Unveiling 3 Undiscovered Gems in Asia with Promising Potential

As global markets navigate a landscape marked by geopolitical uncertainties and fluctuating indices, Asia's economic resilience continues to capture investor interest. Amid this backdrop, identifying promising small-cap stocks in the region can be particularly rewarding for those seeking opportunities beyond the mainstream. In this article, we explore three lesser-known Asian companies that stand out due to their robust fundamentals and potential for growth in today's dynamic market environment.

Top 10 Undiscovered Gems With Strong Fundamentals In Asia

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Hongmian Zhihui Science and Technology InnovationLtd.Guangzhou | 17.36% | -10.02% | 57.60% | ★★★★★★ |

| Saison Technology | NA | 1.32% | -10.74% | ★★★★★★ |

| Saha-Union | 0.70% | 0.67% | 18.29% | ★★★★★★ |

| Nanfang Ventilator | NA | -10.23% | 25.64% | ★★★★★★ |

| Woojin | 1.02% | 8.91% | -11.74% | ★★★★★★ |

| Myung In Pharmaceutical | NA | 8.27% | 8.53% | ★★★★★★ |

| Shenzhen Zhongheng Huafa | NA | 2.72% | 37.80% | ★★★★★★ |

| Chin Hsin Environ Engineering | 5.28% | 24.51% | 40.62% | ★★★★★☆ |

| MNtech | 69.81% | 10.24% | -13.03% | ★★★★★☆ |

| ILSEUNG | 35.04% | 0.33% | 32.17% | ★★★★★☆ |

We're going to check out a few of the best picks from our screener tool.

