General Dynamics (GD): Assessing Valuation After Strong Q2 Earnings Beat and Surging Order Backlog

General Dynamics (GD) just delivered a second-quarter update that is hard for investors to ignore. Not only did the company report earnings per share and revenues that topped expectations, but it also revealed a massive jump in its order backlog, now at $103.68 billion compared to $88.66 billion in the previous quarter. This kind of backlog expansion signals that demand remains strong, and it is the sort of operational story that can shift how investors view the company’s future growth.

This upbeat report came on the back of steady, if sometimes underappreciated, price momentum. Over the past year, General Dynamics shares have climbed 12%, with an increase of nearly 15% in the past 3 months as confidence seems to be building. While General Dynamics has been the topic of bullish estimate revisions lately, previous growth in both revenue and net income helps explain why the stock continues to attract buyers after its recent reports. In the context of a five-year total return of 140%, forward-looking optimism appears to be building.

After this earnings-fueled run, investors may be wondering if there is still an opportunity to pick up General Dynamics at a discount, or if the market is already factoring in all of its future potential.

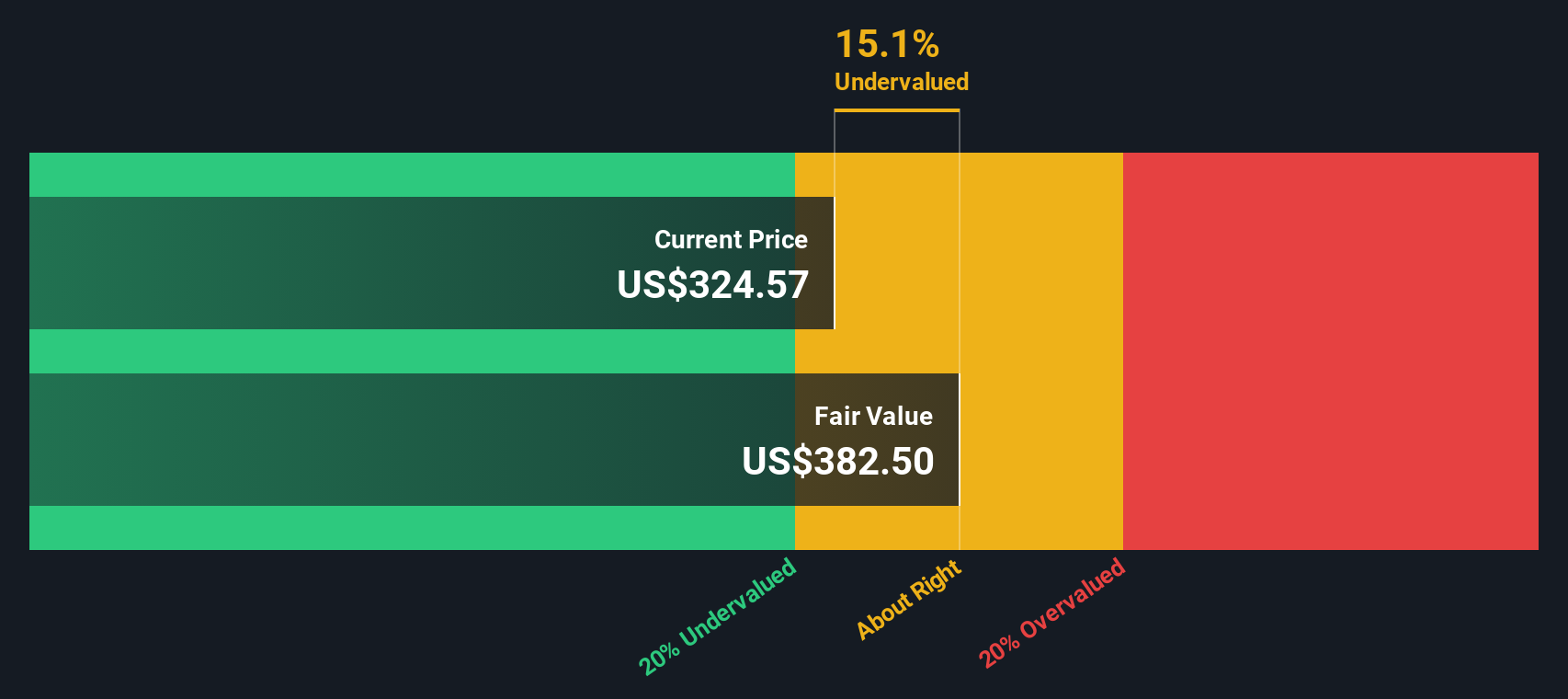

Most Popular Narrative: 4.1% Undervalued

According to community narrative, General Dynamics is currently considered undervalued, with its fair value estimated to be slightly above the recent trading price. Analysts highlight ongoing catalysts and robust growth expectations as key drivers behind this assessment.

Expansion of the Electric Boat program, along with significant new contracts for advanced submarines and additional support from higher U.S. Navy funding and industrial base investments, is expected to position the Marine Systems segment for sustained sales growth and realization of operating leverage. This could benefit both top and bottom-line results over the long term.

Curious about why analysts see more upside ahead? The answer may lie in a detailed set of financial projections and margin targets that most investors overlook. If you want a glimpse into the underlying calculations and forward-looking assumptions supporting this narrative, you may want to see what expectations are being priced in.

Result: Fair Value of $333.41 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.However, supply chain challenges and shifts in defense technology demand could quickly alter General Dynamics' growth trajectory, which may impact future earnings expectations.

Find out about the key risks to this General Dynamics narrative.Another View: What Does Discounted Cash Flow Say?

While the fair value estimate is based on analyst consensus and future earnings, our DCF model offers a different approach to valuation. This method also points to the company being undervalued. However, do both really agree on what matters most?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own General Dynamics Narrative

If you want to dig into the numbers or have your own perspective on where General Dynamics is headed, you can create a personalized view of the story in just a few minutes. Simply do it your way.

A good starting point is our analysis highlighting 5 key rewards investors are optimistic about regarding General Dynamics.

Looking for more investment ideas?

Now is the perfect time to keep your momentum going and uncover fresh investment opportunities that fit your goals. Let Simply Wall Street point you to hand-picked strategies that could put you ahead of the curve. Don’t miss out on these potential winners. Your next top idea might be one click away.

- Accelerate your search for strong, high-yield portfolios by checking out companies offering dividend stocks with yields > 3%. These options can add stability and income to your investments.

- Seize the potential of healthcare innovations by spotting leaders among healthcare AI stocks. These companies are shaping the next generation of medical breakthroughs with artificial intelligence.

- Power your strategy with emerging trends by exploring cryptocurrency and blockchain stocks. These opportunities are positioned to benefit from the rise of blockchain and digital assets in the financial world.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number : +852 3852 8500Service Email : service@webull.hkBusiness Cooperation : marketinghk@webull.hkWebull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English