Insiders were the key beneficiaries as Mabpharm Limited's (HKG:2181) market cap rises to HK$2.1b

Key Insights

- Insiders appear to have a vested interest in Mabpharm's growth, as seen by their sizeable ownership

- 68% of the business is held by the top 2 shareholders

- Ownership research, combined with past performance data can help provide a good understanding of opportunities in a stock

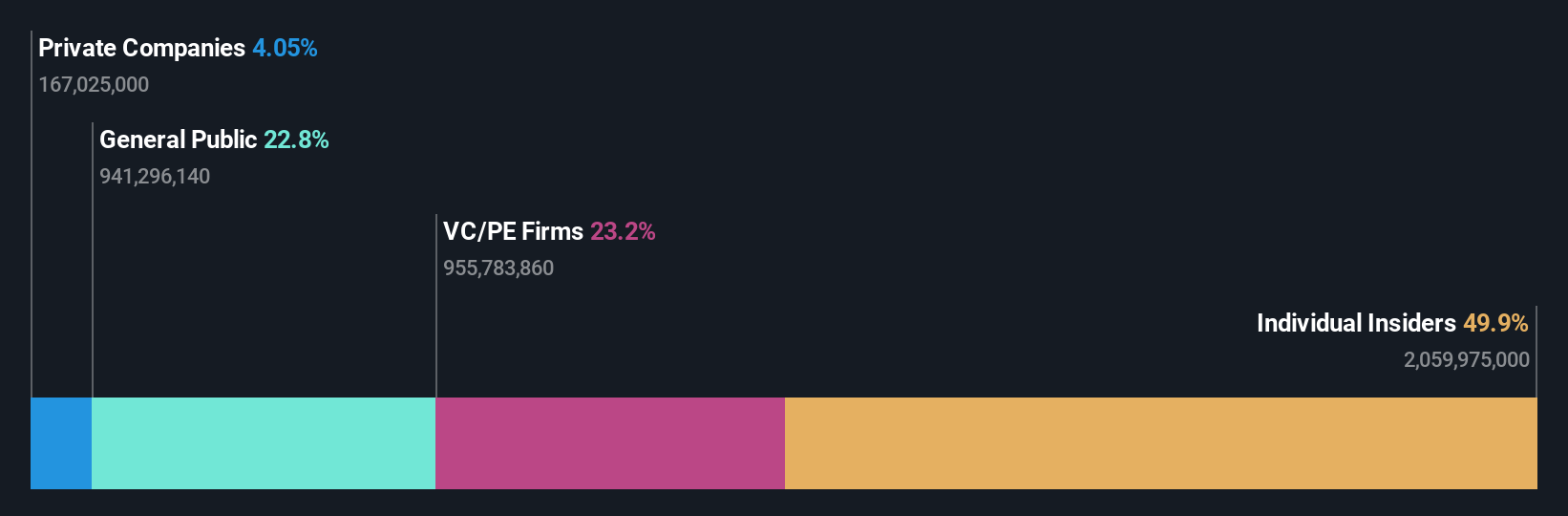

A look at the shareholders of Mabpharm Limited (HKG:2181) can tell us which group is most powerful. And the group that holds the biggest piece of the pie are individual insiders with 50% ownership. Put another way, the group faces the maximum upside potential (or downside risk).

Clearly, insiders benefitted the most after the company's market cap rose by HK$206m last week.

Let's delve deeper into each type of owner of Mabpharm, beginning with the chart below.

See our latest analysis for Mabpharm

What Does The Lack Of Institutional Ownership Tell Us About Mabpharm?

We don't tend to see institutional investors holding stock of companies that are very risky, thinly traded, or very small. Though we do sometimes see large companies without institutions on the register, it's not particularly common.

