China Life Insurance Company Limited (HKG:2628) Surges 25% Yet Its Low P/E Is No Reason For Excitement

Despite an already strong run, China Life Insurance Company Limited (HKG:2628) shares have been powering on, with a gain of 25% in the last thirty days. The annual gain comes to 145% following the latest surge, making investors sit up and take notice.

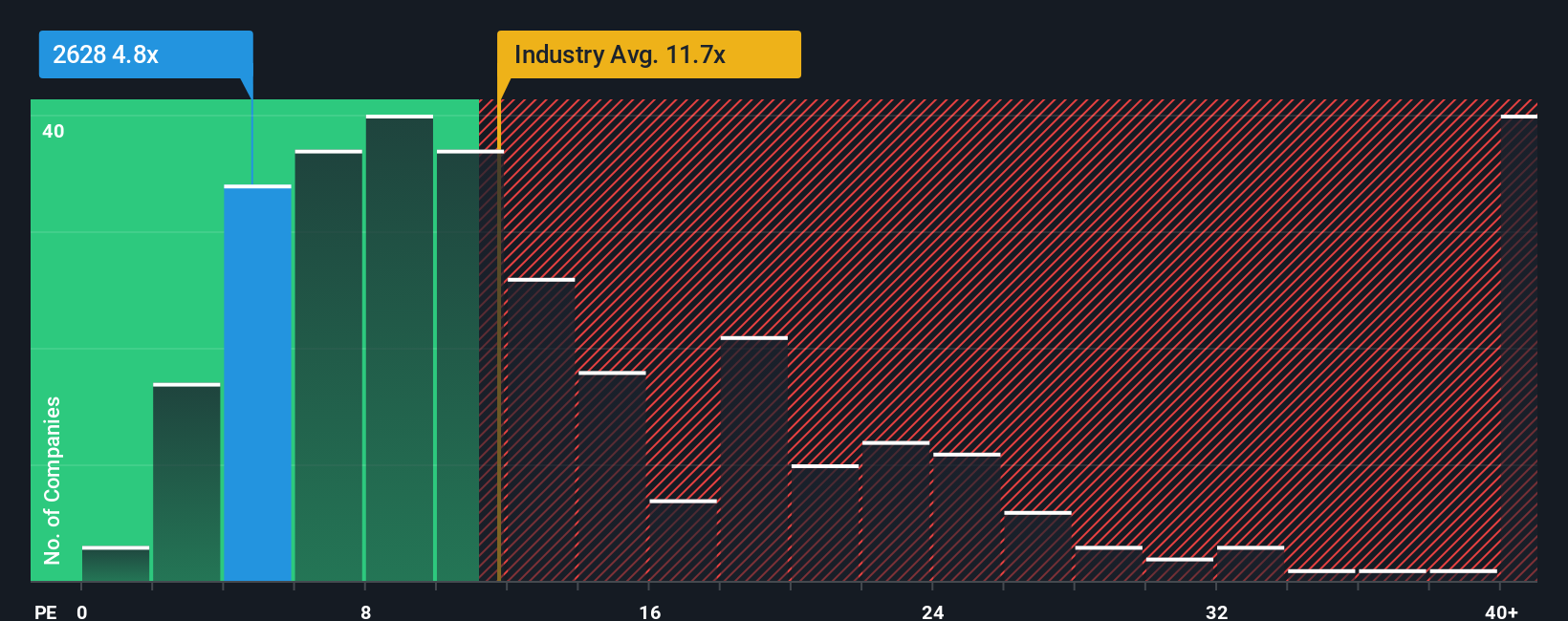

In spite of the firm bounce in price, China Life Insurance may still be sending very bullish signals at the moment with its price-to-earnings (or "P/E") ratio of 5.2x, since almost half of all companies in Hong Kong have P/E ratios greater than 13x and even P/E's higher than 26x are not unusual. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's so limited.

China Life Insurance certainly has been doing a good job lately as it's been growing earnings more than most other companies. It might be that many expect the strong earnings performance to degrade substantially, which has repressed the P/E. If not, then existing shareholders have reason to be quite optimistic about the future direction of the share price.

See our latest analysis for China Life Insurance

How Is China Life Insurance's Growth Trending?

In order to justify its P/E ratio, China Life Insurance would need to produce anemic growth that's substantially trailing the market.

Taking a look back first, we see that the company grew earnings per share by an impressive 45% last year. Pleasingly, EPS has also lifted 411% in aggregate from three years ago, thanks to the last 12 months of growth. Accordingly, shareholders would have probably welcomed those medium-term rates of earnings growth.

Shifting to the future, estimates from the twelve analysts covering the company suggest earnings growth is heading into negative territory, declining 28% per year over the next three years. Meanwhile, the broader market is forecast to expand by 14% per year, which paints a poor picture.

In light of this, it's understandable that China Life Insurance's P/E would sit below the majority of other companies. Nonetheless, there's no guarantee the P/E has reached a floor yet with earnings going in reverse. Even just maintaining these prices could be difficult to achieve as the weak outlook is weighing down the shares.

What We Can Learn From China Life Insurance's P/E?

Shares in China Life Insurance are going to need a lot more upward momentum to get the company's P/E out of its slump. It's argued the price-to-earnings ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

As we suspected, our examination of China Life Insurance's analyst forecasts revealed that its outlook for shrinking earnings is contributing to its low P/E. At this stage investors feel the potential for an improvement in earnings isn't great enough to justify a higher P/E ratio. Unless these conditions improve, they will continue to form a barrier for the share price around these levels.

You always need to take note of risks, for example - China Life Insurance has 1 warning sign we think you should be aware of.

You might be able to find a better investment than China Life Insurance. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English