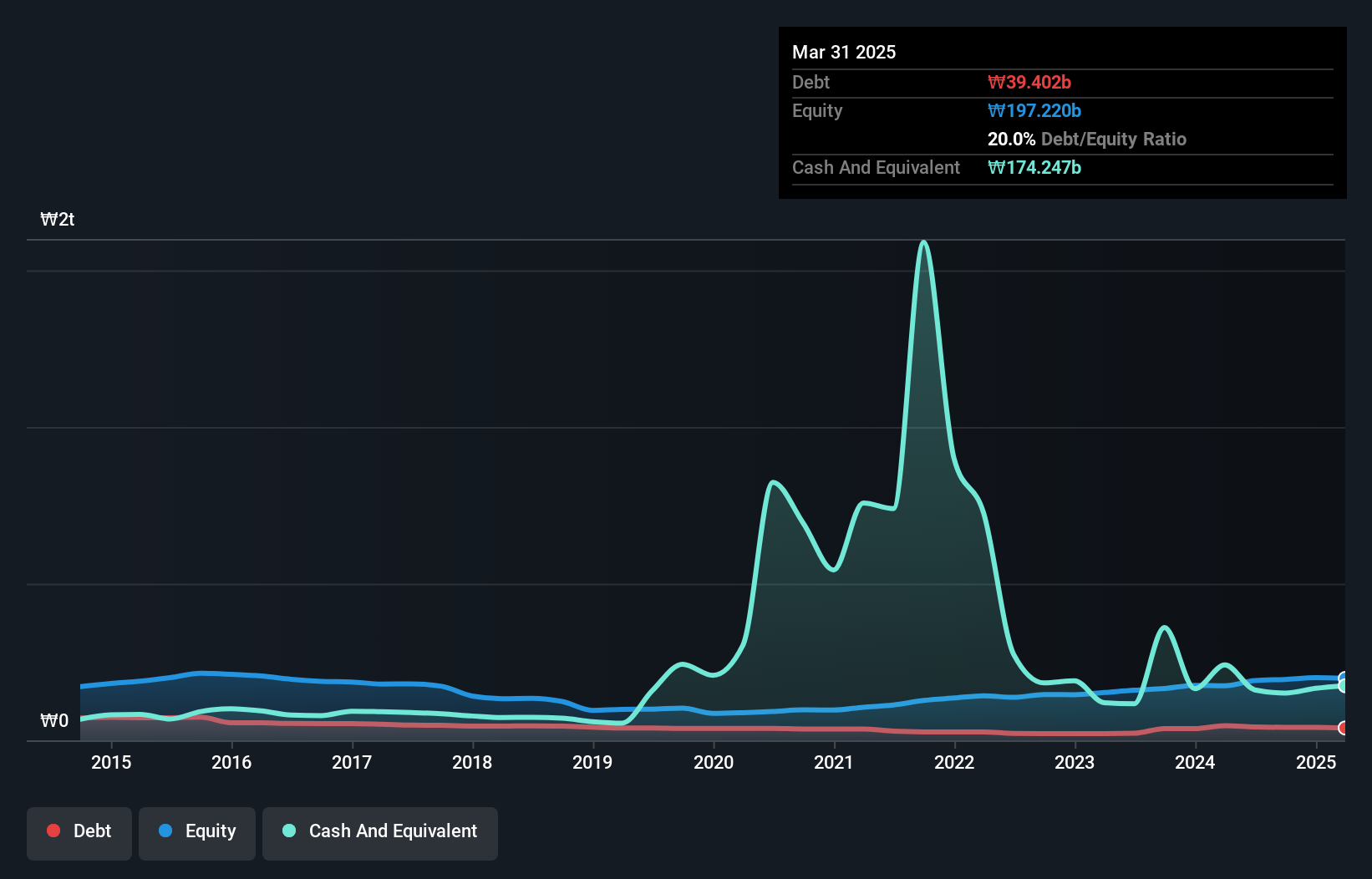

Kona ILtd (KOSDAQ:A052400)

Simply Wall St Value Rating: ★★★★★★

Overview: Kona I Co., Ltd. offers solutions and platforms for the financial technology market both in South Korea and internationally, with a market cap of ₩907.73 billion.

Operations: Kona I Co., Ltd. generates revenue through its financial technology solutions and platforms, catering to both domestic and international markets. The company's market cap is ₩907.73 billion, reflecting its scale in the industry.

Kona I Ltd., a small player in the tech sector, has shown impressive earnings growth of 125.2% over the past year, significantly outpacing the industry's 9.6%. Despite its volatile share price recently, it trades at nearly half its estimated fair value. The company's net income surged to ₩30.07 billion for Q3 2025 from ₩7.45 billion a year earlier, boosted by a one-off gain of ₩14 billion. Kona I's debt-to-equity ratio improved from 37.1% to 16.4% over five years, and with interest payments well covered by EBIT (355x), it appears financially robust despite recent challenges in sales figures.

- Navigate through the intricacies of Kona ILtd with our comprehensive health report here.

Evaluate Kona ILtd's historical performance by accessing our past performance report.

