Shareholders May Not Be So Generous With China Metal Resources Utilization Limited's (HKG:1636) CEO Compensation And Here's Why

Key Insights

- China Metal Resources Utilization's Annual General Meeting to take place on 30th of June

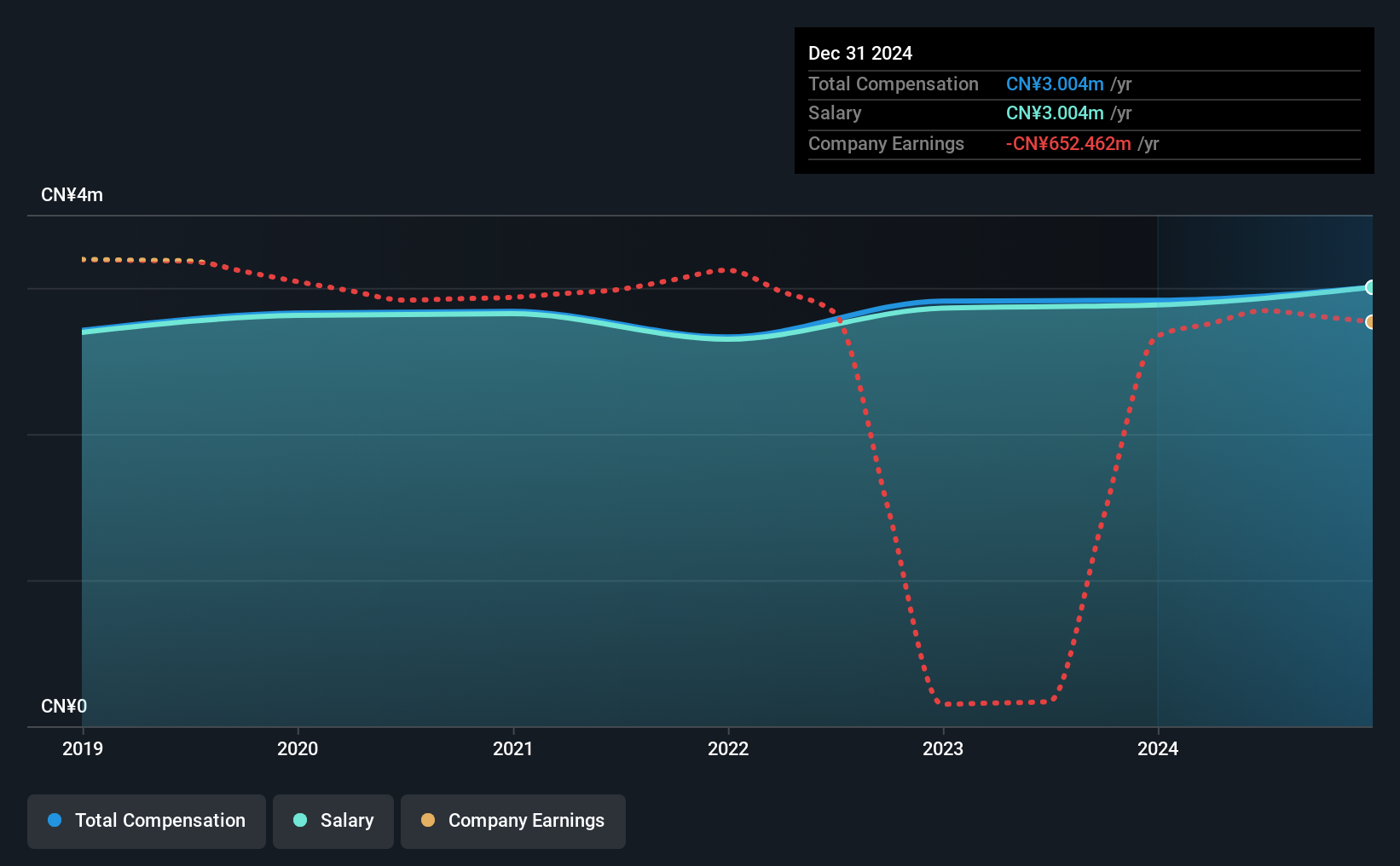

- CEO Jianqiu Yu's total compensation includes salary of CN¥3.00m

- Total compensation is 233% above industry average

- Over the past three years, China Metal Resources Utilization's EPS grew by 16% and over the past three years, the total loss to shareholders 71%

