Astronics (ATRO) Is Up 9.6% After Raising Revenue Guidance and Posting Turnaround Profit—What's Changed

- Astronics Corporation recently reported its second quarter 2025 results, posting sales of US$204.68 million and a net income of US$1.31 million, while also raising the lower end of its full-year revenue guidance to a range of US$840 million to US$860 million.

- An interesting insight is that for the first six months of 2025, Astronics recorded a turnaround from a net loss a year ago to a net profit of US$10.84 million, reflecting improved operating performance and business momentum.

- To understand how Astronics’ increased revenue outlook shapes its long-term outlook, we’ll now examine its updated investment narrative.

We've found 19 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

Astronics Investment Narrative Recap

To own Astronics, you need to believe in the continued recovery of commercial aerospace and the company’s ability to benefit from rising aircraft production and demand for cabin technology. The company’s raised revenue guidance suggests positive momentum for the short-term catalyst of major aircraft production ramps, while the main risk, execution problems in its Test segment, remains unchanged as the latest results did not materially address this challenge.

Among recent announcements, Astronics’ inclusion in multiple Russell growth indices stands out. This could help support market interest as the company pursues its growth initiatives, but index inclusion alone does not mitigate fundamentals-based risks or shift the short-term outlook.

However, investors should be aware that despite higher revenues, persistent execution risk in the Test segment remains unresolved and...

Read the full narrative on Astronics (it's free!)

Astronics' narrative projects $956.5 million revenue and $86.1 million earnings by 2028. This requires 5.1% yearly revenue growth and a $89.8 million earnings increase from the current -$3.7 million.

Uncover how Astronics' forecasts yield a $38.58 fair value, a 15% upside to its current price.

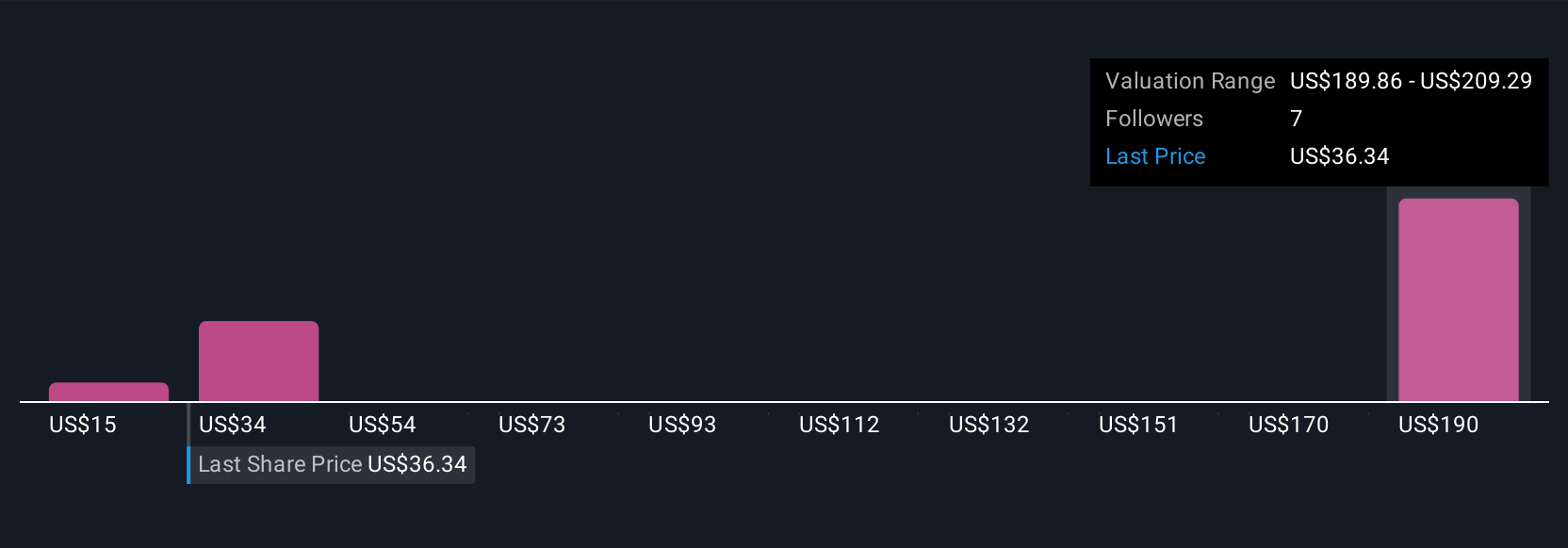

Exploring Other Perspectives

Three members of the Simply Wall St Community estimated Astronics’ fair value from US$15 up to US$208 per share, a striking spread. While revenue momentum appears strong, ongoing execution risk in the Test segment could weigh on results, so review several perspectives to form a balanced outlook.

Explore 3 other fair value estimates on Astronics - why the stock might be worth over 6x more than the current price!

Build Your Own Astronics Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Astronics research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Astronics research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Astronics' overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- AI is about to change healthcare. These 27 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Outshine the giants: these 19 early-stage AI stocks could fund your retirement.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 28 best rare earth metal stocks of the very few that mine this essential strategic resource.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number : +852 3852 8500Service Email : service@webull.hkBusiness Cooperation : marketinghk@webull.hkWebull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English