TTM Technologies (TTMI): Evaluating Valuation Following CEO Transition to Dr. Edwin Roks

TTM Technologies (TTMI) is attracting attention this week following the announcement that Dr. Edwin Roks will assume the role of CEO, succeeding Thomas Edman, who has led the company since 2014. Dr. Roks brings extensive industry expertise from his tenure at Teledyne Technologies, where he oversaw digital imaging growth and managed major integrations. Investors are closely monitoring this leadership transition, viewing it as a sign that TTM is focusing more on expanding in aerospace, defense, and industrial electronics—sectors in which Dr. Roks has significant experience.

Management changes are not the only developments; the stock itself has delivered notable gains, rising 120% over the past year and increasing nearly 81% year-to-date. Although there was a slight decline in the past month, momentum has strengthened since the spring. This positive trend coincides with the company maintaining steady revenue growth and achieving a substantial increase in net income, developments that are contributing to market optimism regarding the potential impact of a new strategic direction for TTM.

The main question now is clear: with this leadership change and significant stock performance, is TTM Technologies trading at a discount, or has the market already anticipated what may come next?

Most Popular Narrative: 21.7% Undervalued

According to community narrative, TTM Technologies is considered significantly undervalued, with market price trailing behind consensus fair value based on ambitious forward projections.

Large-scale data center buildouts announced by tech giants (e.g., Google, CoreWeave, Meta) and TTM's new Wisconsin facility position the company to capture outsized demand for advanced PCBs and interconnects required for AI and cloud infrastructure. This is seen as directly supporting revenue growth and long-term customer relationships. Sustained increases in U.S. and NATO defense spending plans, alongside TTM's deep strategic alignment and $1.46 billion A&D backlog, are viewed as providing long-term visibility and stability for high-margin revenue streams. This may improve the predictability of forward earnings and support ongoing margin expansion.

Want to know why analysts are bullish on TTM's valuation? The future price is built on assumptions of robust earnings growth, fatter profit margins, and higher profitability than many industry peers. What ambitious financial projections power this target? The full narrative uncovers the surprising calculations and market expectations fueling this bullish consensus.

Result: Fair Value of $56.75 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.However, risks remain. TTM faces ongoing customer concentration and slower-than-expected facility ramp-ups, both of which could challenge expected margin improvements and earnings growth.

Find out about the key risks to this TTM Technologies narrative.Another View: SWS DCF Model Raises Different Questions

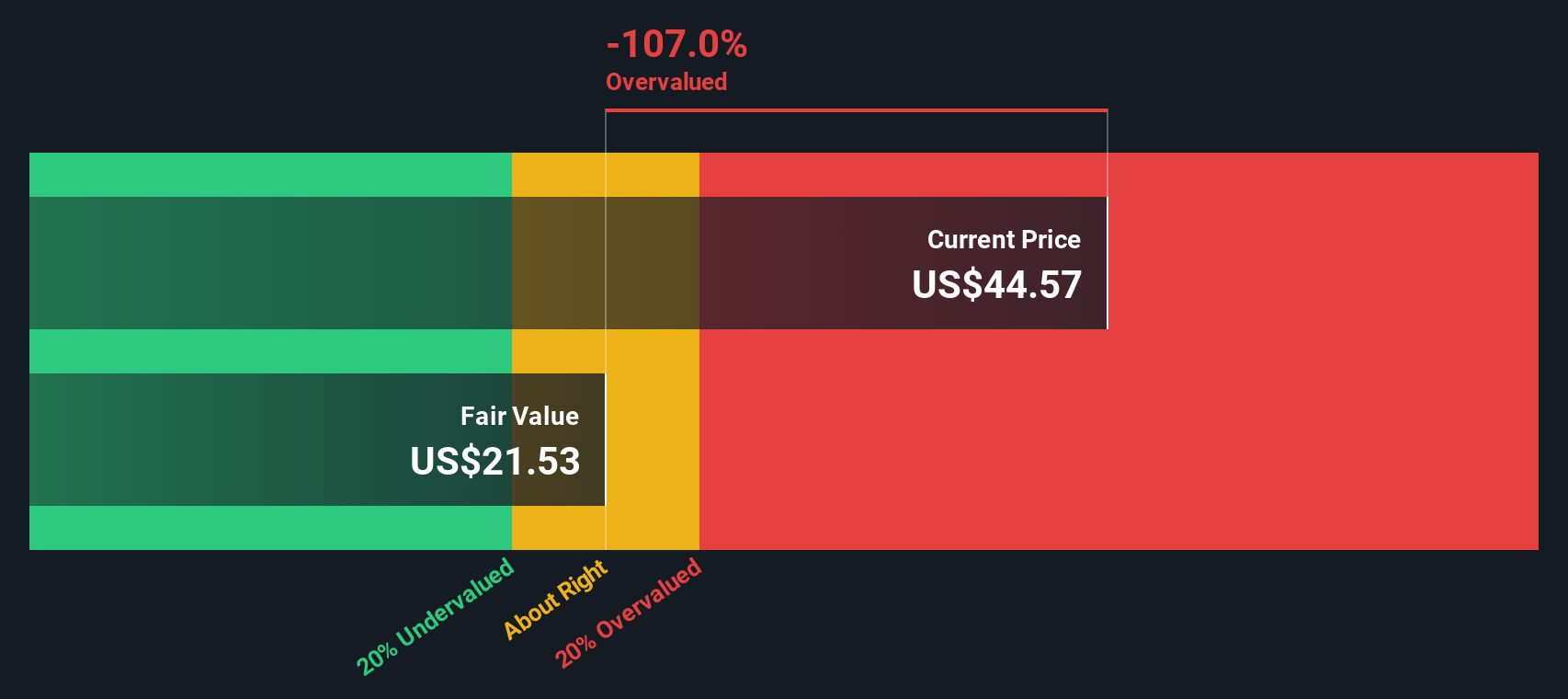

Looking at things from a different perspective, our DCF model suggests TTM Technologies may actually be overvalued. This view stands in stark contrast to the bullish outlook based on projected earnings and market optimism. Which perspective is closer to reality? Is it a growth-driven fair value, or is the market price already ahead of itself?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own TTM Technologies Narrative

If these views do not align with your own, or you prefer to analyze the numbers yourself, you can quickly assemble your own take in just minutes. do it your way.

A great starting point for your TTM Technologies research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for More Smart Investment Opportunities?

You have seen how TTM Technologies stacks up, but why stop there? The market is full of potential, and the next winning idea could be just a click away. Take charge of your investing strategy and get an edge with tailored ideas crafted for savvy investors like you:

- Capture consistent income by checking out dividend stocks with strong yields through dividend stocks with yields > 3%.

- Explore the wave of tomorrow’s breakthroughs by researching promising healthcare companies transforming medicine with artificial intelligence via healthcare AI stocks.

- Discover rare hidden gems among undervalued businesses based on their cash flow metrics when you use undervalued stocks based on cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number : +852 3852 8500Service Email : service@webull.hkBusiness Cooperation : marketinghk@webull.hkWebull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English