Is Watts International Maritime (HKG:2258) Using Debt In A Risky Way?

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We can see that Watts International Maritime Company Limited (HKG:2258) does use debt in its business. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

What Is Watts International Maritime's Net Debt?

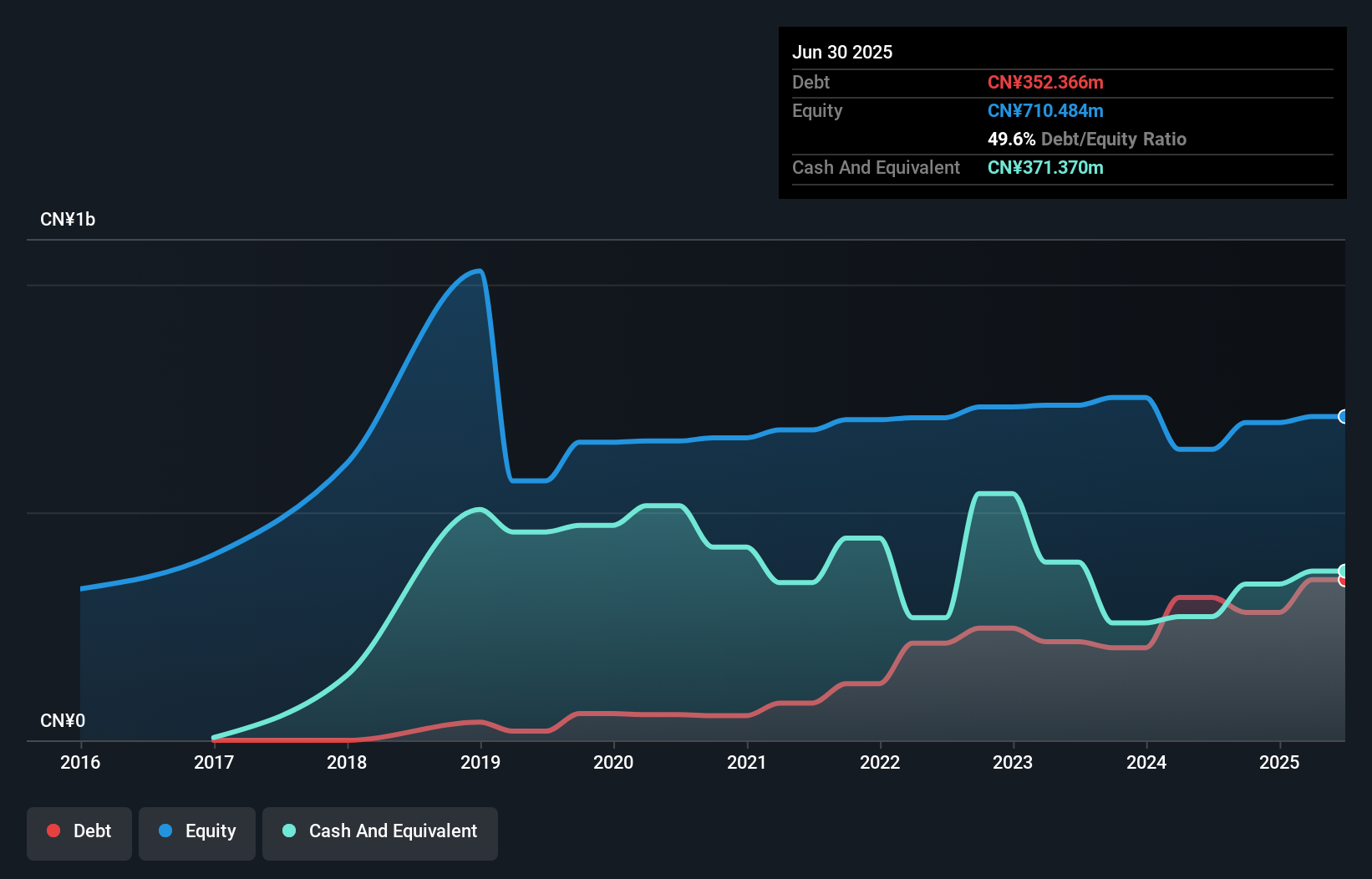

You can click the graphic below for the historical numbers, but it shows that as of June 2025 Watts International Maritime had CN¥352.4m of debt, an increase on CN¥313.7m, over one year. But on the other hand it also has CN¥371.4m in cash, leading to a CN¥19.0m net cash position.

How Strong Is Watts International Maritime's Balance Sheet?

The latest balance sheet data shows that Watts International Maritime had liabilities of CN¥2.48b due within a year, and liabilities of CN¥111.4m falling due after that. On the other hand, it had cash of CN¥371.4m and CN¥2.04b worth of receivables due within a year. So its liabilities total CN¥175.8m more than the combination of its cash and short-term receivables.

When you consider that this deficiency exceeds the company's CN¥162.4m market capitalization, you might well be inclined to review the balance sheet intently. Hypothetically, extremely heavy dilution would be required if the company were forced to pay down its liabilities by raising capital at the current share price. Given that Watts International Maritime has more cash than debt, we're pretty confident it can handle its debt, despite the fact that it has a lot of liabilities in total. The balance sheet is clearly the area to focus on when you are analysing debt. But you can't view debt in total isolation; since Watts International Maritime will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

View our latest analysis for Watts International Maritime

In the last year Watts International Maritime had a loss before interest and tax, and actually shrunk its revenue by 14%, to CN¥1.6b. We would much prefer see growth.

So How Risky Is Watts International Maritime?

While Watts International Maritime lost money on an earnings before interest and tax (EBIT) level, it actually booked a paper profit of CN¥70m. So when you consider it has net cash, along with the statutory profit, the stock probably isn't as risky as it might seem, at least in the short term. Given the lack of transparency around future revenue (and cashflow), we're nervous about this one, until it makes its first big sales. To us, it is a high risk play. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. Be aware that Watts International Maritime is showing 3 warning signs in our investment analysis , and 1 of those is concerning...

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English