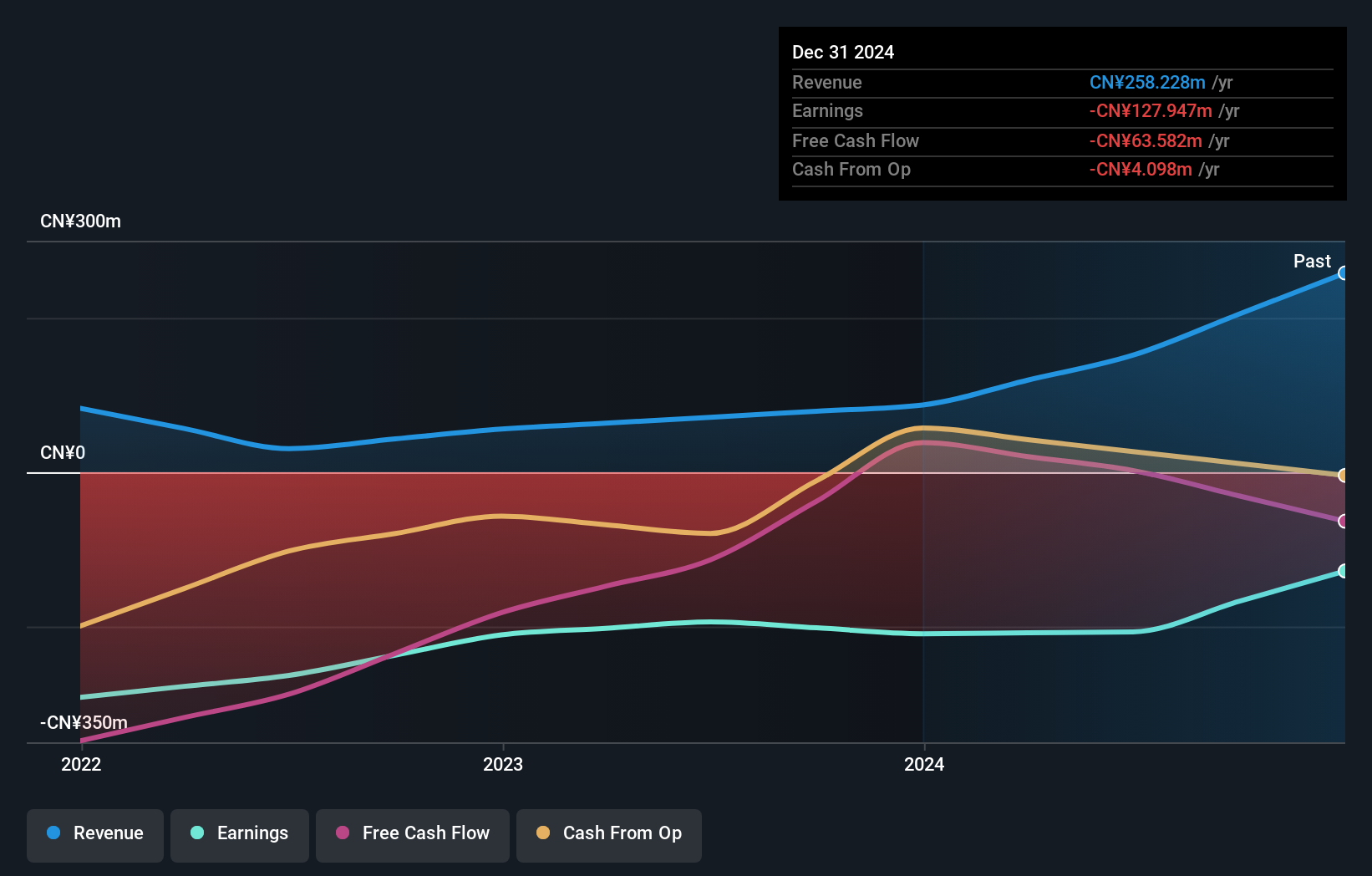

There are many reasons why a company might not have any institutions on the share registry. It may be hard for institutions to buy large amounts of shares, if liquidity (the amount of shares traded each day) is low. If the company has not needed to raise capital, institutions might lack the opportunity to build a position. Alternatively, there might be something about the company that has kept institutional investors away. Mabpharm's earnings and revenue track record (below) may not be compelling to institutional investors -- or they simply might not have looked at the business closely.

Mabpharm is not owned by hedge funds. Our data shows that Jianjun Guo is the largest shareholder with 50% of shares outstanding. For context, the second largest shareholder holds about 18% of the shares outstanding, followed by an ownership of 5.2% by the third-largest shareholder.

To make our study more interesting, we found that the top 2 shareholders have a majority ownership in the company, meaning that they are powerful enough to influence the decisions of the company.

Researching institutional ownership is a good way to gauge and filter a stock's expected performance. The same can be achieved by studying analyst sentiments. As far as we can tell there isn't analyst coverage of the company, so it is probably flying under the radar.

Insider Ownership Of Mabpharm

The definition of company insiders can be subjective and does vary between jurisdictions. Our data reflects individual insiders, capturing board members at the very least. Company management run the business, but the CEO will answer to the board, even if he or she is a member of it.

Insider ownership is positive when it signals leadership are thinking like the true owners of the company. However, high insider ownership can also give immense power to a small group within the company. This can be negative in some circumstances.

It seems insiders own a significant proportion of Mabpharm Limited. It has a market capitalization of just HK$2.1b, and insiders have HK$1.0b worth of shares in their own names. This may suggest that the founders still own a lot of shares. You can click here to see if they have been buying or selling.

General Public Ownership

The general public, who are usually individual investors, hold a 23% stake in Mabpharm. This size of ownership, while considerable, may not be enough to change company policy if the decision is not in sync with other large shareholders.

Private Equity Ownership

With an ownership of 23%, private equity firms are in a position to play a role in shaping corporate strategy with a focus on value creation. Some might like this, because private equity are sometimes activists who hold management accountable. But other times, private equity is selling out, having taking the company public.

Private Company Ownership

We can see that Private Companies own 4.0%, of the shares on issue. Private companies may be related parties. Sometimes insiders have an interest in a public company through a holding in a private company, rather than in their own capacity as an individual. While it's hard to draw any broad stroke conclusions, it is worth noting as an area for further research.

Next Steps:

I find it very interesting to look at who exactly owns a company. But to truly gain insight, we need to consider other information, too. Consider risks, for instance. Every company has them, and we've spotted 2 warning signs for Mabpharm you should know about.

Of course this may not be the best stock to buy. So take a peek at this free free list of interesting companies.

NB: Figures in this article are calculated using data from the last twelve months, which refer to the 12-month period ending on the last date of the month the financial statement is dated. This may not be consistent with full year annual report figures.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Contact Us

Contact Number : +852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English