We Think Edgewell Personal Care (NYSE:EPC) Is Taking Some Risk With Its Debt

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies Edgewell Personal Care Company (NYSE:EPC) makes use of debt. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

How Much Debt Does Edgewell Personal Care Carry?

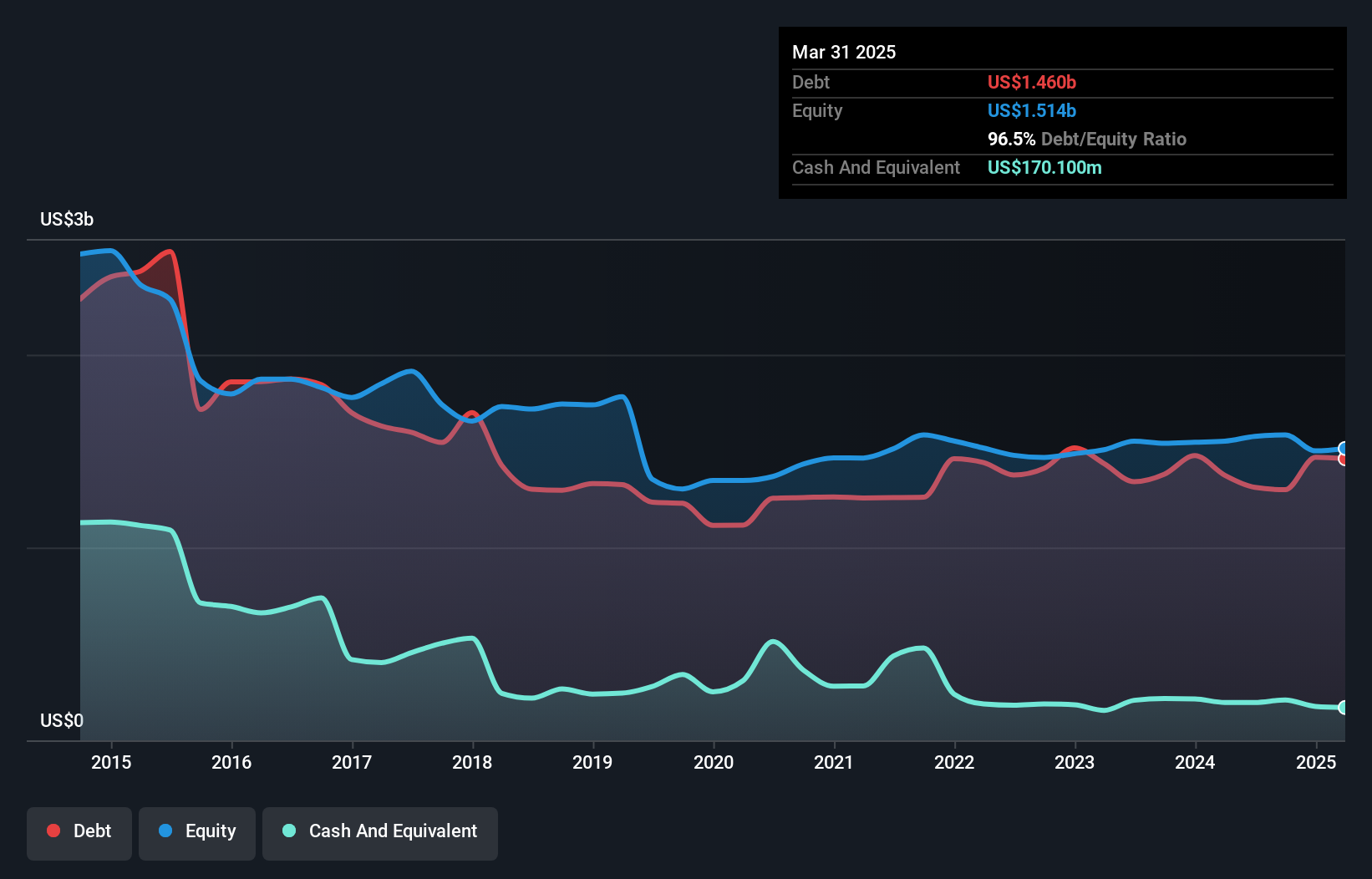

The image below, which you can click on for greater detail, shows that at March 2025 Edgewell Personal Care had debt of US$1.46b, up from US$1.37b in one year. On the flip side, it has US$170.1m in cash leading to net debt of about US$1.29b.

How Healthy Is Edgewell Personal Care's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Edgewell Personal Care had liabilities of US$536.3m due within 12 months and liabilities of US$1.72b due beyond that. Offsetting this, it had US$170.1m in cash and US$235.0m in receivables that were due within 12 months. So its liabilities total US$1.85b more than the combination of its cash and short-term receivables.

This deficit casts a shadow over the US$1.21b company, like a colossus towering over mere mortals. So we'd watch its balance sheet closely, without a doubt. At the end of the day, Edgewell Personal Care would probably need a major re-capitalization if its creditors were to demand repayment.

See our latest analysis for Edgewell Personal Care

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Edgewell Personal Care's debt is 4.0 times its EBITDA, and its EBIT cover its interest expense 3.2 times over. This suggests that while the debt levels are significant, we'd stop short of calling them problematic. Even more troubling is the fact that Edgewell Personal Care actually let its EBIT decrease by 3.5% over the last year. If it keeps going like that paying off its debt will be like running on a treadmill -- a lot of effort for not much advancement. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Edgewell Personal Care can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So we always check how much of that EBIT is translated into free cash flow. In the last three years, Edgewell Personal Care's free cash flow amounted to 48% of its EBIT, less than we'd expect. That's not great, when it comes to paying down debt.

Our View

We'd go so far as to say Edgewell Personal Care's level of total liabilities was disappointing. Having said that, its ability to convert EBIT to free cash flow isn't such a worry. Overall, it seems to us that Edgewell Personal Care's balance sheet is really quite a risk to the business. For this reason we're pretty cautious about the stock, and we think shareholders should keep a close eye on its liquidity. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. Be aware that Edgewell Personal Care is showing 4 warning signs in our investment analysis , and 1 of those is a bit unpleasant...

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Contact Us

Contact Number : +852 3852 8500Service Email : service@webull.hkBusiness Cooperation : marketinghk@webull.hkWebull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English