A Look At SITC International Holdings (SEHK:1308) Valuation After New Nippon Express Container Branding Partnership

Nippon Express (China) Co., Ltd. has begun using NX Branded Containers on SITC International Holdings (SEHK:1308) vessels on the Shanghai to Osaka route, highlighting SITC’s role in intra Asian container shipping services.

See our latest analysis for SITC International Holdings.

The Nippon Express container branding agreement comes at a time when SITC International Holdings’ share price is HK$31.2 and recent momentum is positive, with a 7 day share price return of 5.12% and a 30 day share price return of 12.72%, backing up a 1 year total shareholder return of 99.78%.

If this partnership has you looking for more transport linked opportunities, it could be worth scanning our list of 24 power grid technology and infrastructure stocks as another way to find potential supply chain winners.

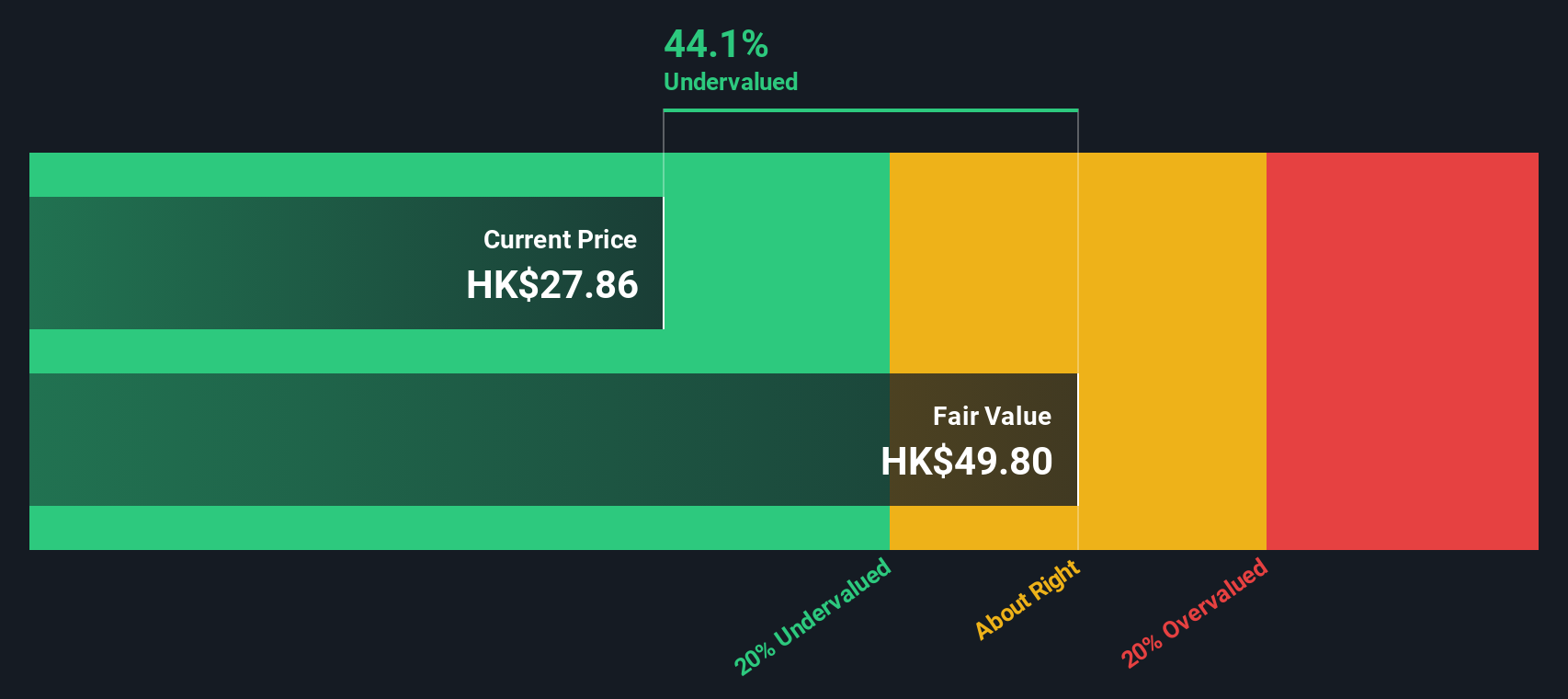

With SITC shares up almost 100% over the past year and trading slightly above the HK$29.82 analyst target, combined with an indicated 39% intrinsic discount, investors may ask whether there is still value available or whether the market is already pricing in future growth.

Price to Earnings of 8.2x: Is it justified?

On a P/E of 8.2x, SITC International Holdings screens cheaper than many peers, even though its HK$31.2 share price sits above the HK$29.82 analyst target.

The P/E multiple compares the current share price with the company’s earnings per share, so it effectively shows how much investors are paying for each dollar of current profit. For a shipping and logistics group like SITC, where earnings can fluctuate with trade flows and freight rates, the P/E often reflects how confident the market is that current profitability can be maintained.

Here, the picture is mixed. On one hand, SITC is described as good value relative to the Asian Shipping industry average P/E of 10.6x and the peer average of 8.9x. This points to a cheaper entry price for its earnings compared with competitors. On the other hand, it is labelled expensive when stacked against an estimated fair P/E of 7.7x. This is a level the market could move towards if sentiment cools or earnings expectations shift.

Result: Price-to-Earnings of 8.2x (ABOUT RIGHT)

Explore the SWS fair ratio for SITC International Holdings

However, you also have to weigh the declines in annual revenue and net income, as well as the fact that the current HK$31.2 price sits above analyst targets.

Find out about the key risks to this SITC International Holdings narrative.

Another View: Cash Flows Tell a Different Story

While the 8.2x P/E suggests SITC International Holdings is roughly in line with where the market might expect it to be, our DCF model points in a very different direction. It indicates the shares are trading around 39% below an intrinsic value of HK$50.74 per share.

That kind of gap can look like either a cushion for pessimistic earnings forecasts or a sign that the cash flow assumptions are too generous. Which side of the argument do you find more convincing?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out SITC International Holdings for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 227 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own SITC International Holdings Narrative

If you see the data differently or prefer to run your own checks, you can pull the key numbers together and Do it your way in under 3 minutes.

A great starting point for your SITC International Holdings research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

Ready to uncover more opportunities?

If you stop your research with a single stock, you risk missing better fits for your goals. Let the Simply Wall St Screener surface ideas you might not spot on your own.

- Target higher quality value ideas by scanning our list of 227 high quality undervalued stocks that combine attractive pricing with solid underlying businesses.

- Strengthen your income stream by checking out 430 dividend fortresses that focus on yields of 5% or more.

- Prioritise resilience by reviewing 330 resilient stocks with low risk scores selected for their lower risk scores and steadier profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English