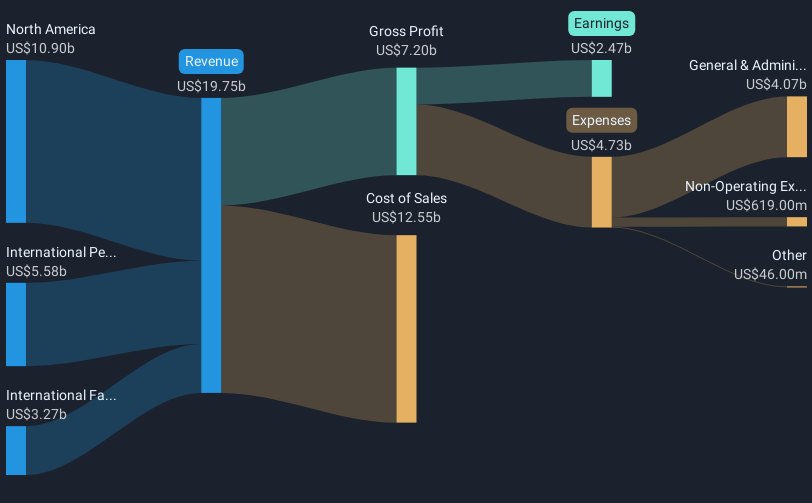

Kimberly-Clark (KMB) 2025 Guidance & Earnings: Sales Dip, Income Impacted by Divestitures

Kimberly-Clark (KMB) has recently experienced a 2% decline over the past week, which aligns with broad market trends influenced by global events. Despite a decline in Kimberly-Clark's second-quarter sales and net income, the company's guidance for organic sales growth to surpass current category and country averages presents a positive outlook. Meanwhile, external factors, such as the reintroduction of tariff uncertainties and a weaker-than-expected jobs report, have contributed to the downdraft affecting many shares including KMB. These elements may have added weight to the broader market setbacks rather than creating a company-specific effect.

We've spotted 1 weakness for Kimberly-Clark you should be aware of.

Outshine the giants: these 20 early-stage AI stocks could fund your retirement.

The recent 2% decline in Kimberly-Clark's shares may reflect broader market unease rather than specific company issues, aligning with global factors like tariff uncertainties and economic data. Despite these external pressures, the company's strategy of focusing on product innovation and cost efficiencies aims to position it favorably against potential headwinds in revenue and earnings forecasts. However, the pressure on margins due to ongoing global cost challenges could challenge achieving projected earnings growth.

Over the long term, the company's total shareholder return, including dividends, increased by 4.70% over a three-year period. This contextualizes the current price movement and highlights its relative stability though it underperformed the broader US market, which gained 15.7% over the past year, and the Household Products industry, which declined by 5.3%.

The stock is currently trading at US$124.62, which represents a discount of approximately 13% relative to the consensus analyst price target of US$140.83. This gap suggests potential upside if the company meets analyst projections, which include modest revenue declines and slight margin improvements over the coming years. Investors might weigh these factors against market volatility to determine if current valuations present a compelling opportunity.

Review our historical performance report to gain insights into Kimberly-Clark's track record.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number : +852 3852 8500Service Email : service@webull.hkBusiness Cooperation : marketinghk@webull.hkWebull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English