Reassessing Want Want China Holdings (SEHK:151) Valuation After Mixed Half-Year Results and Profit Decline

Want Want China Holdings (SEHK:151) just posted mixed half year earnings, with sales edging higher but net income and earnings per share slipping, giving investors a tricky read on underlying profitability.

See our latest analysis for Want Want China Holdings.

The latest half year numbers land after a choppy stretch for the shares, with a 7 day share price return of 5.36 percent but a 90 day share price return of negative 11.69 percent. The 1 year total shareholder return of 14.60 percent suggests longer term holders are still ahead even as near term momentum looks tentative.

If this mixed picture has you reassessing your watchlist, it could be a good moment to explore fast growing stocks with high insider ownership as a way to uncover other potential compounders.

With sales ticking up, profits sliding, a sizeable intrinsic value discount and only a modest gap to analyst targets, investors now face the key question: is Want Want undervalued or already pricing in its future growth?

Price-to-Earnings of 12.6x: Is it justified?

On a price-to-earnings basis, Want Want China Holdings trades at 12.6x earnings, placing it slightly above peer averages despite the recent share price weakness.

The price-to-earnings ratio compares the current share price to earnings per share. It is a simple way to gauge how much investors are paying for each unit of profit in a relatively mature, cash generative consumer staples business.

For Want Want, the market is asking a small premium to the peer average of 12.4x. This still screens as reasonable value against the estimated fair price-to-earnings ratio of 13x, which suggests there may be room for the multiple to expand if earnings trends stabilise.

Compared with the broader Hong Kong Food industry, where the average price-to-earnings ratio sits at 13.1x, Want Want trades at a modest discount. This underlines that the stock is not being priced as an outright growth outlier, but rather as a slightly cheaper way to access the sector if its earnings can re accelerate.

Explore the SWS fair ratio for Want Want China Holdings

Result: Price-to-Earnings of 12.6x (ABOUT RIGHT)

However, persistent margin pressure, or a sharper slowdown in China’s packaged food demand, could quickly cap any valuation upside investors are hoping for.

Find out about the key risks to this Want Want China Holdings narrative.

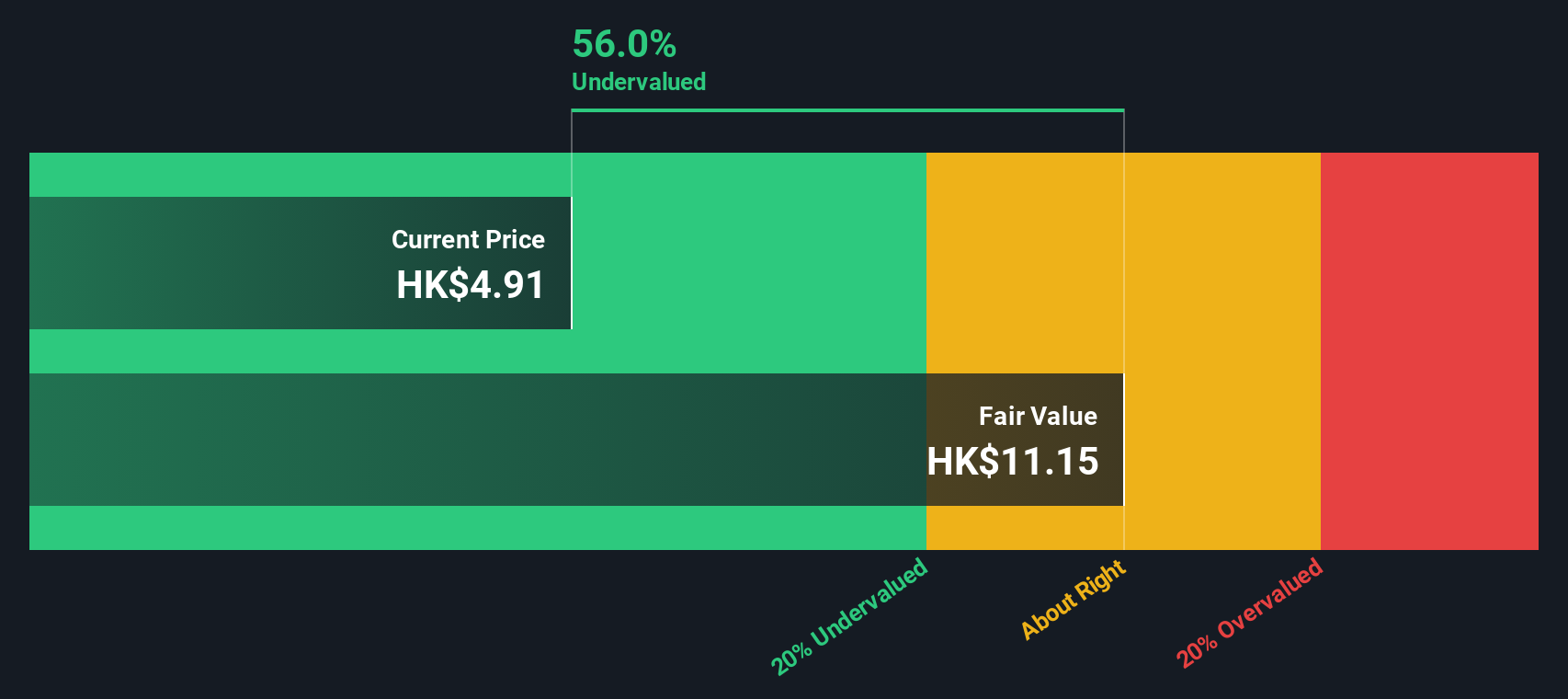

Another View: Our DCF Model Points Much Higher

While the 12.6x price to earnings ratio looks about right, our DCF model paints a very different picture. It suggests a fair value of around HK$11.15 per share compared with today’s HK$4.91, which indicates the market could be heavily discounting Want Want’s future cash flows.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Want Want China Holdings for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 906 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Want Want China Holdings Narrative

If you see the story differently or want to stress test the assumptions with your own research, you can build a custom narrative in minutes: Do it your way.

A great starting point for your Want Want China Holdings research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Ready for your next investing move?

Want Want might only be the starting point, and ignoring other high potential ideas could mean leaving serious upside on the table, so consider how to put your capital to work intelligently.

- Explore income focused opportunities by scanning these 15 dividend stocks with yields > 3% that may help strengthen your portfolio with cash returns.

- Focus your growth search by targeting these 26 AI penny stocks positioned to benefit from shifts in artificial intelligence adoption.

- Position yourself ahead of the crowd by reviewing these 81 cryptocurrency and blockchain stocks that are shaping developments in digital finance and blockchain infrastructure.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English