Atour Lifestyle Holdings And 2 Other Stocks That Might Be Trading Below Estimated Value

As global markets experience turbulence due to geopolitical tensions, with the Dow Jones dropping significantly and oil prices surging, investors are increasingly on the lookout for opportunities that may be undervalued amidst the volatility. In such a fluctuating environment, identifying stocks that are trading below their estimated value can offer potential for growth and stability in an otherwise uncertain market landscape.

Top 10 Undervalued Stocks Based On Cash Flows In The United States

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Tuniu (TOUR) | $0.923 | $1.84 | 49.9% |

| Sotera Health (SHC) | $11.75 | $23.28 | 49.5% |

| Reddit (RDDT) | $116.20 | $229.48 | 49.4% |

| Lyft (LYFT) | $15.44 | $30.49 | 49.4% |

| Lincoln Educational Services (LINC) | $22.39 | $44.04 | 49.2% |

| Ligand Pharmaceuticals (LGND) | $114.45 | $225.70 | 49.3% |

| KBR (KBR) | $53.69 | $107.25 | 49.9% |

| First Busey (BUSE) | $22.79 | $45.56 | 50% |

| Constellium (CSTM) | $13.96 | $27.83 | 49.8% |

| Brookline Bancorp (BRKL) | $10.59 | $20.85 | 49.2% |

Underneath we present a selection of stocks filtered out by our screen.

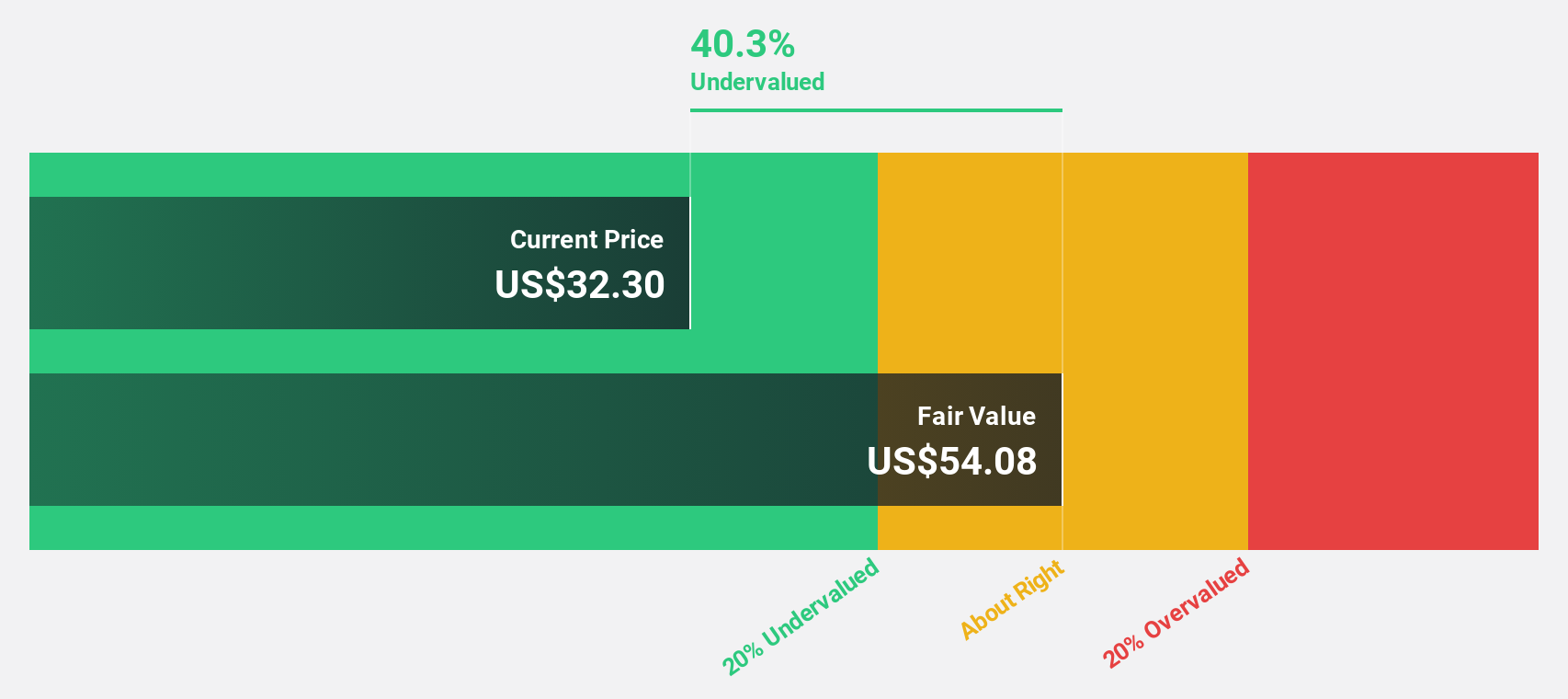

Atour Lifestyle Holdings (ATAT)

Overview: Atour Lifestyle Holdings Limited, with a market cap of $4.26 billion, develops lifestyle brands centered around hotel offerings in the People's Republic of China through its subsidiaries.

Operations: Atour Lifestyle Holdings generates its revenue of CN¥7.69 billion primarily from the Atour Group segment, focusing on lifestyle brand development related to hotel offerings in China.

