Okura Holdings' (HKG:1655) Returns On Capital Are Heading Higher

If we want to find a stock that could multiply over the long term, what are the underlying trends we should look for? One common approach is to try and find a company with returns on capital employed (ROCE) that are increasing, in conjunction with a growing amount of capital employed. Ultimately, this demonstrates that it's a business that is reinvesting profits at increasing rates of return. With that in mind, we've noticed some promising trends at Okura Holdings (HKG:1655) so let's look a bit deeper.

Return On Capital Employed (ROCE): What Is It?

For those that aren't sure what ROCE is, it measures the amount of pre-tax profits a company can generate from the capital employed in its business. The formula for this calculation on Okura Holdings is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

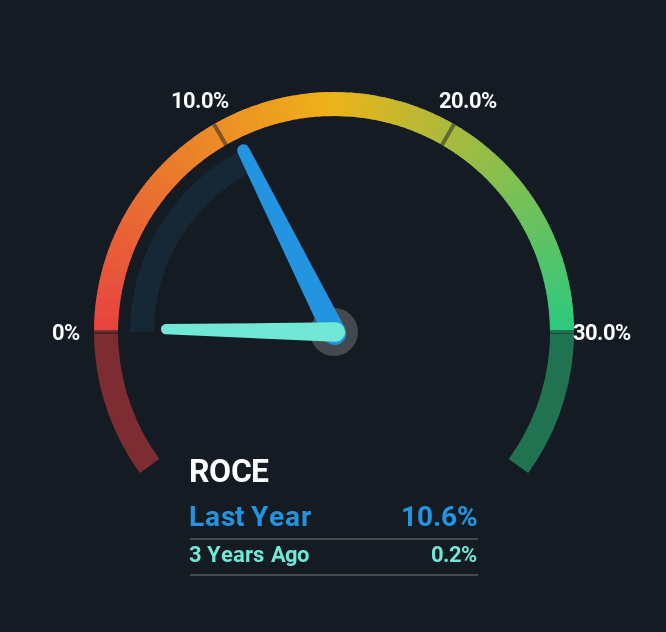

0.11 = JP¥1.6b ÷ (JP¥18b - JP¥3.0b) (Based on the trailing twelve months to December 2024).

Therefore, Okura Holdings has an ROCE of 11%. On its own, that's a standard return, however it's much better than the 7.0% generated by the Hospitality industry.

See our latest analysis for Okura Holdings

Historical performance is a great place to start when researching a stock so above you can see the gauge for Okura Holdings' ROCE against it's prior returns. If you want to delve into the historical earnings , check out these free graphs detailing revenue and cash flow performance of Okura Holdings.

What The Trend Of ROCE Can Tell Us

We're pretty happy with how the ROCE has been trending at Okura Holdings. The figures show that over the last five years, returns on capital have grown by 158%. The company is now earning JP¥0.1 per dollar of capital employed. Speaking of capital employed, the company is actually utilizing 42% less than it was five years ago, which can be indicative of a business that's improving its efficiency. A business that's shrinking its asset base like this isn't usually typical of a soon to be multi-bagger company.

In Conclusion...

In the end, Okura Holdings has proven it's capital allocation skills are good with those higher returns from less amount of capital. Although the company may be facing some issues elsewhere since the stock has plunged 85% in the last five years. In any case, we believe the economic trends of this company are positive and looking into the stock further could prove rewarding.

One more thing: We've identified 2 warning signs with Okura Holdings (at least 1 which makes us a bit uncomfortable) , and understanding them would certainly be useful.

If you want to search for solid companies with great earnings, check out this free list of companies with good balance sheets and impressive returns on equity.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Contact Us

Contact Number : +852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English