Here's Why Akeso, Inc.'s (HKG:9926) CEO May Deserve A Raise

Key Insights

- Akeso will host its Annual General Meeting on 30th of June

- Total pay for CEO Michelle Xia includes CN¥4.74m salary

- Total compensation is 94% below industry average

- Over the past three years, Akeso's EPS grew by 43% and over the past three years, the total shareholder return was 284%

The impressive results at Akeso, Inc. (HKG:9926) recently will be great news for shareholders. This would be kept in mind at the upcoming AGM on 30th of June which will be a chance for them to hear the board review the financial results, discuss future company strategy and vote on resolutions such as executive remuneration and other matters. Let's take a look at why we think the CEO has done a good job and we'll present the case for a bump in pay.

See our latest analysis for Akeso

How Does Total Compensation For Michelle Xia Compare With Other Companies In The Industry?

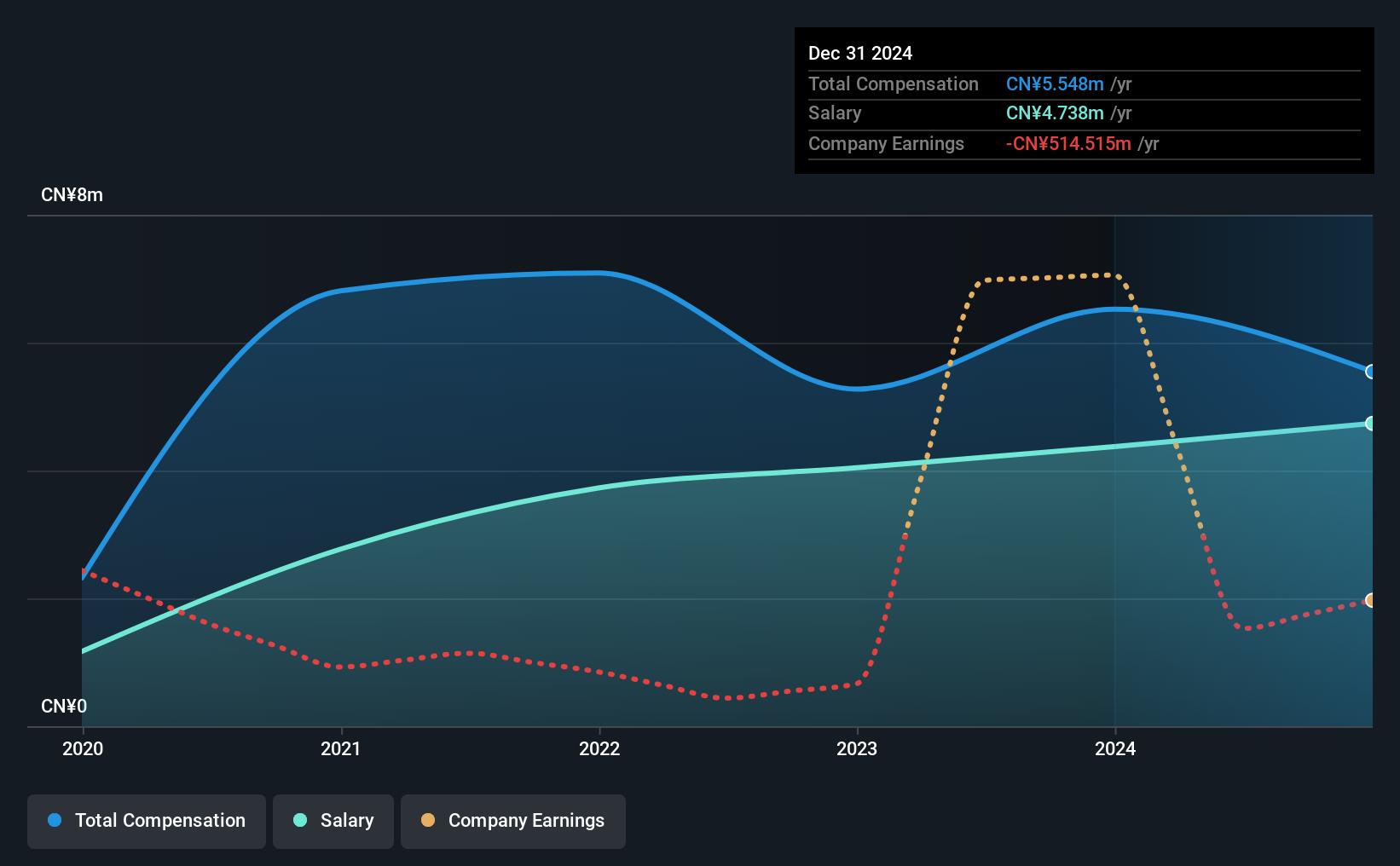

At the time of writing, our data shows that Akeso, Inc. has a market capitalization of HK$85b, and reported total annual CEO compensation of CN¥5.5m for the year to December 2024. That's a notable decrease of 15% on last year. Notably, the salary which is CN¥4.74m, represents most of the total compensation being paid.

On comparing similar companies in the Hong Kong Biotechs industry with market capitalizations above HK$63b, we found that the median total CEO compensation was CN¥94m. Accordingly, Akeso pays its CEO under the industry median. Moreover, Michelle Xia also holds HK$7.3b worth of Akeso stock directly under their own name, which reveals to us that they have a significant personal stake in the company.

| Component | 2024 | 2023 | Proportion (2024) |

| Salary | CN¥4.7m | CN¥4.4m | 85% |

| Other | CN¥810k | CN¥2.2m | 15% |

| Total Compensation | CN¥5.5m | CN¥6.5m | 100% |

On an industry level, roughly 52% of total compensation represents salary and 48% is other remuneration. Akeso pays out 85% of remuneration in the form of a salary, significantly higher than the industry average. If salary dominates total compensation, it suggests that CEO compensation is leaning less towards the variable component, which is usually linked with performance.

Akeso, Inc.'s Growth

Akeso, Inc.'s earnings per share (EPS) grew 43% per year over the last three years. In the last year, its revenue is down 53%.

Overall this is a positive result for shareholders, showing that the company has improved in recent years. The lack of revenue growth isn't ideal, but it is the bottom line that counts most in business. Historical performance can sometimes be a good indicator on what's coming up next but if you want to peer into the company's future you might be interested in this free visualization of analyst forecasts.

Has Akeso, Inc. Been A Good Investment?

Boasting a total shareholder return of 284% over three years, Akeso, Inc. has done well by shareholders. So they may not be at all concerned if the CEO were to be paid more than is normal for companies around the same size.

In Summary...

The company's solid performance might have made most shareholders happy, possibly making CEO remuneration the least of the matters to be discussed in the AGM. However, investors will get the chance to engage on key strategic initiatives and future growth opportunities for the company and set their longer-term expectations.

While it is important to pay attention to CEO remuneration, investors should also consider other elements of the business. We did our research and spotted 1 warning sign for Akeso that investors should look into moving forward.

Important note: Akeso is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

① During the campaign period, US stocks, US stocks short selling, US stock options, Hong Kong stocks, and A-shares trading will maintain at $0 commission, and no subscription/redemption fees for mutual fund transactions. $0 fee offer has a time limit, until further notice. For more information, please visit: https://www.webull.hk/pricing

Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English