Beauty Farm Medical and Health Industry Inc. (HKG:2373) Looks Just Right With A 26% Price Jump

Despite an already strong run, Beauty Farm Medical and Health Industry Inc. (HKG:2373) shares have been powering on, with a gain of 26% in the last thirty days. The last 30 days bring the annual gain to a very sharp 86%.

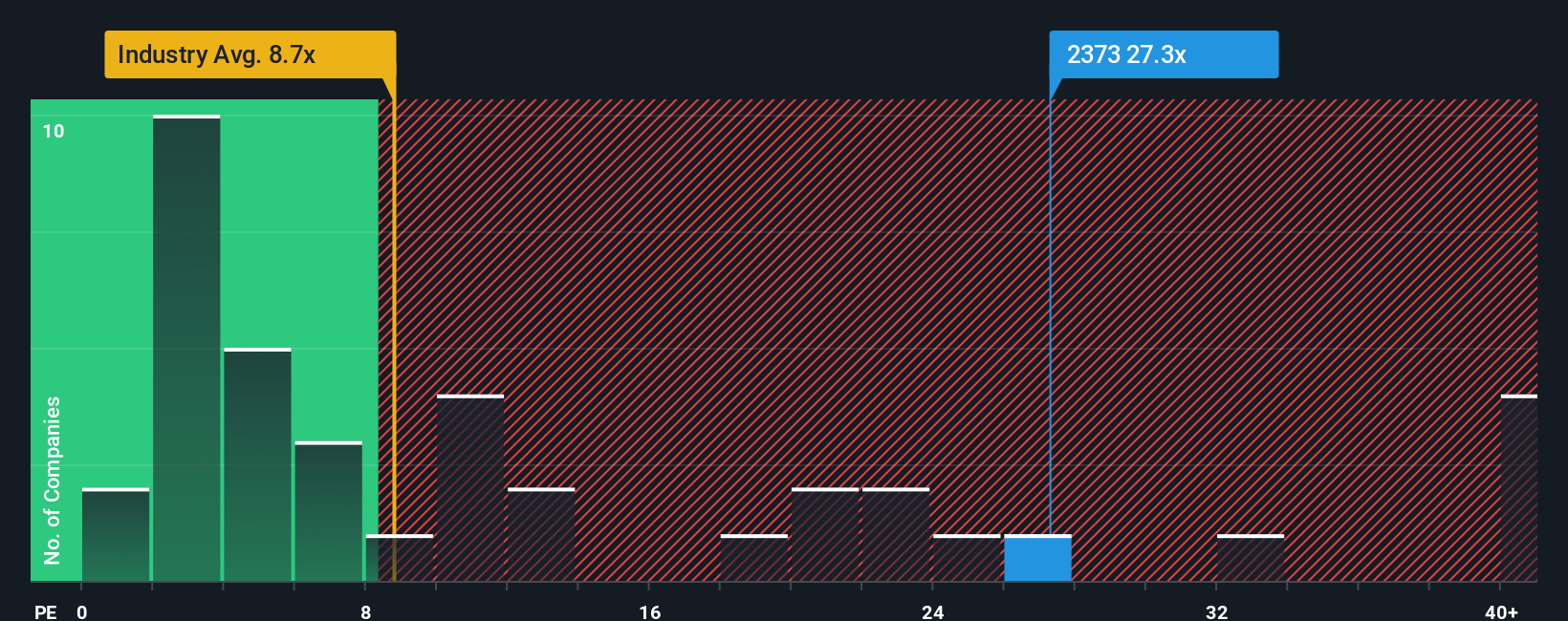

After such a large jump in price, Beauty Farm Medical and Health Industry may be sending very bearish signals at the moment with a price-to-earnings (or "P/E") ratio of 27.3x, since almost half of all companies in Hong Kong have P/E ratios under 11x and even P/E's lower than 6x are not unusual. However, the P/E might be quite high for a reason and it requires further investigation to determine if it's justified.

With earnings growth that's superior to most other companies of late, Beauty Farm Medical and Health Industry has been doing relatively well. It seems that many are expecting the strong earnings performance to persist, which has raised the P/E. If not, then existing shareholders might be a little nervous about the viability of the share price.

View our latest analysis for Beauty Farm Medical and Health Industry

Does Growth Match The High P/E?

In order to justify its P/E ratio, Beauty Farm Medical and Health Industry would need to produce outstanding growth well in excess of the market.

Retrospectively, the last year delivered a decent 5.5% gain to the company's bottom line. Still, EPS has barely risen at all in aggregate from three years ago, which is not ideal. Therefore, it's fair to say that earnings growth has been inconsistent recently for the company.

Looking ahead now, EPS is anticipated to climb by 20% per annum during the coming three years according to the four analysts following the company. That's shaping up to be materially higher than the 14% per annum growth forecast for the broader market.

With this information, we can see why Beauty Farm Medical and Health Industry is trading at such a high P/E compared to the market. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

What We Can Learn From Beauty Farm Medical and Health Industry's P/E?

Shares in Beauty Farm Medical and Health Industry have built up some good momentum lately, which has really inflated its P/E. Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

We've established that Beauty Farm Medical and Health Industry maintains its high P/E on the strength of its forecast growth being higher than the wider market, as expected. At this stage investors feel the potential for a deterioration in earnings isn't great enough to justify a lower P/E ratio. Unless these conditions change, they will continue to provide strong support to the share price.

Plus, you should also learn about this 1 warning sign we've spotted with Beauty Farm Medical and Health Industry.

It's important to make sure you look for a great company, not just the first idea you come across. So take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Contact Us

Contact Number : +852 3852 8500Service Email : service@webull.hkBusiness Cooperation : marketinghk@webull.hkWebull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English