A Look At Semiconductor Manufacturing International (SEHK:981) Valuation After Strong Multi Year Returns

Recent performance snapshot

Semiconductor Manufacturing International (SEHK:981) has drawn attention after a period of mixed share performance, with declines over the past week and month contrasting with a positive total return over the past year.

See our latest analysis for Semiconductor Manufacturing International.

The recent 1 day share price return of 1.89% and 7 day share price return of 12.69% both sit against a year to date share price return of 10.19% and a 1 year total shareholder return of 40.81%. This suggests shorter term momentum is currently fading after a strong run supported by multi year total shareholder returns that are more than 2x over 3 years and well above 1x over 5 years.

If Semiconductor Manufacturing International’s recent swings have you reassessing chip exposure, it could be a good moment to see what else is moving across 1 AI infrastructure stocks and compare different ways to get AI hardware exposure.

With Semiconductor Manufacturing International still showing a 40.81% 1 year total return but weaker recent price moves, the real question is whether current levels offer value or if the market is already pricing in future growth?

Most Popular Narrative: 10% Undervalued

With Semiconductor Manufacturing International last closing at HK$67.45 against a widely followed fair value estimate of HK$74.69, the current pricing sits slightly below that narrative view and puts the underlying assumptions in focus.

SMIC's aggressive expansion of wafer capacity, particularly in 8-inch and 12-inch nodes, positions the company to capture rising demand from domestic downstream markets such as automotive and analog, supported by strong volume growth and high utilization rates, this supports long-term revenue growth and stabilization of gross margins.

Curious what sits behind that fair value gap? The narrative leans on steady top line momentum, firmer margins, and a future profit multiple that assumes solid earnings traction. The real interest is how those ingredients are combined to justify today’s target.

Result: Fair Value of HK$74.69 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, the thesis could unravel if pricing pressure continues to drag on gross margins, or if heavy capital spending results in overcapacity and weaker returns.

Find out about the key risks to this Semiconductor Manufacturing International narrative.

Another way to look at value

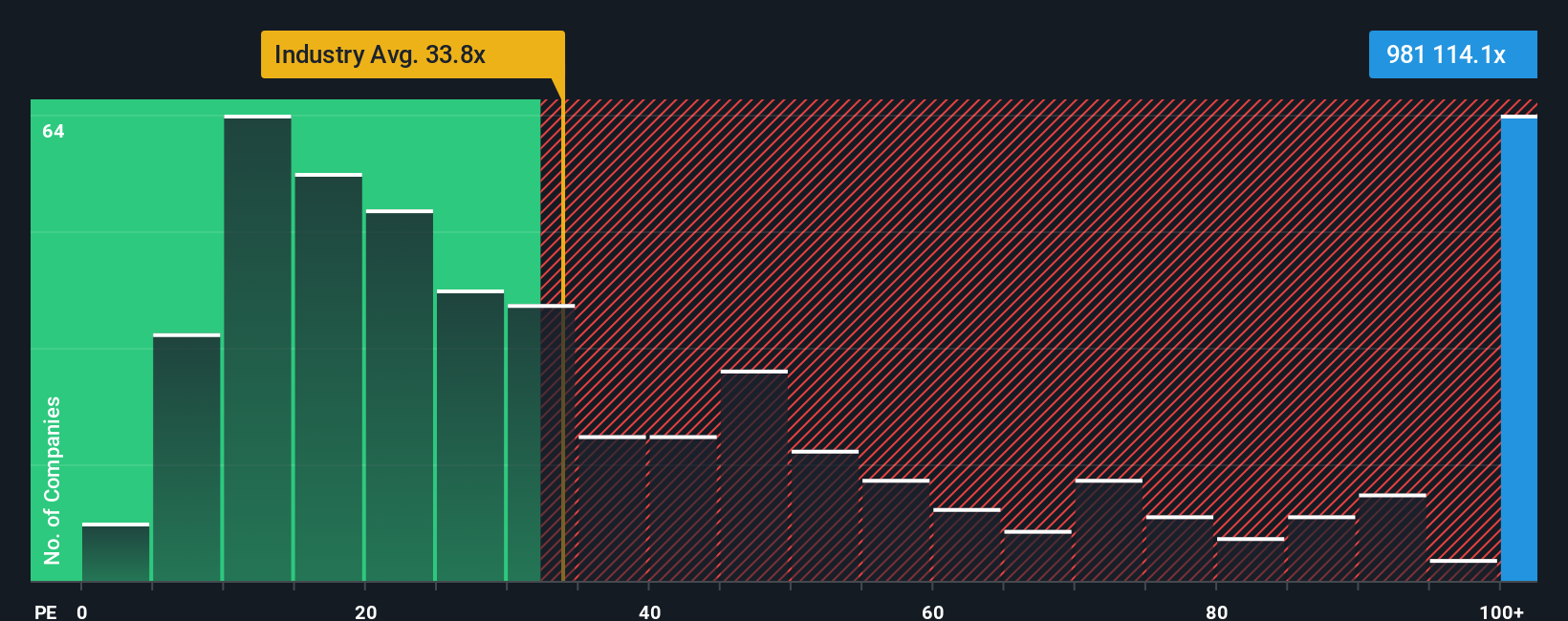

While the narrative implies Semiconductor Manufacturing International is around 10% undervalued at HK$74.69, the current P/E of 111.4x tells a different story. It sits well above the fair ratio of 44.4x and the Asian semiconductor average of 42.7x, and also far above the 29.5x peer average. That kind of gap can mean high expectations are already baked in, so the key question is whether you think earnings can grow fast enough to justify staying this far ahead of the pack.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Semiconductor Manufacturing International Narrative

If you are not fully on board with this view, or simply prefer to weigh the data yourself, you can piece together your own Semiconductor Manufacturing International story in just a few minutes, starting with Do it your way.

A great starting point for your Semiconductor Manufacturing International research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If SMIC has sharpened your interest in chip exposure, do not stop here. A broader watchlist can help you stay ready when the next setup appears.

- Pinpoint value focused opportunities by scanning our 234 high quality undervalued stocks that combine quality fundamentals with prices that may sit below fair estimates.

- Reduce portfolio stress by checking 332 resilient stocks with low risk scores that score well on stability and lower risk profiles.

- Get ahead of the crowd by reviewing our screener containing 140 high quality undiscovered gems that highlight quality businesses which are not yet widely followed.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English