July to HK$0.25. Based on this payment, the dividend yield for the company will be 7.5%, which is fairly typical for the industry.

AEON Credit Service (Asia)'s Payment Could Potentially Have Solid Earnings Coverage

While it is always good to see a solid dividend yield, we should also consider whether the payment is feasible. Based on the last dividend, AEON Credit Service (Asia) is earning enough to cover the payment, but then it makes up 177% of cash flows. This signals that the company is more focused on returning cash flow to shareholders, but it could mean that the dividend is exposed to cuts in the future.

Over the next year, EPS is forecast to expand by 50.5%. If the dividend continues along recent trends, we estimate the payout ratio will be 35%, which is in the range that makes us comfortable with the sustainability of the dividend.

Check out our latest analysis for AEON Credit Service (Asia)

Dividend Volatility

The company has a long dividend track record, but it doesn't look great with cuts in the past. Since 2015, the annual payment back then was HK$0.36, compared to the most recent full-year payment of HK$0.50. This means that it has been growing its distributions at 3.3% per annum over that time. We're glad to see the dividend has risen, but with a limited rate of growth and fluctuations in the payments the total shareholder return may be limited.

AEON Credit Service (Asia) May Find It Hard To Grow The Dividend

Given that the dividend has been cut in the past, we need to check if earnings are growing and if that might lead to stronger dividends in the future. However, AEON Credit Service (Asia)'s EPS was effectively flat over the past five years, which could stop the company from paying more every year. The company has been growing at a pretty soft 1.6% per annum, and is paying out quite a lot of its earnings to shareholders. This could mean the dividend doesn't have the growth potential we look for going into the future.

Our Thoughts On AEON Credit Service (Asia)'s Dividend

Overall, this is probably not a great income stock, even though the dividend is being raised at the moment. While AEON Credit Service (Asia) is earning enough to cover the payments, the cash flows are lacking. We would be a touch cautious of relying on this stock primarily for the dividend income.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. However, there are other things to consider for investors when analysing stock performance. For example, we've identified 2 warning signs for AEON Credit Service (Asia) (1 is potentially serious!) that you should be aware of before investing. Is AEON Credit Service (Asia) not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

① During the campaign period, US stocks, US stocks short selling, US stock options, Hong Kong stocks, and A-shares trading will maintain at $0 commission, and no subscription/redemption fees for mutual fund transactions. $0 fee offer has a time limit, until further notice. For more information, please visit: https://www.webull.hk/pricing

Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English