This Insider Has Just Sold Shares In Northern Trust

We wouldn't blame Northern Trust Corporation (NASDAQ:NTRS) shareholders if they were a little worried about the fact that Steven Fradkin, a company insider, recently netted about US$1.6m selling shares at an average price of US$129. However, that sale only accounted for 5.4% of their holding, so arguably it doesn't say much about their conviction.

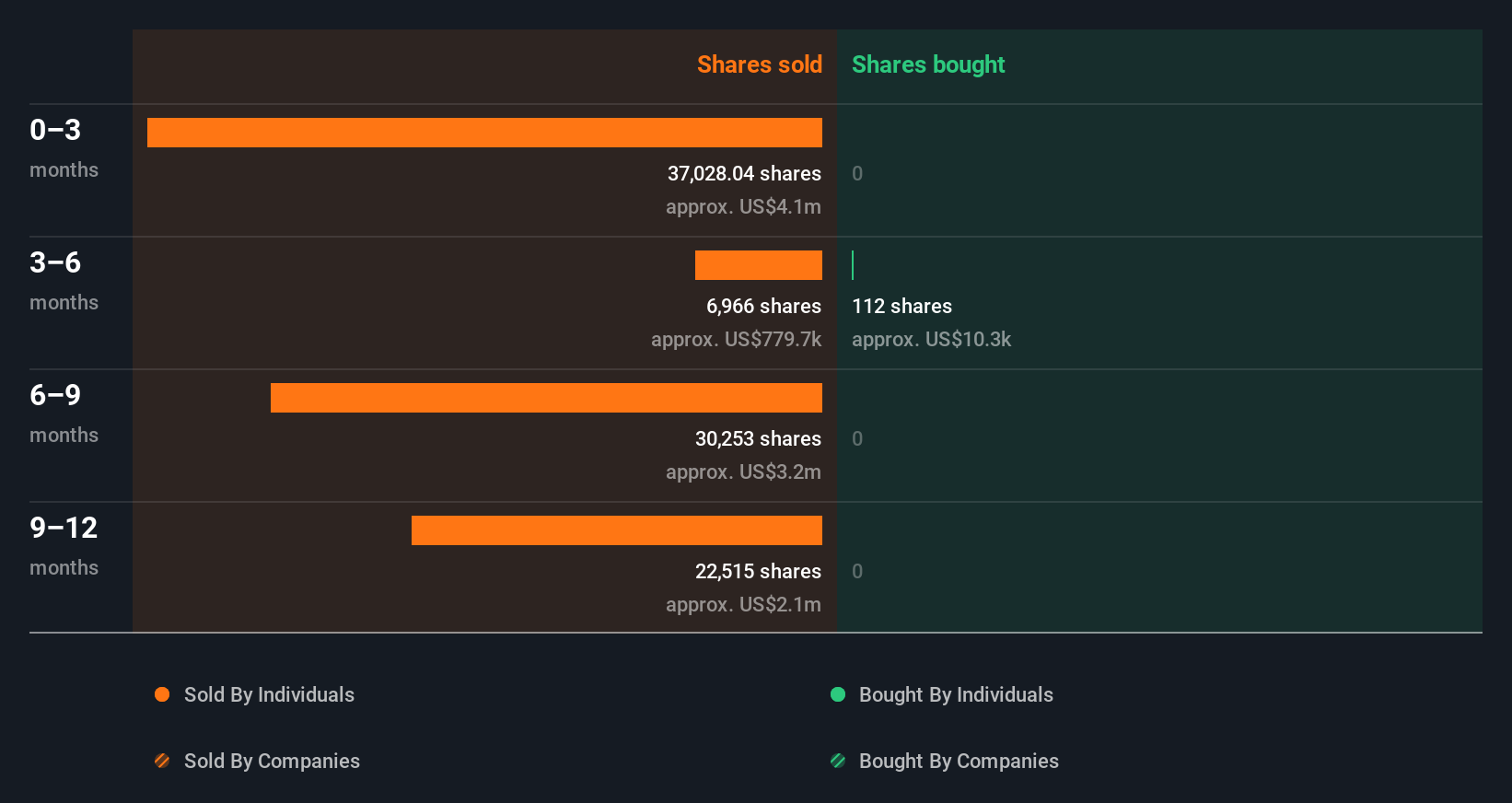

Northern Trust Insider Transactions Over The Last Year

The Executive VP & COO, Peter Cherecwich, made the biggest insider sale in the last 12 months. That single transaction was for US$1.7m worth of shares at a price of US$105 each. That means that an insider was selling shares at slightly below the current price (US$130). As a general rule we consider it to be discouraging when insiders are selling below the current price, because it suggests they were happy with a lower valuation. Please do note, however, that sellers may have a variety of reasons for selling, so we don't know for sure what they think of the stock price. We note that the biggest single sale was only 31% of Peter Cherecwich's holding.

Over the last year we saw more insider selling of Northern Trust shares, than buying. You can see a visual depiction of insider transactions (by companies and individuals) over the last 12 months, below. By clicking on the graph below, you can see the precise details of each insider transaction!

View our latest analysis for Northern Trust

For those who like to find hidden gems this free list of small cap companies with recent insider purchasing, could be just the ticket.

Does Northern Trust Boast High Insider Ownership?

For a common shareholder, it is worth checking how many shares are held by company insiders. Usually, the higher the insider ownership, the more likely it is that insiders will be incentivised to build the company for the long term. It's great to see that Northern Trust insiders own 1.5% of the company, worth about US$366m. I like to see this level of insider ownership, because it increases the chances that management are thinking about the best interests of shareholders.

What Might The Insider Transactions At Northern Trust Tell Us?

Insiders sold stock recently, but they haven't been buying. Zooming out, the longer term picture doesn't give us much comfort. But since Northern Trust is profitable and growing, we're not too worried by this. While insiders do own a lot of shares in the company (which is good), our analysis of their transactions doesn't make us feel confident about the company. In addition to knowing about insider transactions going on, it's beneficial to identify the risks facing Northern Trust. At Simply Wall St, we found 1 warning sign for Northern Trust that deserve your attention before buying any shares.

Of course, you might find a fantastic investment by looking elsewhere. So take a peek at this free list of interesting companies.

For the purposes of this article, insiders are those individuals who report their transactions to the relevant regulatory body. We currently account for open market transactions and private dispositions of direct interests only, but not derivative transactions or indirect interests.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Contact Us

Contact Number : +852 3852 8500Service Email : service@webull.hkBusiness Cooperation : marketinghk@webull.hkWebull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English