A Look At CyberArk Software (CYBR) Valuation As Earnings Highlight Revenue Growth And A Smaller Net Loss

Earnings report puts CyberArk Software (CYBR) in focus

CyberArk Software (NasdaqGS:CYBR) is back on investors’ radar after its latest earnings release, which paired higher fourth quarter and full year 2025 revenue with a much smaller quarterly net loss.

See our latest analysis for CyberArk Software.

The earnings release and upcoming WEST Conference appearance have arrived after a weaker patch for the stock. The 30 day share price return is 10.40% and the 90 day share price return is 20.85%, set against a 3 year total shareholder return of about 1.8x. This hints that long term enthusiasm has cooled recently but not disappeared.

If this earnings driven move has you looking beyond a single name, it could be a good moment to see what else is happening across 57 profitable AI stocks that aren't just burning cash and compare how other AI focused software players are being priced.

With CyberArk shares giving back some ground over the past month despite higher revenue and a narrower quarterly loss, the key question now is whether this pullback leaves the stock undervalued or if the market is already pricing in future growth.

Most Popular Narrative: 13.8% Undervalued

CyberArk’s most followed narrative puts fair value at about $474.79 versus the last close at $409.22, framing the recent pullback as a potential valuation gap rather than a verdict on the business.

The evolving machine identity market, coupled with CyberArk’s focus on AI-driven identity security through its machine identity capabilities and Secrets Management, is expected to drive significant revenue growth as organizations seek integrated solutions to manage increasingly complex identity security needs. CyberArk's unified identity security platform, which includes privileged access management and workforce security, is expected to drive higher average deal sizes, revenue growth, and improved net margins as customers increasingly consolidate their identity security solutions with trusted vendors.

Want to see what sits behind that valuation gap? The narrative leans on faster revenue compounding, a swing to profits, and a premium earnings multiple that assumes CyberArk keeps winning bigger identity security budgets.

Result: Fair Value of $474.79 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, you also need to weigh two key watchpoints: the execution risk around integrating Venafi and Zilla Security, and the pressure from intensifying identity security competition.

Find out about the key risks to this CyberArk Software narrative.

Another way to look at CyberArk’s valuation

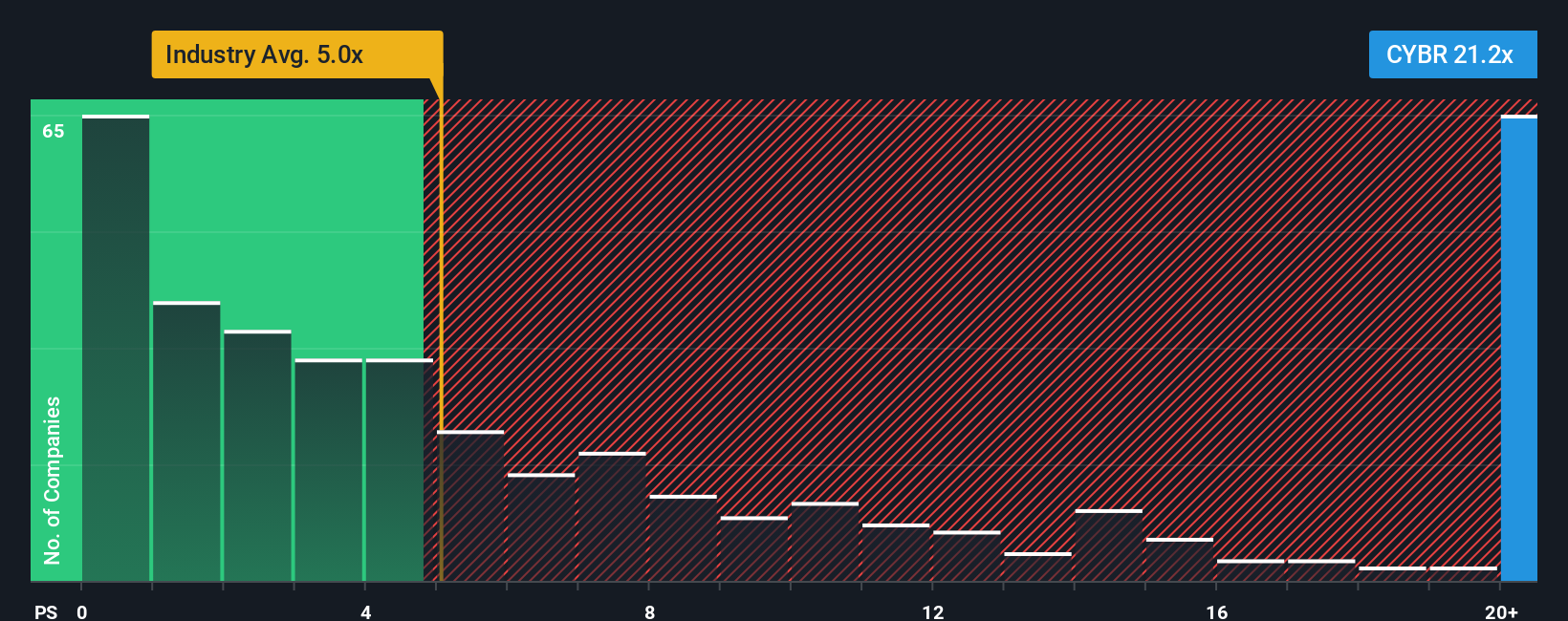

That $474.79 fair value relies on future earnings. If you switch to the current P/S ratio, CyberArk trades on 15.2x sales, which is far above the US Software average of 3.8x, the peer average of 7.3x, and a fair ratio of 7.8x. That kind of gap can mean rich expectations and a smaller margin for error. Which story do you trust more right now?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own CyberArk Software Narrative

If you look at this and think the story should read differently, that is your cue to test the numbers yourself and shape a version you trust, then Do it your way.

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding CyberArk Software.

Looking for more investment ideas?

If CyberArk has sharpened your appetite for deeper opportunities, now is the time to broaden your watchlist and pressure test your thinking across different types of stocks.

- Zero in on potential mispricings by scanning our 52 high quality undervalued stocks to find companies that pair quality fundamentals with prices that may sit below intrinsic value estimates.

- Prioritize resilience and sleep better at night by checking companies in our 82 resilient stocks with low risk scores that score well on financial strength and business stability.

- Stay a step ahead of the crowd by studying our screener containing 24 high quality undiscovered gems where strong fundamentals have not yet attracted broad market attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English