The Price Is Right For East Buy Holding Limited (HKG:1797) Even After Diving 29%

The East Buy Holding Limited (HKG:1797) share price has softened a substantial 29% over the previous 30 days, handing back much of the gains the stock has made lately. Looking at the bigger picture, even after this poor month the stock is up 86% in the last year.

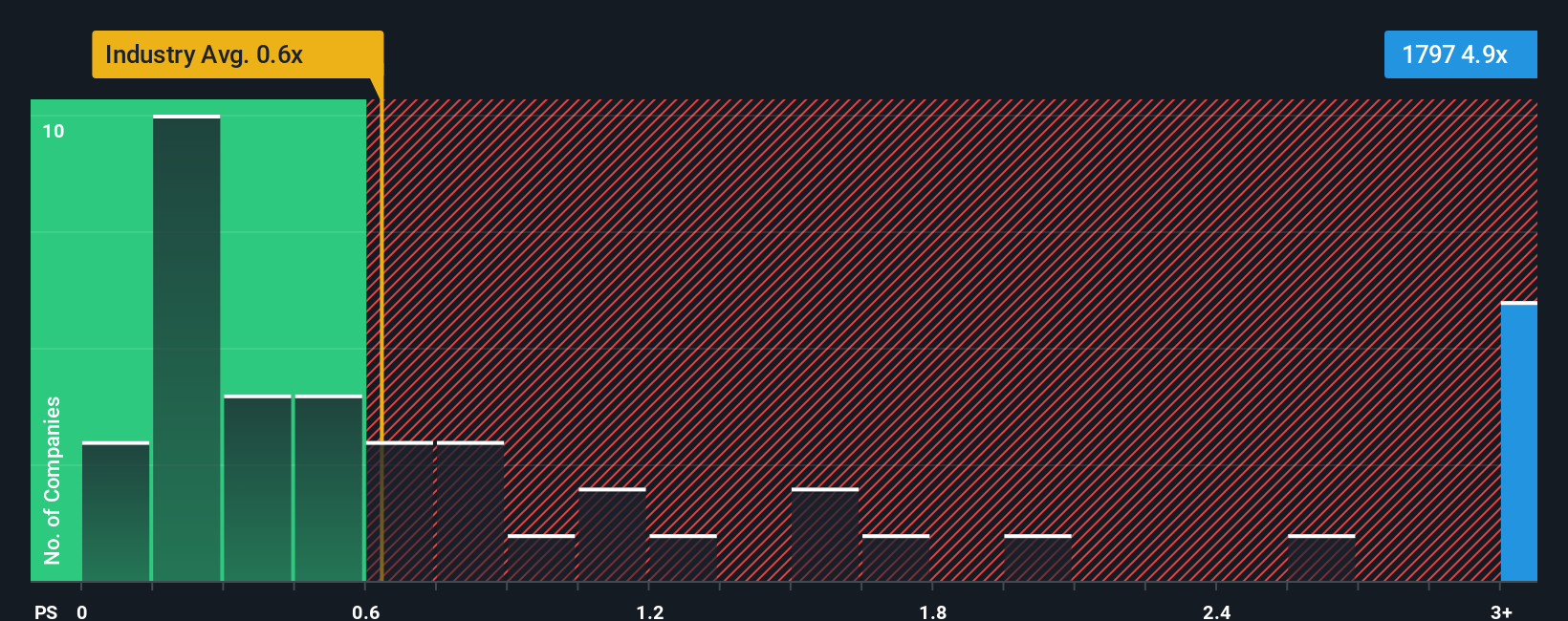

Even after such a large drop in price, you could still be forgiven for thinking East Buy Holding is a stock to steer clear of with a price-to-sales ratios (or "P/S") of 4.9x, considering almost half the companies in Hong Kong's Consumer Retailing industry have P/S ratios below 0.6x. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/S.

Check out our latest analysis for East Buy Holding

What Does East Buy Holding's Recent Performance Look Like?

While the industry has experienced revenue growth lately, East Buy Holding's revenue has gone into reverse gear, which is not great. It might be that many expect the dour revenue performance to recover substantially, which has kept the P/S from collapsing. However, if this isn't the case, investors might get caught out paying too much for the stock.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on East Buy Holding.Is There Enough Revenue Growth Forecasted For East Buy Holding?

The only time you'd be truly comfortable seeing a P/S as steep as East Buy Holding's is when the company's growth is on track to outshine the industry decidedly.

Taking a look back first, the company's revenue growth last year wasn't something to get excited about as it posted a disappointing decline of 33%. In spite of this, the company still managed to deliver immense revenue growth over the last three years. So while the company has done a great job in the past, it's somewhat concerning to see revenue growth decline so harshly.

Shifting to the future, estimates from the ten analysts covering the company suggest revenue should grow by 15% per year over the next three years. That's shaping up to be materially higher than the 12% per annum growth forecast for the broader industry.

With this in mind, it's not hard to understand why East Buy Holding's P/S is high relative to its industry peers. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

What Does East Buy Holding's P/S Mean For Investors?

East Buy Holding's shares may have suffered, but its P/S remains high. Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

We've established that East Buy Holding maintains its high P/S on the strength of its forecasted revenue growth being higher than the the rest of the Consumer Retailing industry, as expected. It appears that shareholders are confident in the company's future revenues, which is propping up the P/S. Unless these conditions change, they will continue to provide strong support to the share price.

And what about other risks? Every company has them, and we've spotted 3 warning signs for East Buy Holding you should know about.

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English