Should You Buy, Sell, or Hold Vertiv Stock Post Q2 Earnings?

Vertiv VRT shares have gained 1.1% since it reported second-quarter 2025 results on Wednesday. The uptick can be attributed to strong organic sales growth, driven by higher adjusted operating profit and robust performance across its regional segments.

Click here to check the details of Vertiv’s second-quarter 2025 results.

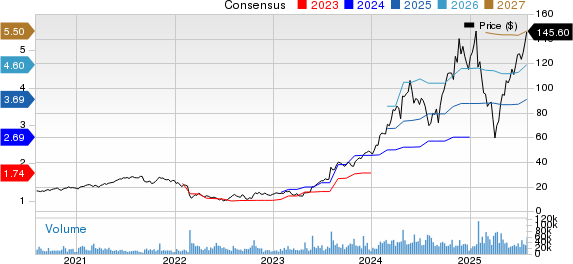

Vertiv shares have gained 28.4% year to date, outperforming the broader Zacks Computer and Technology sector’s increase of 11.5%. The Zacks Computers - IT Services industry declined 10.6% in the same time frame.

VRT Stock Performance

Image Source: Zacks Investment Research

Vertiv is benefiting from an extensive product portfolio, which spans thermal systems, liquid cooling, UPS, switchgear, busbar, and modular solutions, which is noteworthy. In the trailing 12 months, organic orders grew approximately 11%, with a book-to-bill of 1.2 times for the second quarter of 2025, indicating a strong prospect. Backlog grew 7% sequentially and 21% year over year to $8.5 billion.

Vertiv Expands With NVDA and OKLO Deals

Vertiv is a leading provider of thermal and power management solutions for data centers that consume immense amounts of power. As the demand for efficient energy use in data centers is rising, VRT’s role has become increasingly vital, with innovation and strategic partnerships serving as key catalysts for driving the future of sustainable data center solutions.

Building on this momentum, in July 2025, Vertiv partnered with Oklo OKLO to co-develop advanced, modular power and thermal management solutions specifically designed for data centers powered by Oklo’s advanced nuclear reactors.

The collaboration will leverage steam and electricity from Oklo’s Aurora powerhouse to enhance energy efficiency, resilience, and environmental performance. Integrating Vertiv’s cooling systems with Oklo’s onsite nuclear heat and power, the companies aim to create reference designs for next-generation, high-performance, and AI-driven data centers.

Further expanding its portfolio with NVIDIA NVDA in May 2025, the company confirmed its alignment with NVIDIA’s AI roadmap to deploy 800 VDC power architectures ahead of NVIDIA Kyber and Rubin Ultra platforms.

Vertiv aims to stay one GPU generation ahead of NVIDIA, providing efficient and scalable power solutions for next-generation AI data centers. The partnership highlights Vertiv’s commitment to supporting NVIDIA’s evolving compute demands with advanced power and cooling infrastructure.

VRT Raises 2025 Guidance

Vertiv is benefiting from its strong portfolio and rich partner base, which will continue to benefit the company’s top-line growth.

For 2025, revenues are now expected to be between $9.925 billion and $10.075 billion. Organic net sales growth is expected to be between 23% and 25%.

VRT expects 2025 non-GAAP earnings between $3.75 per share and $3.85 per share.

For third-quarter 2025, revenues are expected to be between $2.510 billion and $2.590 billion. Organic net sales are expected to increase in the 20% to 24% range.

VRT expects third-quarter 2025 non-GAAP earnings between 94 cents and $1.00 per share.

VRT’s Earnings Estimates Revisions Are Steady

The Zacks Consensus Estimate for third-quarter 2025 earnings is currently pegged at 96 cents per share, which has increased by a penny over the past 30 days. The figure indicates a year-over-year increase of 26.32%.

The Zacks Consensus Estimate for Vertiv’s 2025 revenues is pegged at $9.47 billion, suggesting growth of 18.22% year over year.

The Zacks Consensus Estimate for 2025 earnings is currently pegged at $3.57 per share, which has increased by a penny over the past 30 days. This indicates a 25.26% increase from the 2024 reported figure.

Vertiv Holdings Co. Price and Consensus

Vertiv Holdings Co. price-consensus-chart | Vertiv Holdings Co. Quote

VRT Suffers From Stiff Competition

Despite Vertiv’s expanding portfolio and partner base, Vertiv’s AI infrastructure solutions face increasing competition from Super Micro Computer SMCI and Hewlett-Packard Enterprise, both of which are expanding their capabilities to serve hyperscale and enterprise AI data center deployments.

Super Micro Computer is strengthening its position with end-to-end AI rack-scale systems that integrate compute, networking, storage, and liquid cooling. Super Micro Computer shares have appreciated 93.5% in the year-to-date period.

Vertiv Stock is Trading at a Premium

Vertiv is currently overvalued, as suggested by a Value Score of D.

In terms of the trailing 12-month Price/Book, Vertiv is currently trading at 20.81X, compared with the broader Computer and Technology sector’s 10.62X.

VRT Valuation

Image Source: Zacks Investment Research

Conclusion: Hold Vertiv Stock for Now

Vertiv is benefiting from its strong portfolio and rich partner base, which are driving order growth. However, a challenging macroeconomic environment, including the uncertainty created by higher tariffs, does not bode well for Vertiv’s profitability. Stiff competition and stretched valuation also remain a concern that makes VRT stock a risky bet.

VRT currently has a Zacks Rank #3 (Hold), which implies that investors should wait for a more favorable entry point to accumulate the stock. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

NVIDIA Corporation (NVDA): Free Stock Analysis Report

Super Micro Computer, Inc. (SMCI): Free Stock Analysis Report

Vertiv Holdings Co. (VRT): Free Stock Analysis Report

Oklo Inc. (OKLO): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Contact Us

Contact Number : +852 3852 8500Service Email : service@webull.hkBusiness Cooperation : marketinghk@webull.hkWebull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English