Globalstar (GSAT) Valuation in Focus After Government Contract Wins and Defense Sector Expansion

Globalstar (GSAT) has been turning heads after clinching a series of new government contracts and unveiling strategic partnerships, including a notable collaboration with the U.S. Army. The company is leveraging its Low Earth Orbit satellite constellation and advanced networking technologies to supply essential communications solutions for defense and government clients. This activity is not just about headlines, as management confirmed at least $60 million in new contract revenue over the next five years. This development adds to a broader narrative around Globalstar’s expanding government and defense pipeline.

In this context, Globalstar’s stock has quietly climbed around 20% over the past year, showing a stretch of building momentum that stands out after a lackluster start to 2024. For longer-term holders, it serves as a reminder that investments in capacity, such as the recently announced ground station expansion in Singapore, do not always pay off overnight. This year’s swing follows significant volatility and contrasts with a weak three-year total return, suggesting a change in how the market perceives Globalstar’s risk and growth profile.

After a year of gains and several government deals, it remains to be seen whether the market is already pricing in all of Globalstar’s future potential, or if there is still opportunity for investors interested in long-term growth.

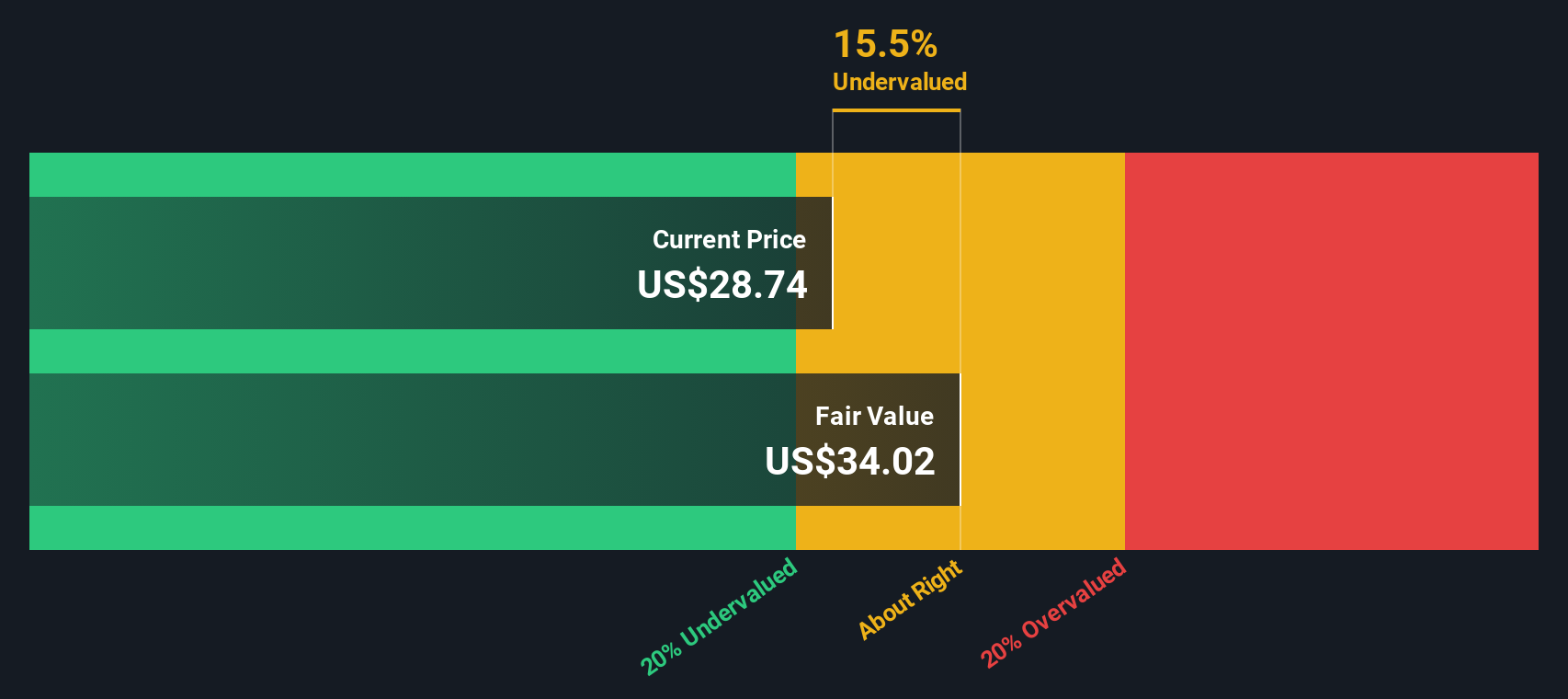

Most Popular Narrative: 49% Undervalued

According to community narrative, Globalstar is currently trading at a significant discount to its fair value, as analysts point to robust long-term growth drivers. The valuation reflects expectations of major improvements in earnings and profit margins, fueled by strategic expansion and technological upgrades.

Ongoing upgrades to ground infrastructure, and the deployment of next-generation satellites (C-3 system and new launches with SpaceX), will boost network capacity, reach, and performance. This will enable Globalstar to meet rising demand for hybrid and direct-to-device solutions, supporting long-term service revenue and higher discretionary earnings.

Want to know what’s turning heads among analysts? This valuation is built on bold revenue and earnings leaps in the years ahead. Are future profits being valued like high-growth startups? Get the inside story behind the numbers that make this price target so ambitious. There is plenty hidden beneath the headline.

Result: Fair Value of $52.5 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.However, persistent high capital expenditures or extended sales cycles could threaten Globalstar’s ability to deliver on its ambitious growth and profit projections.

Find out about the key risks to this Globalstar narrative.Another View: A Different Valuation Angle

Looking at Globalstar from a different angle, the SWS DCF model tells a similar story. It suggests the shares are trading below fair value based on future cash flow estimates. Does this reinforce the growth story, or is the market missing something?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Globalstar Narrative

If you see things differently or would rather dig into the details yourself, you can put together your own view in just a few minutes. do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Globalstar.

Looking for Your Next Winning Investment?

Smart investors never settle for just one opportunity. You can boost your odds by checking out carefully curated stock ideas our team has handpicked for their standout potential. Here is how you can take action right now and position yourself to capture tomorrow’s gains:

- Capture stable income by seeking dividend stocks with yields > 3% that consistently outperform with steady payouts and robust financial fundamentals.

- Ride the wave of technology change and tap into AI penny stocks poised to benefit from breakthroughs in artificial intelligence across global industries.

- Maximize value for your portfolio by targeting strong undervalued stocks based on cash flows that seasoned investors are watching for their potential to deliver outsized returns based on future cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number : +852 3852 8500Service Email : service@webull.hkBusiness Cooperation : marketinghk@webull.hkWebull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English