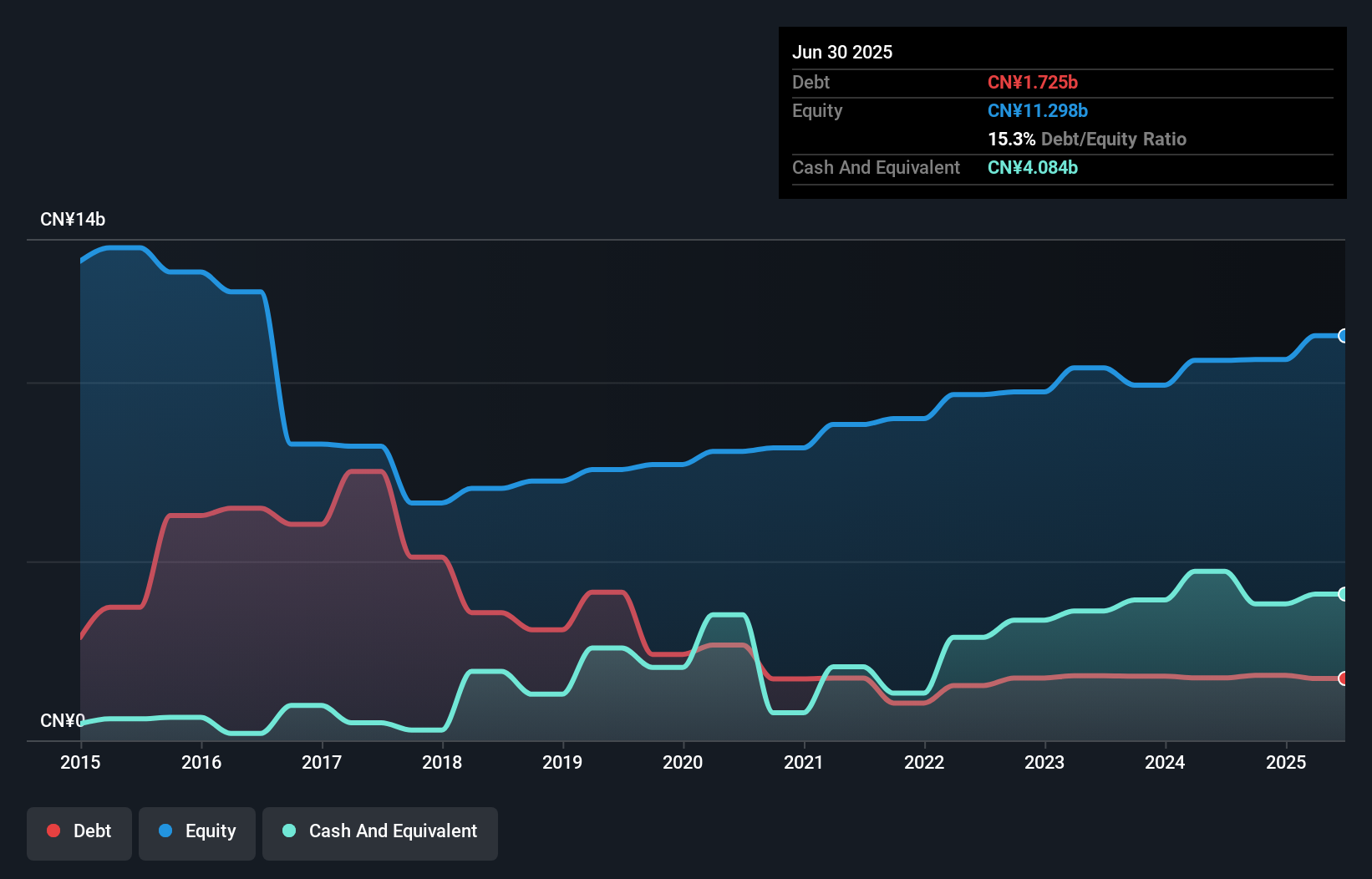

Sinofert Holdings (SEHK:297)

Simply Wall St Value Rating: ★★★★★☆

Overview: Sinofert Holdings Limited is an investment holding company involved in the production, import and export, distribution, and retail of fertilizer raw materials and crop nutrition products both in Mainland China and internationally, with a market capitalization of approximately HK$12.92 billion.

Operations: Sinofert Holdings generates revenue primarily from its Basic Business, contributing CN¥16.37 billion, and Growth Business, which adds CN¥11.18 billion. The Production segment accounts for CN¥5.54 billion in revenue.

Sinofert Holdings, a notable player in the Asian market, has shown promising growth with earnings surging 65.7% over the past year, outpacing the Chemicals industry at 19.2%. Its debt-to-equity ratio improved significantly from 33% to 15.3% over five years, indicating better financial health. The company appears undervalued by trading at 30.1% below its estimated fair value and holds more cash than total debt, suggesting a strong balance sheet position. Recent executive changes include Ms. Lai Ying Tung's appointment as Company Secretary following Ms. Cheung Kar Mun's resignation, reflecting ongoing corporate governance enhancements within Sinofert Holdings' structure.

- Click to explore a detailed breakdown of our findings in Sinofert Holdings' health report.

Understand Sinofert Holdings' track record by examining our Past report.

