Pak Tak International Limited's (HKG:2668) CEO Will Probably Find It Hard To See A Huge Raise This Year

Key Insights

- Pak Tak International to hold its Annual General Meeting on 20th of June

- CEO Pu Qian's total compensation includes salary of HK$1.58m

- Total compensation is similar to the industry average

- Over the past three years, Pak Tak International's EPS fell by 81% and over the past three years, the total loss to shareholders 69%

In the past three years, the share price of Pak Tak International Limited (HKG:2668) has struggled to grow and now shareholders are sitting on a loss. In addition, the company's per-share earnings growth is not looking good, despite growing revenues. Shareholders will have a chance to take their concerns to the board at the next AGM on 20th of June and vote on resolutions including executive compensation, which studies show may have an impact on company performance. Here's our take on why we think shareholders might be hesitant about approving a raise at the moment.

View our latest analysis for Pak Tak International

Comparing Pak Tak International Limited's CEO Compensation With The Industry

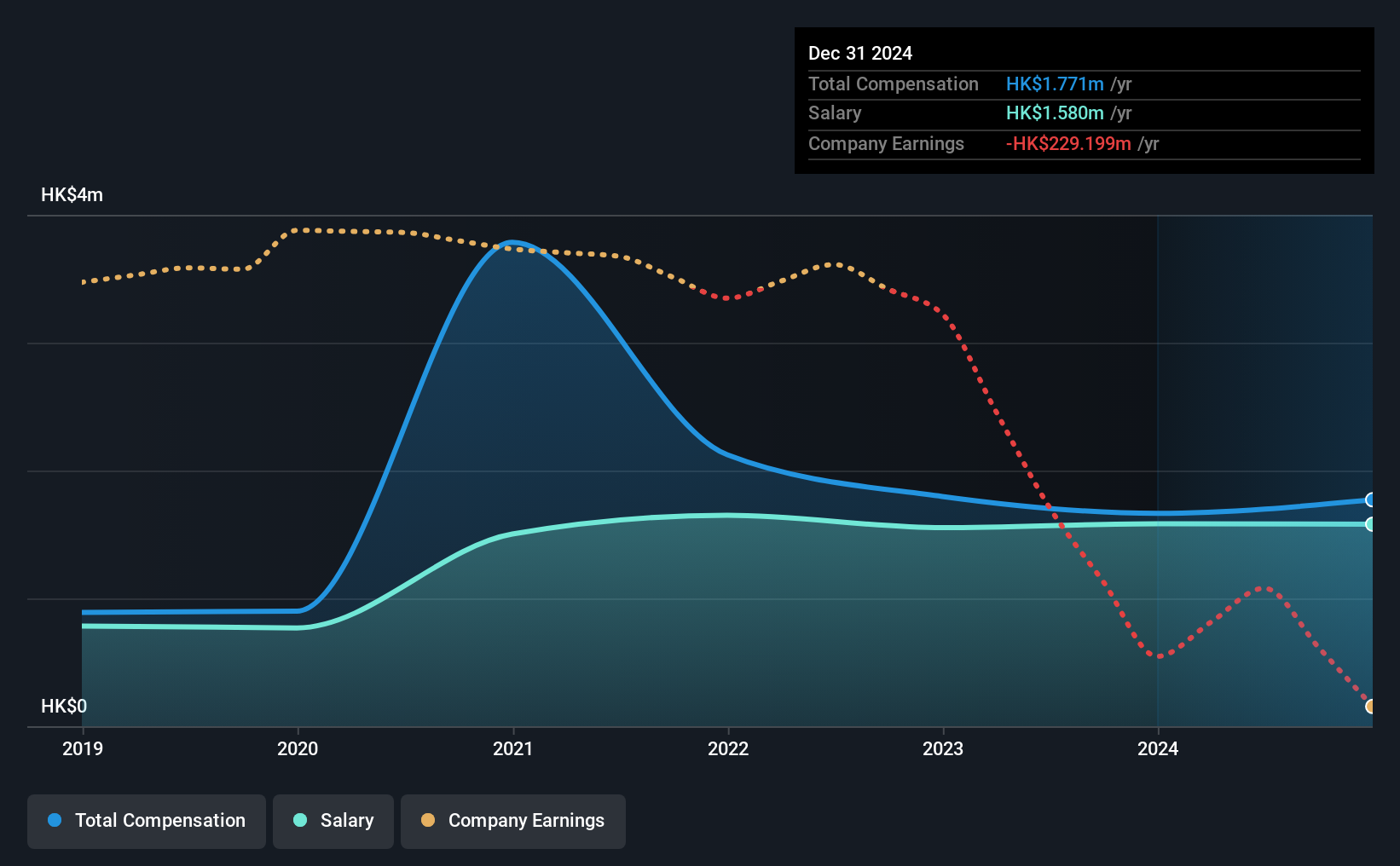

According to our data, Pak Tak International Limited has a market capitalization of HK$360m, and paid its CEO total annual compensation worth HK$1.8m over the year to December 2024. That's just a smallish increase of 6.4% on last year. Notably, the salary which is HK$1.58m, represents most of the total compensation being paid.

For comparison, other companies in the Hong Kong Luxury industry with market capitalizations below HK$1.6b, reported a median total CEO compensation of HK$2.2m. From this we gather that Pu Qian is paid around the median for CEOs in the industry.

| Component | 2024 | 2023 | Proportion (2024) |

| Salary | HK$1.6m | HK$1.6m | 89% |

| Other | HK$191k | HK$81k | 11% |

| Total Compensation | HK$1.8m | HK$1.7m | 100% |

On an industry level, around 89% of total compensation represents salary and 11% is other remuneration. Our data reveals that Pak Tak International allocates salary more or less in line with the wider market. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

Pak Tak International Limited's Growth

Over the last three years, Pak Tak International Limited has shrunk its earnings per share by 81% per year. Its revenue is up 58% over the last year.

The reduction in EPS, over three years, is arguably concerning. But in contrast the revenue growth is strong, suggesting future potential for EPS growth. These two metrics are moving in different directions, so while it's hard to be confident judging performance, we think the stock is worth watching. Although we don't have analyst forecasts, you might want to assess this data-rich visualization of earnings, revenue and cash flow.

Has Pak Tak International Limited Been A Good Investment?

Few Pak Tak International Limited shareholders would feel satisfied with the return of -69% over three years. So shareholders would probably want the company to be less generous with CEO compensation.

To Conclude...

The loss to shareholders over the past three years is certainly concerning and possibly has something to do with the fact that the company's earnings haven't grown. The upcoming AGM will provide shareholders the opportunity to revisit the company’s remuneration policies and evaluate if the board’s judgement and decision-making is aligned with that of the company’s shareholders.

CEO compensation is an important area to keep your eyes on, but we've also need to pay attention to other attributes of the company. We identified 5 warning signs for Pak Tak International (3 don't sit too well with us!) that you should be aware of before investing here.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Contact Us

Contact Number : +852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English