The Returns On Capital At Kong Sun Holdings (HKG:295) Don't Inspire Confidence

If we're looking to avoid a business that is in decline, what are the trends that can warn us ahead of time? A business that's potentially in decline often shows two trends, a return on capital employed (ROCE) that's declining, and a base of capital employed that's also declining. This combination can tell you that not only is the company investing less, it's earning less on what it does invest. Having said that, after a brief look, Kong Sun Holdings (HKG:295) we aren't filled with optimism, but let's investigate further.

What Is Return On Capital Employed (ROCE)?

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. Analysts use this formula to calculate it for Kong Sun Holdings:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

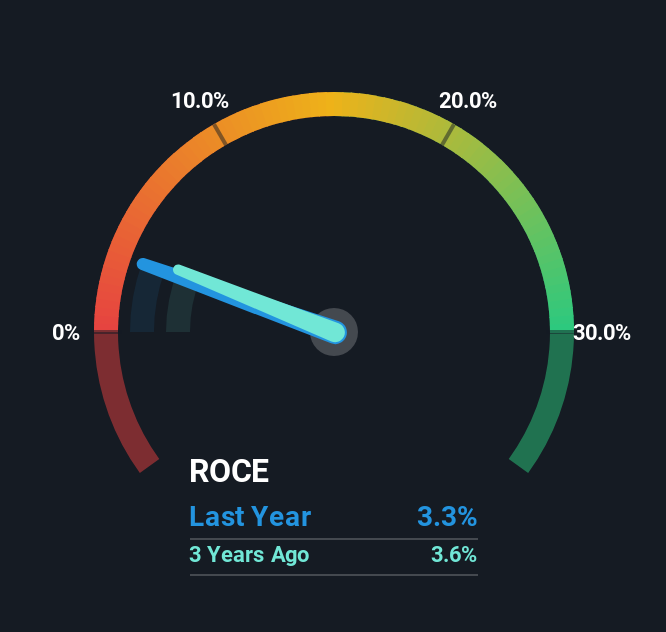

0.033 = CN¥104m ÷ (CN¥4.6b - CN¥1.4b) (Based on the trailing twelve months to June 2025).

Therefore, Kong Sun Holdings has an ROCE of 3.3%. Ultimately, that's a low return and it under-performs the Renewable Energy industry average of 6.8%.

View our latest analysis for Kong Sun Holdings

Historical performance is a great place to start when researching a stock so above you can see the gauge for Kong Sun Holdings' ROCE against it's prior returns. If you're interested in investigating Kong Sun Holdings' past further, check out this free graph covering Kong Sun Holdings' past earnings, revenue and cash flow.

What Can We Tell From Kong Sun Holdings' ROCE Trend?

The trend of returns that Kong Sun Holdings is generating are raising some concerns. Unfortunately, returns have declined substantially over the last five years to the 3.3% we see today. What's equally concerning is that the amount of capital deployed in the business has shrunk by 77% over that same period. The fact that both are shrinking is an indication that the business is going through some tough times. Typically businesses that exhibit these characteristics aren't the ones that tend to multiply over the long term, because statistically speaking, they've already gone through the growth phase of their life cycle.

While on the subject, we noticed that the ratio of current liabilities to total assets has risen to 31%, which has impacted the ROCE. If current liabilities hadn't increased as much as they did, the ROCE could actually be even lower. While the ratio isn't currently too high, it's worth keeping an eye on this because if it gets particularly high, the business could then face some new elements of risk.

What We Can Learn From Kong Sun Holdings' ROCE

In short, lower returns and decreasing amounts capital employed in the business doesn't fill us with confidence. We expect this has contributed to the stock plummeting 84% during the last five years. Unless there is a shift to a more positive trajectory in these metrics, we would look elsewhere.

On a separate note, we've found 1 warning sign for Kong Sun Holdings you'll probably want to know about.

For those who like to invest in solid companies, check out this free list of companies with solid balance sheets and high returns on equity.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English