A Peek at Ameresco's Future Earnings

Ameresco (NYSE:AMRC) is gearing up to announce its quarterly earnings on Monday, 2025-11-03. Here's a quick overview of what investors should know before the release.

Analysts are estimating that Ameresco will report an earnings per share (EPS) of $0.29.

The announcement from Ameresco is eagerly anticipated, with investors seeking news of surpassing estimates and favorable guidance for the next quarter.

It's worth noting for new investors that guidance can be a key determinant of stock price movements.

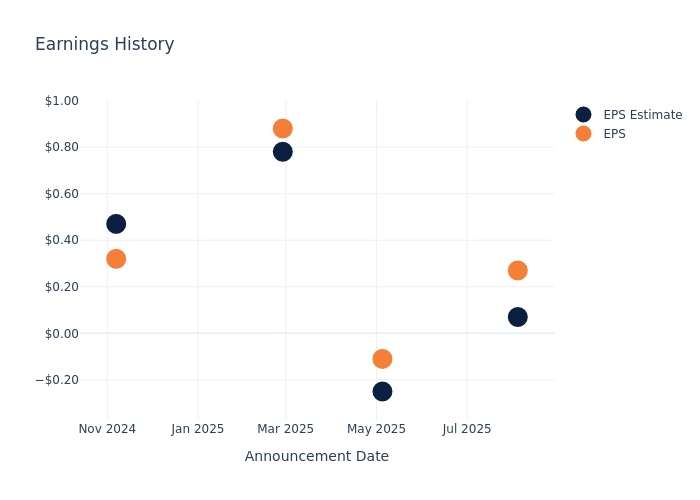

Historical Earnings Performance

During the last quarter, the company reported an EPS beat by $0.20, leading to a 48.98% increase in the share price on the subsequent day.

Here's a look at Ameresco's past performance and the resulting price change:

| Quarter | Q2 2025 | Q1 2025 | Q4 2024 | Q3 2024 |

|---|---|---|---|---|

| EPS Estimate | 0.07 | -0.25 | 0.78 | 0.47 |

| EPS Actual | 0.27 | -0.11 | 0.88 | 0.32 |

| Price Change % | 49.00 | 12.00 | -36.00 | -16.00 |

Performance of Ameresco Shares

Shares of Ameresco were trading at $38.97 as of October 30. Over the last 52-week period, shares are up 18.7%. Given that these returns are generally positive, long-term shareholders are likely bullish going into this earnings release.

Insights Shared by Analysts on Ameresco

For investors, staying informed about market sentiments and expectations in the industry is paramount. This analysis provides an exploration of the latest insights on Ameresco.

Analysts have provided Ameresco with 4 ratings, resulting in a consensus rating of Buy. The average one-year price target stands at $32.25, suggesting a potential 17.24% downside.

Comparing Ratings with Competitors

The following analysis focuses on the analyst ratings and average 1-year price targets of Legence, Centuri Holdings and MYR Group, three prominent industry players, providing insights into their relative performance expectations and market positioning.

- Analysts currently favor an Buy trajectory for Legence, with an average 1-year price target of $37.54, suggesting a potential 3.67% downside.

- Analysts currently favor an Underperform trajectory for Centuri Holdings, with an average 1-year price target of $20.0, suggesting a potential 48.68% downside.

- Analysts currently favor an Neutral trajectory for MYR Group, with an average 1-year price target of $211.0, suggesting a potential 441.44% upside.

Analysis Summary for Peers

In the peer analysis summary, key metrics for Legence, Centuri Holdings and MYR Group are highlighted, providing an understanding of their respective standings within the industry and offering insights into their market positions and comparative performance.

| Company | Consensus | Revenue Growth | Gross Profit | Return on Equity |

|---|---|---|---|---|

| Ameresco | Buy | 7.83% | $73.36M | 1.26% |

| Legence | Buy | 15.00% | $128.67M | -1.94% |

| Centuri Holdings | Underperform | 7.73% | $67.80M | 1.46% |

| MYR Group | Neutral | 7.02% | $111.89M | 5.35% |

Key Takeaway:

Ameresco ranks highest in Revenue Growth among its peers. It also leads in Gross Profit margin. However, it has the lowest Return on Equity. Overall, Ameresco is positioned favorably compared to its peers in terms of financial performance metrics.

Unveiling the Story Behind Ameresco

Ameresco Inc provides energy efficiency solutions for facilities in North America and Europe. It focuses on projects that reduce energy, also focuses on the operations and maintenance costs of governmental, educational, utility, healthcare, and other institutional, commercial, and industrial entities facilities. Ameresco distributes solar energy products and systems, such as PV panels, solar regulators, solar charge controllers, inverters, solar-powered lighting systems, solar-powered water pumps, solar panel mounting hardware, and other system components. The company's segment includes U.S. Regions; U.S. Federal; Canada; Alternative Fuels; Non-Solar DG and All Other. It derives a majority of its revenue from the U.S. Regions segment.

Financial Milestones: Ameresco's Journey

Market Capitalization: Indicating a reduced size compared to industry averages, the company's market capitalization poses unique challenges.

Revenue Growth: Ameresco's revenue growth over a period of 3 months has been noteworthy. As of 30 June, 2025, the company achieved a revenue growth rate of approximately 7.83%. This indicates a substantial increase in the company's top-line earnings. As compared to competitors, the company encountered difficulties, with a growth rate lower than the average among peers in the Industrials sector.

Net Margin: Ameresco's net margin falls below industry averages, indicating challenges in achieving strong profitability. With a net margin of 2.72%, the company may face hurdles in effective cost management.

Return on Equity (ROE): Ameresco's ROE is below industry standards, pointing towards difficulties in efficiently utilizing equity capital. With an ROE of 1.26%, the company may encounter challenges in delivering satisfactory returns for shareholders.

Return on Assets (ROA): Ameresco's ROA is below industry standards, pointing towards difficulties in efficiently utilizing assets. With an ROA of 0.3%, the company may encounter challenges in delivering satisfactory returns from its assets.

Debt Management: The company faces challenges in debt management with a debt-to-equity ratio higher than the industry average. With a ratio of 1.82, caution is advised due to increased financial risk.

To track all earnings releases for Ameresco visit their earnings calendar on our site.

This article was generated by Benzinga's automated content engine and reviewed by an editor.

Contact Us

Contact Number : +852 3852 8500Service Email : service@webull.hkBusiness Cooperation : marketinghk@webull.hkWebull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English