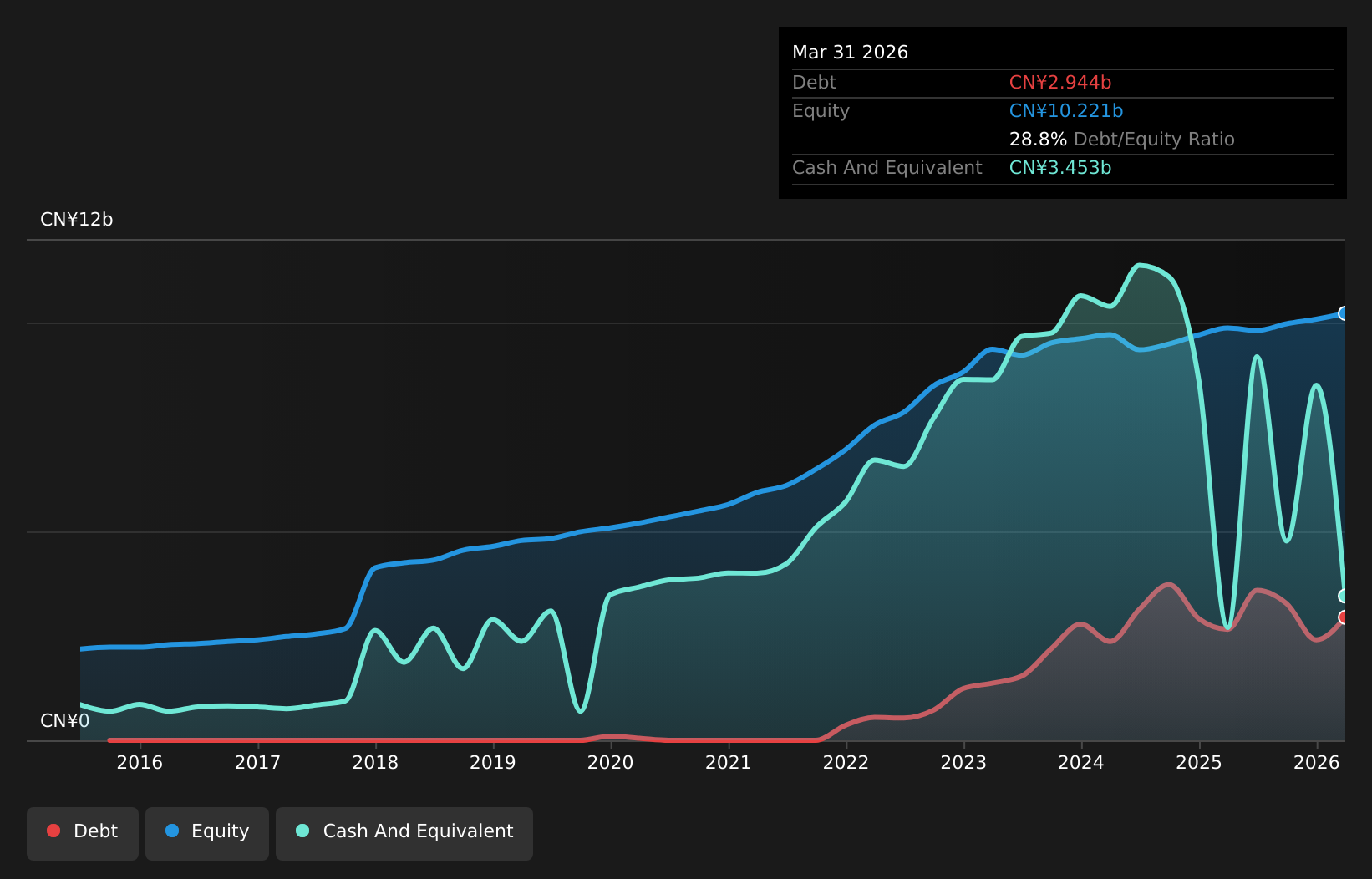

Anhui Guangxin Agrochemical (SHSE:603599)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Anhui Guangxin Agrochemical Co., Ltd. engages in the research, development, production, and sale of pesticide technicals, preparations, and intermediates in China with a market capitalization of CN¥12.83 billion.

Operations: Anhui Guangxin Agrochemical generates revenue primarily from the sale of pesticide technicals, preparations, and intermediates. The company's financial performance is reflected in its market capitalization of CN¥12.83 billion.

Anhui Guangxin Agrochemical, a smaller player in the agrochemical sector, presents an intriguing investment case with its solid financial footing. The company boasts a price-to-earnings ratio of 17.7x, notably below the China market average of 49.3x, suggesting it trades at an attractive value compared to peers. Despite a rise in its debt-to-equity ratio to 32.8% over five years, Anhui maintains more cash than total debt, ensuring financial stability and interest coverage is well-managed as profits exceed interest obligations. Although recent earnings growth of 5.1% lagged behind the industry average of 6.2%, future prospects appear promising with forecasts predicting annual growth of 17%.

Taking Advantage

- Click this link to deep-dive into the 2498 companies within our Asian Undiscovered Gems With Strong Fundamentals screener.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English