Can Dorman (DORM) Balance Innovation and Profitability Amid Tariff Headwinds and Product Expansion?

- In October 2025, Dorman Products reported third quarter results with net sales rising to US$543.74 million and net income reaching US$76.42 million, both up from the prior year, and reaffirmed its full-year 2025 guidance for sales growth and earnings per share.

- A key highlight was the launch of an aftermarket-first electronic power steering rack for Ram trucks, reflecting the company’s continued product innovation focus within the automotive parts industry.

- We'll explore how Dorman's strong earnings amid tariff pressures and unique product launches could reshape its investment narrative.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

Dorman Products Investment Narrative Recap

To have conviction as a Dorman Products shareholder today, you need to believe in resilient aftermarket demand fueled by an aging vehicle fleet and the company’s consistent new product launches, even as tariff volatility threatens input costs and margin stability. The latest Q3 results, with strong sales and earnings growth, solidify Dorman’s reputation for operational execution, but the biggest short-term catalyst, margin expansion via automation and portfolio innovation, remains at risk from unpredictable tariff-related expenses. The recent earnings announcement confirms Dorman’s ability to pass through higher costs, but does not materially change the fact that tariff pressures still threaten to compress margins in coming quarters.

Among the most relevant recent announcements is the launch of Dorman’s aftermarket-first electronic power steering rack for Ram trucks. This strengthened the company’s innovation credentials and supports the core narrative that proprietary solutions can drive growth and profitability, particularly as the market for complex automotive electronics expands.

In contrast, investors should be aware that margin growth remains exposed to ongoing tariff uncertainty and...

Read the full narrative on Dorman Products (it's free!)

Dorman Products is projected to reach $2.5 billion in revenue and $237.0 million in earnings by 2028. This outlook requires a 6.0% annual revenue growth rate and an $11 million earnings increase from current earnings of $226.0 million.

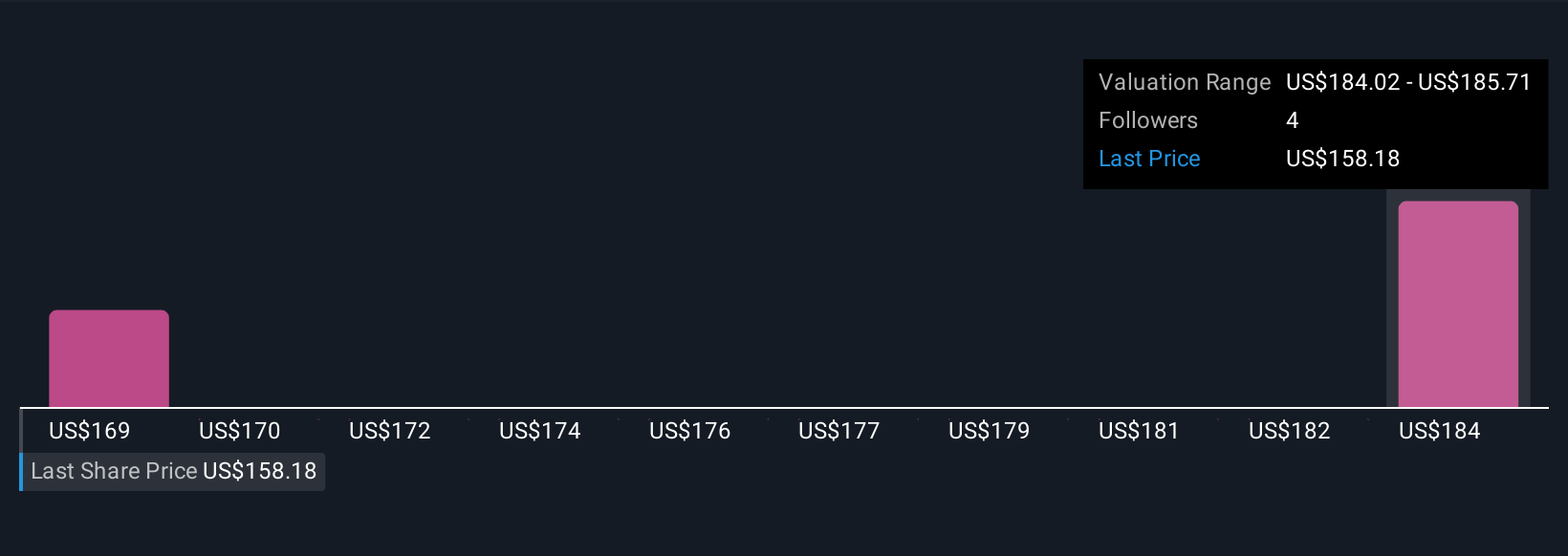

Uncover how Dorman Products' forecasts yield a $173.50 fair value, a 29% upside to its current price.

Exploring Other Perspectives

Simply Wall St Community members currently estimate Dorman’s fair value between US$173.50 and US$185.18 across 2 different views. While consensus sees resilient aftermarket demand as a positive driver, ongoing tariff costs highlight how outlooks for future margins may diverge.

Explore 2 other fair value estimates on Dorman Products - why the stock might be worth as much as 38% more than the current price!

Build Your Own Dorman Products Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Dorman Products research is our analysis highlighting 4 key rewards that could impact your investment decision.

- Our free Dorman Products research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Dorman Products' overall financial health at a glance.

Searching For A Fresh Perspective?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- These 16 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Find companies with promising cash flow potential yet trading below their fair value.

- Outshine the giants: these 26 early-stage AI stocks could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number : +852 3852 8500Service Email : service@webull.hkBusiness Cooperation : marketinghk@webull.hkWebull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English