Capital Allocation Trends At Chanhigh Holdings (HKG:2017) Aren't Ideal

When it comes to investing, there are some useful financial metrics that can warn us when a business is potentially in trouble. When we see a declining return on capital employed (ROCE) in conjunction with a declining base of capital employed, that's often how a mature business shows signs of aging. Ultimately this means that the company is earning less per dollar invested and on top of that, it's shrinking its base of capital employed. In light of that, from a first glance at Chanhigh Holdings (HKG:2017), we've spotted some signs that it could be struggling, so let's investigate.

What Is Return On Capital Employed (ROCE)?

For those that aren't sure what ROCE is, it measures the amount of pre-tax profits a company can generate from the capital employed in its business. Analysts use this formula to calculate it for Chanhigh Holdings:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

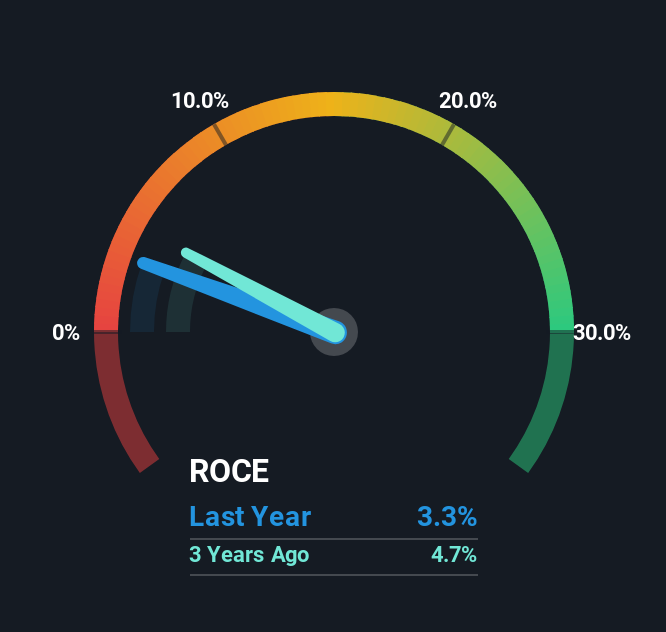

0.033 = CN¥34m ÷ (CN¥2.1b - CN¥1.1b) (Based on the trailing twelve months to June 2025).

So, Chanhigh Holdings has an ROCE of 3.3%. In absolute terms, that's a low return and it also under-performs the Construction industry average of 4.9%.

See our latest analysis for Chanhigh Holdings

Historical performance is a great place to start when researching a stock so above you can see the gauge for Chanhigh Holdings' ROCE against it's prior returns. If you'd like to look at how Chanhigh Holdings has performed in the past in other metrics, you can view this free graph of Chanhigh Holdings' past earnings, revenue and cash flow.

How Are Returns Trending?

We are a bit worried about the trend of returns on capital at Chanhigh Holdings. About five years ago, returns on capital were 7.8%, however they're now substantially lower than that as we saw above. Meanwhile, capital employed in the business has stayed roughly the flat over the period. This combination can be indicative of a mature business that still has areas to deploy capital, but the returns received aren't as high due potentially to new competition or smaller margins. So because these trends aren't typically conducive to creating a multi-bagger, we wouldn't hold our breath on Chanhigh Holdings becoming one if things continue as they have.

On a side note, Chanhigh Holdings' current liabilities are still rather high at 52% of total assets. This effectively means that suppliers (or short-term creditors) are funding a large portion of the business, so just be aware that this can introduce some elements of risk. Ideally we'd like to see this reduce as that would mean fewer obligations bearing risks.

In Conclusion...

In summary, it's unfortunate that Chanhigh Holdings is generating lower returns from the same amount of capital. Investors haven't taken kindly to these developments, since the stock has declined 29% from where it was five years ago. That being the case, unless the underlying trends revert to a more positive trajectory, we'd consider looking elsewhere.

If you want to continue researching Chanhigh Holdings, you might be interested to know about the 1 warning sign that our analysis has discovered.

While Chanhigh Holdings isn't earning the highest return, check out this free list of companies that are earning high returns on equity with solid balance sheets.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English