Estimated Discount To Fair Value: 40.1%

Atour Lifestyle Holdings appears undervalued based on discounted cash flow analysis, trading at US$32.45, significantly below the estimated fair value of US$54.19. The company anticipates robust revenue growth of 20.5% annually, outpacing the broader U.S. market, alongside a projected earnings increase of 24.1% per year over three years. Recent initiatives include a US$400 million share repurchase program aimed at enhancing shareholder value and maintaining strong cash flow management despite decreased dividends.

- According our earnings growth report, there's an indication that Atour Lifestyle Holdings might be ready to expand.

- Click here and access our complete balance sheet health report to understand the dynamics of Atour Lifestyle Holdings.

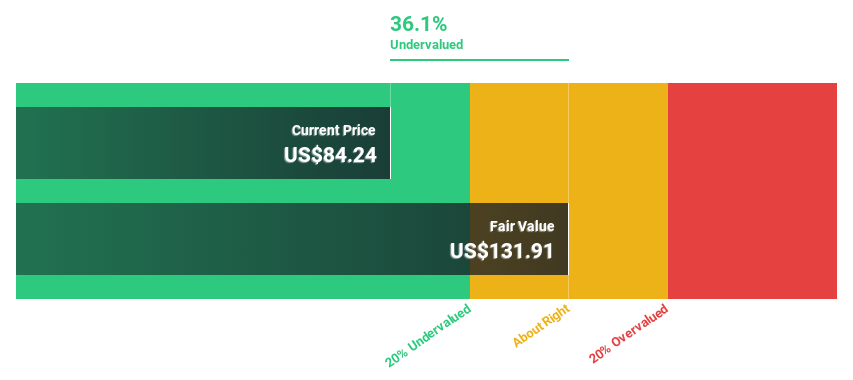

Bel Fuse (BELF.A)

Overview: Bel Fuse Inc. designs, manufactures, markets, and sells products that power, protect, and connect electronic circuits with a market cap of $1.04 billion.

Operations: The company's revenue is derived from three main segments: Magnetic Solutions ($73.77 million), Connectivity Solutions ($216.82 million), and Power Solutions and Protection ($268.36 million).

Estimated Discount To Fair Value: 43.4%

Bel Fuse is trading at US$79.78, considerably below its estimated fair value of US$140.9, highlighting potential undervaluation based on cash flows. Despite a decline in profit margins from 12.6% to 7.7%, earnings are forecast to grow significantly at 24.3% annually, surpassing the U.S. market average of 14.4%. Recent executive changes include Lynn Hutkin's appointment as CFO, which may influence Bel's financial strategies and performance going forward amidst high debt levels.

- The growth report we've compiled suggests that Bel Fuse's future prospects could be on the up.

- Click to explore a detailed breakdown of our findings in Bel Fuse's balance sheet health report.

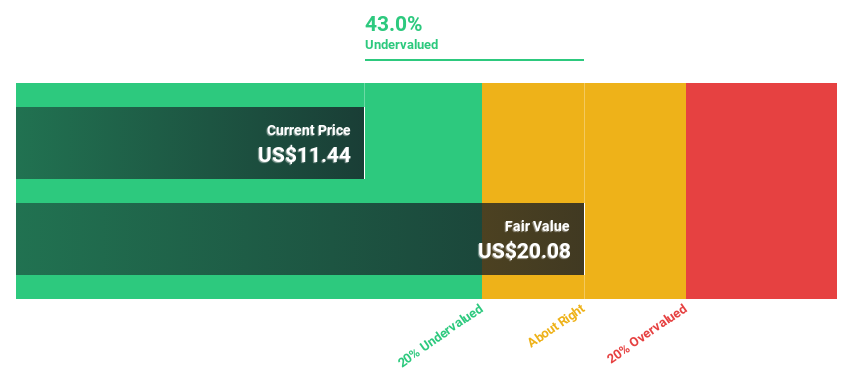

Constellium (CSTM)

Overview: Constellium SE, with a market cap of approximately $1.96 billion, specializes in designing, manufacturing, and selling rolled and extruded aluminum products for various sectors including aerospace, packaging, automotive, commercial transportation, general industrial, and defense.

Operations: The company's revenue segments include Aerospace and Transportation with $1.81 billion, Automotive Structures and Industry at $1.42 billion, and Packaging and Automotive Rolled Products contributing $4.37 billion.

Estimated Discount To Fair Value: 49.8%

Constellium, trading at US$13.96, is significantly undervalued relative to its fair value estimate of US$27.83. Despite a decrease in profit margins from 2% to 1%, earnings are expected to grow substantially at 48% annually, outpacing the U.S. market average of 14.4%. Recent strategic initiatives include successful aluminum recycling for aerospace applications and collaborations on additive manufacturing projects, potentially enhancing long-term cash flow and sustainability prospects despite current debt concerns.

- Our comprehensive growth report raises the possibility that Constellium is poised for substantial financial growth.

- Get an in-depth perspective on Constellium's balance sheet by reading our health report here.

Key Takeaways

- Take a closer look at our Undervalued US Stocks Based On Cash Flows list of 174 companies by clicking here.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

① During the campaign period, US stocks, US stocks short selling, US stock options, Hong Kong stocks, and A-shares trading will maintain at $0 commission, and no subscription/redemption fees for mutual fund transactions. $0 fee offer has a time limit, until further notice. For more information, please visit: https://www.webull.hk/pricing

Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English