A Look At Soho House & Co (SHCO) Valuation After Mixed Short And Long Term Returns

Soho House & Co (SHCO) has recently drawn investor attention after a period of mixed share performance, with the stock showing a small positive 1 year total return alongside negative moves over the past week, month and past 3 months.

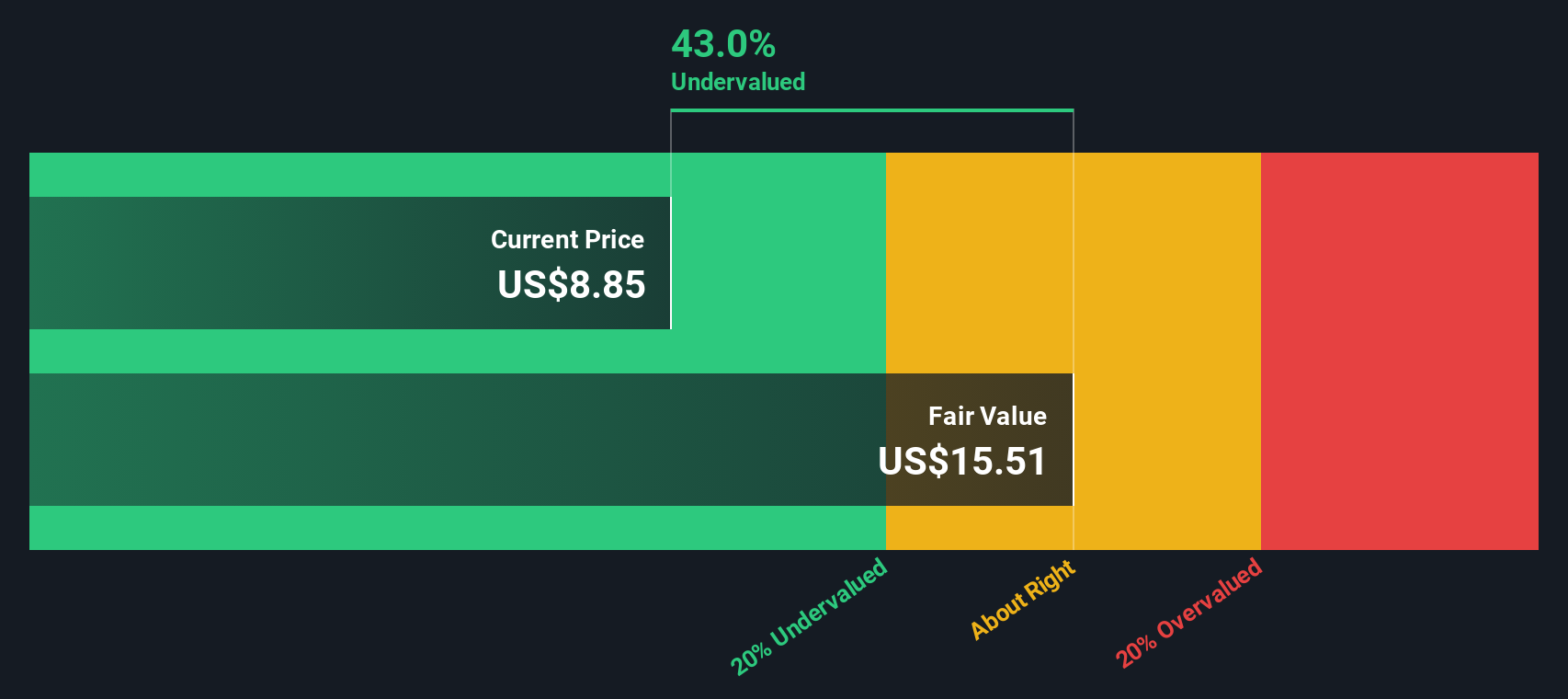

See our latest analysis for Soho House & Co.

The recent 1 day share price return of 2.59% decline, alongside weaker 7 day and 30 day share price returns, suggests fading short term momentum, even as the 3 year total shareholder return of 48.78% points to a stronger longer term journey for committed holders.

If Soho House & Co has you rethinking where growth could come from next, it might be worth widening your lens to fast growing stocks with high insider ownership.

So, with modest 1-year gains, a strong 3-year total return, and a recent loss-making position on roughly $1.29b of revenue, is Soho House & Co undervalued today, or is the market already pricing in future growth?

Most Popular Narrative: 12.2% Undervalued

With Soho House & Co last closing at US$7.90 against a narrative fair value of US$9.00, the current setup points to a valuation gap that depends on how its growth plans and margin ambitions develop over time.

The company is focusing on enhancing operational excellence, aiming for greater profit and cash flow. This includes simplifying business processes, transforming back-of-house systems for efficiencies, and improved service, which should positively impact net margins over time.

Curious what kind of revenue path and margin lift are embedded in that number, and how rich the future earnings multiple needs to be to support it? The narrative is based on faster top line expansion, a swing from losses toward profits, and a valuation multiple more commonly associated with market favorites. If you want to see exactly how those moving parts combine into that fair value, the full narrative lays out the assumptions in detail.

Result: Fair Value of $9.0 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, the potential takeover uncertainty and previously reported financial misstatements could unsettle confidence, and higher near term ERP and finance costs may weigh on margins.

Find out about the key risks to this Soho House & Co narrative.

Another Angle on Value

While the analyst narrative points to Soho House & Co trading about 12.2% below a US$9.00 fair value, our DCF model presents a different perspective. Based on that model, the shares at US$7.90 sit above an estimated fair value of US$7.04, which suggests less apparent upside and a greater need to stress test your own assumptions.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Soho House & Co for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 879 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Soho House & Co Narrative

If you look at the numbers and come to a different conclusion, or just prefer to test every input yourself, you can build a customised view in just a few minutes with Do it your way.

A great starting point for your Soho House & Co research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Ready for more investment ideas?

If Soho House & Co is only one piece of your watchlist, now is the time to widen your search and spot opportunities others might overlook.

- Target potential value by scanning these 879 undervalued stocks based on cash flows that appear attractively priced based on cash flows and may warrant a closer look.

- Spot future themed opportunities by checking out these 29 quantum computing stocks that are linked to emerging computing breakthroughs and specialised hardware.

- Strengthen your income watchlist by reviewing these 12 dividend stocks with yields > 3% that currently offer yields above 3% and might suit a dividend focused approach.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English