Does Autohome’s (ATHM) Aggressive Buyback Reflect Strategic Flexibility or Uncertain Growth Prospects?

- Autohome Inc. recently announced its second-quarter 2025 results, reporting revenue of CNY 1.76 billion and net income of CNY 398.87 million, alongside the completion of a major share buyback totaling approximately US$142.4 million for 4.44% of shares outstanding.

- An interesting insight is that while sales figures increased year-on-year, both revenue and net income declined, highlighting shifts in the company's earnings composition and cost dynamics during this period.

- We’ll explore how Autohome’s earnings performance and completion of its large share buyback shape the company’s forward-looking investment narrative.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

Autohome Investment Narrative Recap

To be an Autohome shareholder today, you need confidence in China's ongoing digital transformation of auto retail and the company's ability to expand its online-to-offline ecosystem. The latest earnings show weaker net income and revenue despite sales growth, but these results do not materially shift the short-term focus: improving margins through technology and widening enterprise services. The clearest risk remains cost pressures and margin volatility if industry price wars or customer concentration persist.

Among recent corporate actions, the just-completed share buyback, totaling US$142.4 million for 4.44% of outstanding shares, is the most relevant here. It signals ongoing capital returns to investors but does not offset the immediate earnings pressure that matters most for sentiment and near-term catalysts.

In contrast, investors should be aware that margin compression tied to escalating operational costs and increasing market competition could still impact...

Read the full narrative on Autohome (it's free!)

Autohome's narrative projects CN¥7.6 billion revenue and CN¥1.8 billion earnings by 2028. This requires 3.8% yearly revenue growth and a CN¥0.3 billion earnings increase from CN¥1.5 billion today.

Uncover how Autohome's forecasts yield a $28.87 fair value, in line with its current price.

Exploring Other Perspectives

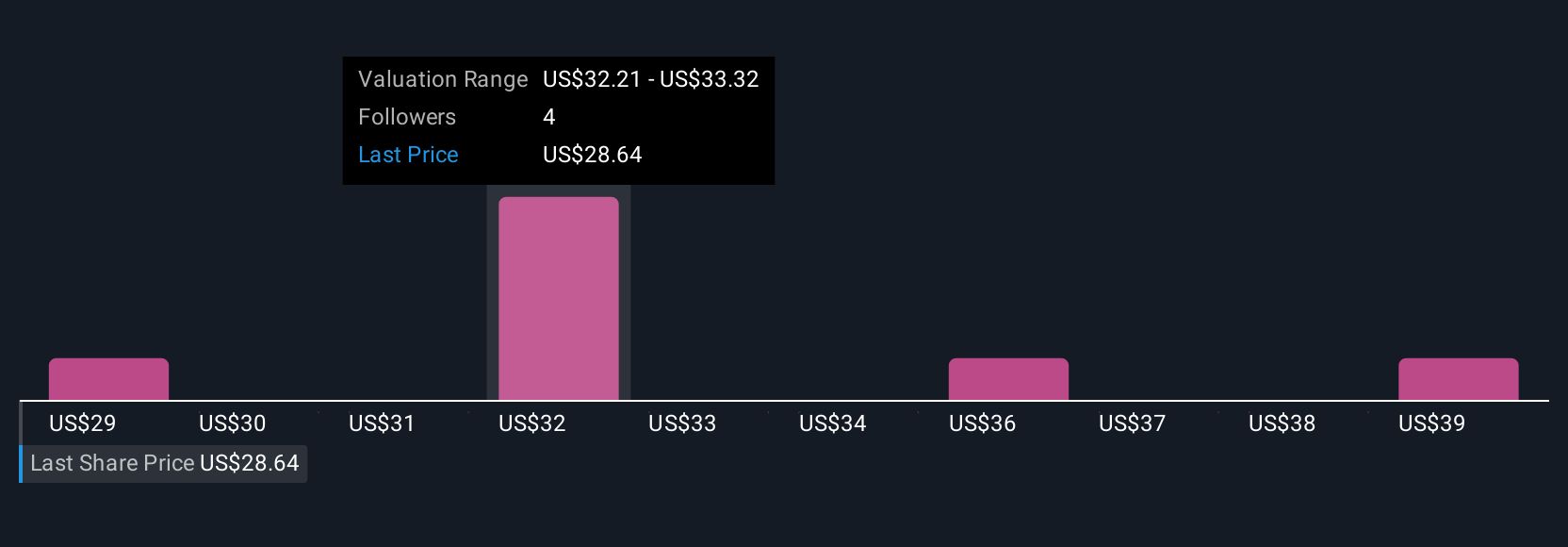

The Simply Wall St Community submitted four fair value estimates for Autohome, ranging widely from US$28.87 to US$40. While viewpoints on value differ, current challenges around margin compression may shape how you interpret these signals, and whether earnings stability will follow. Consider exploring these perspectives to compare priorities and risks with your own.

Explore 4 other fair value estimates on Autohome - why the stock might be worth as much as 35% more than the current price!

Build Your Own Autohome Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Autohome research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Autohome research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Autohome's overall financial health at a glance.

Ready For A Different Approach?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- AI is about to change healthcare. These 25 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 18 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- Rare earth metals are the new gold rush. Find out which 27 stocks are leading the charge.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number : +852 3852 8500Service Email : service@webull.hkBusiness Cooperation : marketinghk@webull.hkWebull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English