Beijing North Star (SEHK:588) Losses Increase 61.5% Annually, Undercutting Value Narrative

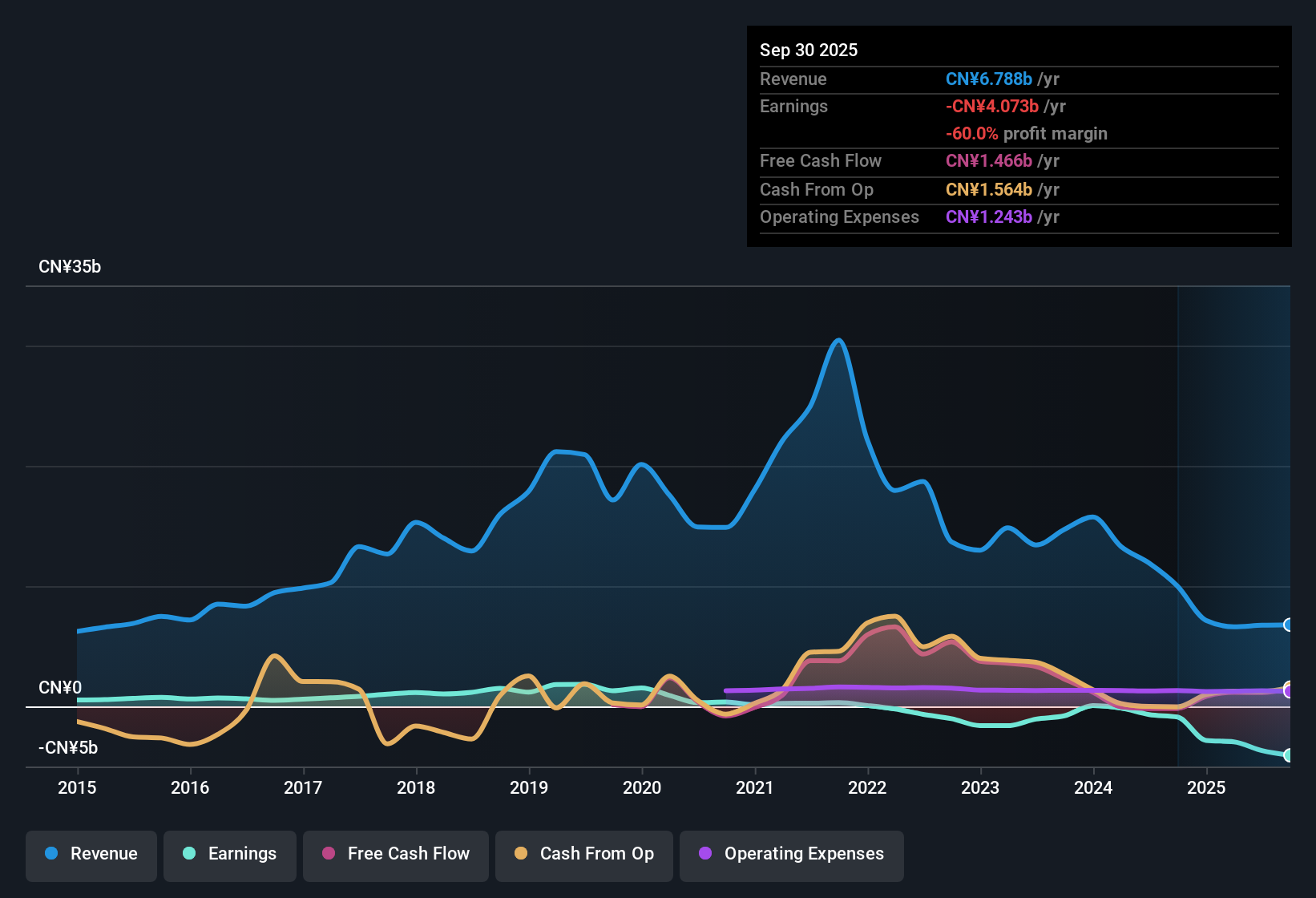

Beijing North Star (SEHK:588) remains unprofitable, with losses deepening at an annual rate of 61.5% over the past five years and no sign of margin recovery. The company's net profit margin has failed to improve, making any historical comparisons for earnings growth impossible at this stage. Despite the tough trends, Beijing North Star trades at a Price-to-Sales Ratio of 0.4x, which is well below peers at 8.5x and also under the Hong Kong real estate industry average of 0.7x. The current share price of HK$0.87 is significantly below an estimated fair value of HK$2.17. However, investors are facing major risks as both revenue and earnings growth remain off the table and financial health is in a poor position.

See our full analysis for Beijing North Star.Now let’s see how these numbers line up with the wider market narratives, and where the consensus may be due for a reality check.

Curious how numbers become stories that shape markets? Explore Community Narratives

Annual Losses Compound at 61.5%

- Beijing North Star’s losses have grown at a steep 61.5% compound annual rate over the past five years, far outpacing any sector recovery and leaving no track record of earnings growth to analyze in recent periods.

- What’s notable is that this deepening unprofitability directly undercuts the narrative that policy support or sector stabilization will soon translate into improved fundamentals for Beijing North Star.

- Despite hopes that state-linked developers might benefit from targeted intervention, the sustained, accelerating loss trend demonstrates the company is not yet positioned to capitalize if or when the broader market stabilizes.

- The lack of any recent margin improvement means that even optimistic sector-wide shifts may not rescue Beijing North Star’s bottom line without significant internal turnaround.

Profit Margins Remain Stuck at Lows

- The company’s net profit margin has shown no improvement, confirming that even as revenues stagnate, cost pressures or weak top-line performance continue to prevent a return to profitability.

- Critics highlight that the absence of margin recovery keeps Beijing North Star out of line with peer rebounds seen in parts of the Hong Kong real estate sector.

- While some competitors may leverage scale or diversified portfolios to cushion against downturns, North Star’s stuck margins suggest persistent structural challenges.

- This flat margin trend adds urgency to concerns about financial health, as ongoing losses erode flexibility for future investment or debt repayments.

Valuation Discount Deepens Amid Risks

- Trading at a Price-to-Sales Ratio of 0.4x, well below industry peers at 8.5x and the sector average of 0.7x, Beijing North Star’s valuation remains heavily discounted, with the share price (HK$0.87) significantly under its DCF fair value (HK$2.17).

- The prevailing view is that this low valuation only partly offsets risk, since both revenue and earnings are not expected to grow and balance sheet strain remains a core concern.

- Even bargain hunters need to weigh whether discounted pricing can outweigh ongoing operating losses and the lack of obvious turnaround catalysts.

- With financial health still described as poor, investors face the double challenge of no growth prospects and no clear improvement on the horizon.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on Beijing North Star's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

Beijing North Star’s deteriorating profitability, stagnant margins, and weak financial health expose investors to ongoing balance sheet strains with no clear recovery in sight.

If you want to focus on companies with strong finances designed to withstand tough markets, use our solid balance sheet and fundamentals stocks screener (1973 results) to filter for sturdier options right now.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English