Skechers (SKX): Taking Stock of Valuation After Recent Share Price Moves

Is Skechers U.S.A (SKX) on your watchlist again? Sometimes, even with no glaring headlines or dramatic announcements, a stock’s recent moves can catch your attention and leave you wondering what is driving the action. For Skechers, there has not been a major event sparking headlines this week. However, the pattern in its price may have investors thinking carefully about what the future holds for this footwear powerhouse.

Looking at the past year, Skechers shares have edged down just over 4%, reflecting some added caution by the market in recent months. This comes even as the company’s longer-term performance still stands out: the stock is up more than sixfold over the past three years and has nearly doubled in the last five years. While momentum has slowed lately, the broader growth story is hard to ignore.

The big question is whether investors are seeing a bargain forming or if the market has already priced in what is coming next for Skechers. Could this be a chance to step in, or is more patience needed?

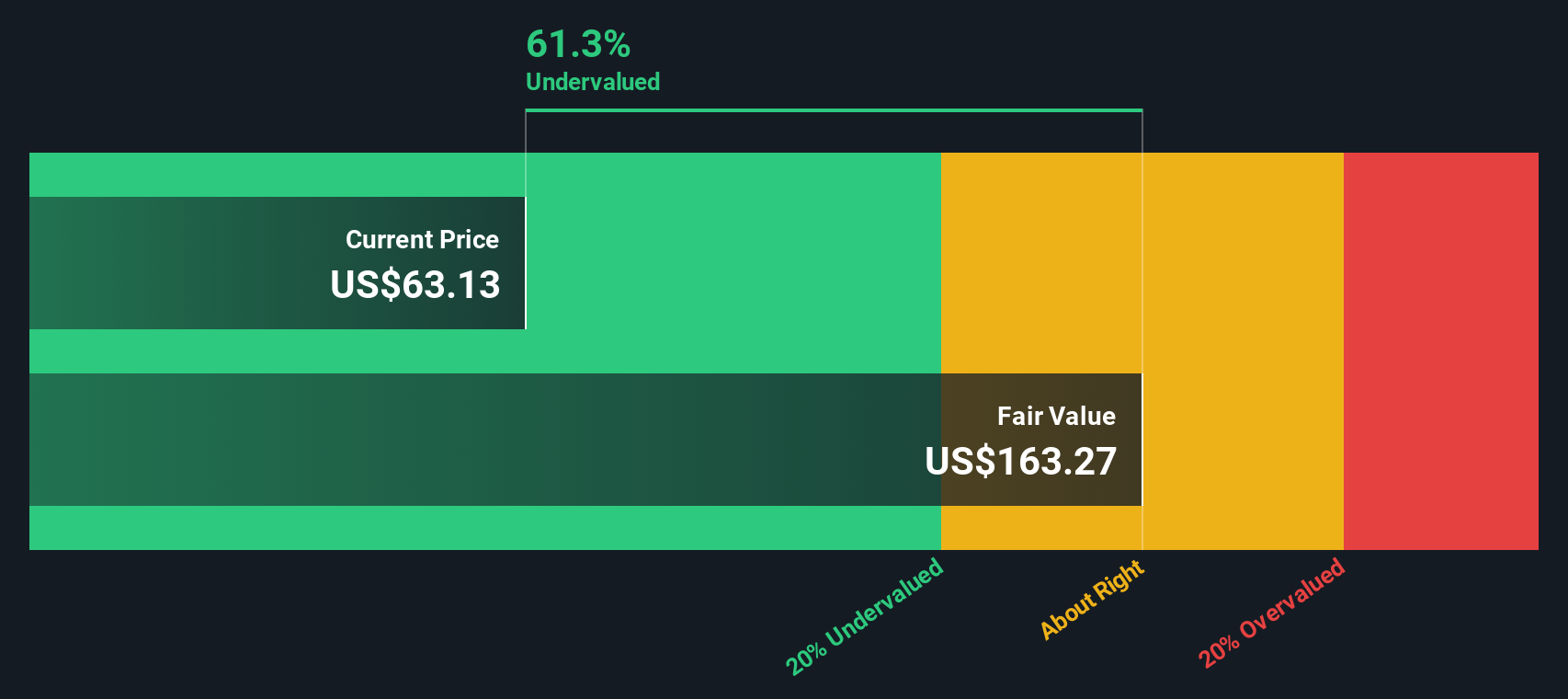

Most Popular Narrative: Fairly Valued

According to the most widely followed narrative, Skechers U.S.A. is trading very close to its fair value, based on future growth prospects, profit margins, and sector risks.

Skechers' focus on international expansion, particularly in EMEA and Americas, and their heavy investment in retail store network and distribution efficiencies are positioned to drive revenue growth. International sales are highlighted as a key growth engine.

Want to uncover the hidden blueprint behind what makes this valuation tick? Analysts are betting on ambitious revenue growth, bold international strategies, and a direct-to-consumer pivot that could transform margins. Which key financial assumptions anchor this thesis? Dive deeper for the full story behind their target price.

Result: Fair Value of $62.3 (ABOUT RIGHT)

Have a read of the narrative in full and understand what's behind the forecasts.However, a shift in tariffs or weakening consumer demand could disrupt these growth assumptions and challenge the optimism around Skechers' fair value.

Find out about the key risks to this Skechers U.S.A narrative.Another View: What About the SWS DCF Model?

While many see Skechers as fairly priced based on earnings compared to its peers, our DCF model points in a different direction. It suggests the shares could be overvalued when future cash flows are factored in. Which narrative captures the real story?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Skechers U.S.A Narrative

If you are not convinced by the prevailing views or like to crunch the numbers yourself, you can build your own narrative quickly and easily with Do it your way.

A great starting point for your Skechers U.S.A research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Smart Investment Opportunities?

Stay ahead by looking beyond Skechers and find companies that truly fit your goals. The right strategy today could mean extraordinary results tomorrow.

- Uncover growth potential with undervalued stocks based on cash flows and see which businesses offer compelling value based on cash flows right now.

- Get in early on tomorrow’s tech trailblazers by checking out leaders harnessing artificial intelligence with AI penny stocks.

- Secure steady income for your portfolio when you target reliable high-yield opportunities via dividend stocks with yields > 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English