Synchrony's Health & Wellness Bet: A Long-Term Growth Catalyst?

Consumer financial services giant Synchrony Financial SYF is steadily strengthening its footprint in the Health & Wellness space through its CareCredit brand, a move that could power sustained expansion in the years ahead. With an aging U.S. population and rising demand for health-related financing, the company is positioning itself in one of the most resilient spending categories.

Spending on health is expected to hit $5.6 trillion this year and climb to $8.6 trillion by 2033, according to the Centers for Medicare and Medicaid Services. Synchrony is tapping this opportunity by broadening its portfolio across areas such as audiology, dental, veterinary and general wellness. Average active accounts in Health & Wellness rose 13.3% in 2023, 8% in 2024, and a modest 0.7% in the first half of 2025, while interest and fees on loans advanced 13.6% last year and another 3.2% in 1H25, underscoring steady momentum.

At the end of the second quarter, 15% of Synchrony’s loan receivables were tied to Health & Wellness. Its provider network surpassed 285,000 locations by 2024-end, and with no single partner (excluding the Walgreens program agreement) accounting for more than 0.6% of total interest and fees, the platform benefits from both scale and diversification. Importantly, much of the CareCredit network’s purchase volume comes from repeat customers, highlighting strong stickiness.

Still, long-term success will depend on Synchrony’s ability to manage credit risk, underwriting discipline and regulatory scrutiny. With its expanding network, strategic partnerships and growing demand tailwinds, Health & Wellness looks well-positioned to serve as a long-term growth catalyst for Synchrony.

How Are SYF’s Peers Faring?

Peers of SYF, including American Express Company AXP and Ally Financial Inc. ALLY, are also seeing growth in receivables and interest income.

American Express’ total loans and card member receivables grew 6% year over year in the second quarter of 2025, while its interest on loans advanced 11%. AmEx’s focus on Millennials and Gen-Z consumers will likely boost the figures. Meanwhile, Ally Financial’s total net finance receivables and loans amounted to $129.8 billion at second-quarter-end. The company’s net financing revenues grew to $1.53 billion in the second quarter.

Synchrony’s Price Performance, Valuation and Estimates

SYF shares have gained 17.8% year to date, outperforming the industry’s 5% increase.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

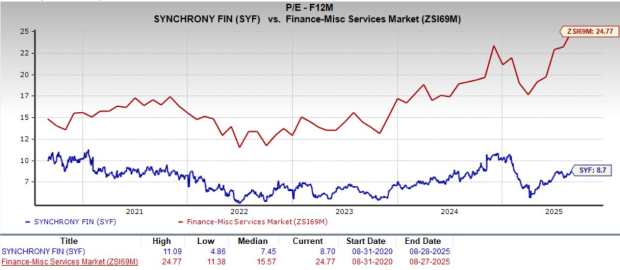

From a valuation standpoint, Synchrony trades at a forward price-to-earnings ratio of 8.70, down from the industry average of 24.77. SYF carries a Value Score of A.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

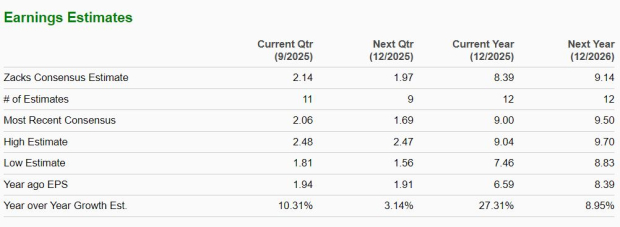

The Zacks Consensus Estimate for Synchrony’s 2025 earnings is pegged at $8.39 per share, implying a 27.3% jump from the year-ago period.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

The stock currently carries a Zacks Rank #3 (Hold).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks Names #1 Semiconductor Stock

This under-the-radar company specializes in semiconductor products that titans like NVIDIA don't build. It's uniquely positioned to take advantage of the next growth stage of this market. And it's just beginning to enter the spotlight, which is exactly where you want to be.

With strong earnings growth and an expanding customer base, it's positioned to feed the rampant demand for Artificial Intelligence, Machine Learning, and Internet of Things. Global semiconductor manufacturing is projected to explode from $452 billion in 2021 to $971 billion by 2028.

See This Stock Now for Free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

American Express Company (AXP): Free Stock Analysis Report

Ally Financial Inc. (ALLY): Free Stock Analysis Report

Synchrony Financial (SYF): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Contact Us

Contact Number : +852 3852 8500Service Email : service@webull.hkBusiness Cooperation : marketinghk@webull.hkWebull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English