Do Wall Street Analysts Like Smurfit Westrock Stock?

Smurfit Westrock Plc (SW), headquartered in Dublin, Ireland, manufactures, distributes, and sells containerboard, corrugated containers, and other paper-based packaging products. Valued at $23.1 billion by market cap, the company operates in 40 countries and taps into the expertise of over 100,000 people, providing its customers with the most diverse, innovative, and sustainable range of renewable and recyclable packaging solutions.

Shares of this packaging giant have underperformed the broader market over the past year. SW has gained 11.8% over this time frame, while the broader S&P 500 Index ($SPX) has rallied nearly 19%. In 2025, SW stock is down 16.2%, compared to the SPX’s 10% rise on a YTD basis.

Narrowing the focus, SW’s underperformance is also apparent compared to the Consumer Discretionary Select Sector SPDR Fund (XLY). The exchange-traded fund has gained about 29.1% over the past year. Moreover, the ETF’s 2.5% returns on a YTD basis outshine the stock’s double-digit losses over the same time frame.

On Jul. 30, SW reported its Q2 results, and its shares closed down more than 6% in the following trading session. Its revenue totaled $7.9 billion, up 167.4% year over year. The company’s loss per share came in at $0.05, down from $0.51 in the year-ago quarter.

For the current fiscal year, ending in December, analysts expect SW’s EPS to grow 16.8% to $2.43 on a diluted basis. The company’s earnings surprise history is disappointing. It missed the consensus estimates in three of the last four quarters while beating the forecast on another occasion.

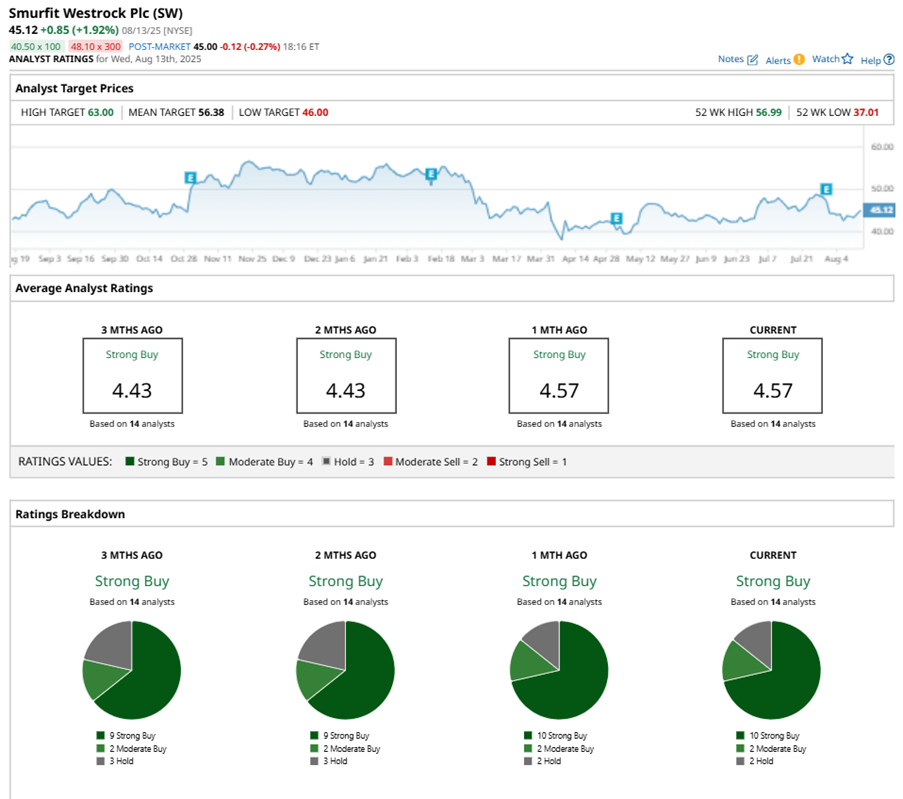

Among the 14 analysts covering SW stock, the consensus is a “Strong Buy.” That’s based on 10 “Strong Buy” ratings, two “Moderate Buys,” and two “Holds.”

This configuration is more bullish than two months ago, with nine analysts suggesting a “Strong Buy.”

On Aug. 4, Morgan Stanley (MS) analyst Brian Morgan maintained a “Buy” rating on SW and set a price target of $53, implying a potential upside of 17.5% from current levels.

The mean price target of $56.38 represents a 25% premium to SW’s current price levels. The Street-high price target of $63 suggests an ambitious upside potential of 39.6%.

On the date of publication, Neha Panjwani did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

Contact Us

Contact Number : +852 3852 8500Service Email : service@webull.hkBusiness Cooperation : marketinghk@webull.hkWebull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English