Beauty Farm Medical and Health Industry (HKG:2373) Could Be Struggling To Allocate Capital

Finding a business that has the potential to grow substantially is not easy, but it is possible if we look at a few key financial metrics. Typically, we'll want to notice a trend of growing return on capital employed (ROCE) and alongside that, an expanding base of capital employed. If you see this, it typically means it's a company with a great business model and plenty of profitable reinvestment opportunities. Having said that, while the ROCE is currently high for Beauty Farm Medical and Health Industry (HKG:2373), we aren't jumping out of our chairs because returns are decreasing.

What Is Return On Capital Employed (ROCE)?

For those that aren't sure what ROCE is, it measures the amount of pre-tax profits a company can generate from the capital employed in its business. Analysts use this formula to calculate it for Beauty Farm Medical and Health Industry:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

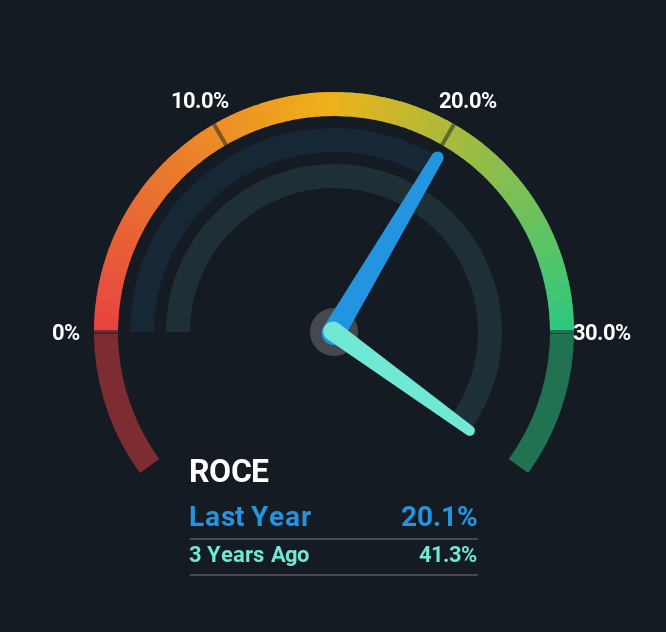

0.20 = CN¥309m ÷ (CN¥4.3b - CN¥2.7b) (Based on the trailing twelve months to December 2024).

Therefore, Beauty Farm Medical and Health Industry has an ROCE of 20%. In absolute terms that's a great return and it's even better than the Consumer Services industry average of 9.2%.

See our latest analysis for Beauty Farm Medical and Health Industry

Above you can see how the current ROCE for Beauty Farm Medical and Health Industry compares to its prior returns on capital, but there's only so much you can tell from the past. If you'd like, you can check out the forecasts from the analysts covering Beauty Farm Medical and Health Industry for free.

What The Trend Of ROCE Can Tell Us

When we looked at the ROCE trend at Beauty Farm Medical and Health Industry, we didn't gain much confidence. While it's comforting that the ROCE is high, five years ago it was 41%. Although, given both revenue and the amount of assets employed in the business have increased, it could suggest the company is investing in growth, and the extra capital has led to a short-term reduction in ROCE. If these investments prove successful, this can bode very well for long term stock performance.

Another thing to note, Beauty Farm Medical and Health Industry has a high ratio of current liabilities to total assets of 64%. This can bring about some risks because the company is basically operating with a rather large reliance on its suppliers or other sorts of short-term creditors. Ideally we'd like to see this reduce as that would mean fewer obligations bearing risks.

The Key Takeaway

Even though returns on capital have fallen in the short term, we find it promising that revenue and capital employed have both increased for Beauty Farm Medical and Health Industry. Furthermore the stock has climbed 71% over the last year, it would appear that investors are upbeat about the future. So should these growth trends continue, we'd be optimistic on the stock going forward.

On a separate note, we've found 1 warning sign for Beauty Farm Medical and Health Industry you'll probably want to know about.

Beauty Farm Medical and Health Industry is not the only stock earning high returns. If you'd like to see more, check out our free list of companies earning high returns on equity with solid fundamentals.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Contact Us

Contact Number : +852 3852 8500Service Email : service@webull.hkBusiness Cooperation : marketinghk@webull.hkWebull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English