Shareholders of China Metal Resources Utilization Limited (HKG:1636) will have been dismayed by the negative share price return over the last three years. What is concerning is that despite positive EPS growth, the share price has not tracked the trend in fundamentals. The AGM coming up on the 30th of June could be an opportunity for shareholders to bring these concerns to the board's attention. They could also influence management through voting on resolutions such as executive remuneration. We think shareholders might be reluctant to increase compensation for the CEO at the moment, according to our analysis below.

Check out our latest analysis for China Metal Resources Utilization

How Does Total Compensation For Jianqiu Yu Compare With Other Companies In The Industry?

Our data indicates that China Metal Resources Utilization Limited has a market capitalization of HK$137m, and total annual CEO compensation was reported as CN¥3.0m for the year to December 2024. That's just a smallish increase of 3.1% on last year. It is worth noting that the CEO compensation consists entirely of the salary, worth CN¥3.0m.

In comparison with other companies in the Hong Kong Metals and Mining industry with market capitalizations under HK$1.6b, the reported median total CEO compensation was CN¥902k. Hence, we can conclude that Jianqiu Yu is remunerated higher than the industry median. Furthermore, Jianqiu Yu directly owns HK$16m worth of shares in the company, implying that they are deeply invested in the company's success.

| Component | 2024 | 2023 | Proportion (2024) |

| Salary | CN¥3.0m | CN¥2.9m | 100% |

| Other | - | CN¥32k | - |

| Total Compensation | CN¥3.0m | CN¥2.9m | 100% |

On an industry level, around 83% of total compensation represents salary and 17% is other remuneration. At the company level, China Metal Resources Utilization pays Jianqiu Yu solely through a salary, preferring to go down a conventional route. If salary is the major component in total compensation, it suggests that the CEO receives a higher fixed proportion of the total compensation, regardless of performance.

A Look at China Metal Resources Utilization Limited's Growth Numbers

China Metal Resources Utilization Limited's earnings per share (EPS) grew 16% per year over the last three years. It saw its revenue drop 44% over the last year.

Overall this is a positive result for shareholders, showing that the company has improved in recent years. The lack of revenue growth isn't ideal, but it is the bottom line that counts most in business. Although we don't have analyst forecasts, you might want to assess this data-rich visualization of earnings, revenue and cash flow.

Has China Metal Resources Utilization Limited Been A Good Investment?

With a total shareholder return of -71% over three years, China Metal Resources Utilization Limited shareholders would by and large be disappointed. Therefore, it might be upsetting for shareholders if the CEO were paid generously.

To Conclude...

China Metal Resources Utilization rewards its CEO solely through a salary, ignoring non-salary benefits completely. The fact that shareholders are sitting on a loss on the value of their shares in the past few years is certainly disconcerting. The stock's movement is disjointed with the company's earnings growth, which ideally should move in the same direction. If there are some unknown variables that are influencing the stock's price, surely shareholders would have some concerns. These concerns should be addressed at the upcoming AGM, where shareholders can question the board and evaluate if their judgement and decision making is still in line with their expectations.

CEO pay is simply one of the many factors that need to be considered while examining business performance. That's why we did our research, and identified 5 warning signs for China Metal Resources Utilization (of which 4 are significant!) that you should know about in order to have a holistic understanding of the stock.

Switching gears from China Metal Resources Utilization, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Contact Us

Contact Number : +852 3852 8500Service Email : service@webull.hkBusiness Cooperation : marketinghk@webull.hkWebull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English