Bio Rad Laboratories Q3 Loss Of US$12.70 EPS Tests Recovery Narrative For BIO Stock

Bio-Rad Laboratories (BIO) has put up a mixed set of numbers for Q3 FY 2025, with revenue of US$653 million and a basic EPS loss of US$12.70, against a backdrop of prior quarters that ranged from EPS of US$23.37 on US$649.7 million of revenue in Q3 FY 2024 to a loss of US$25.57 on US$667.48 million of revenue in Q4 FY 2024. Over the past few quarters, revenue has generally sat in the US$585 million to US$667 million band, while EPS has swung sharply between gains and losses. Investors will therefore be reading this latest print mainly through the lens of how margins are holding up and whether the path back to steadier profitability is coming into view.

See our full analysis for Bio-Rad Laboratories.With the headline figures on the table, the next step is to see how they line up against the big picture stories around Bio-Rad, highlighting where the latest numbers support those narratives and where they start to push back.

See what the community is saying about Bio-Rad Laboratories

Trailing 12 month loss of US$675.9 million

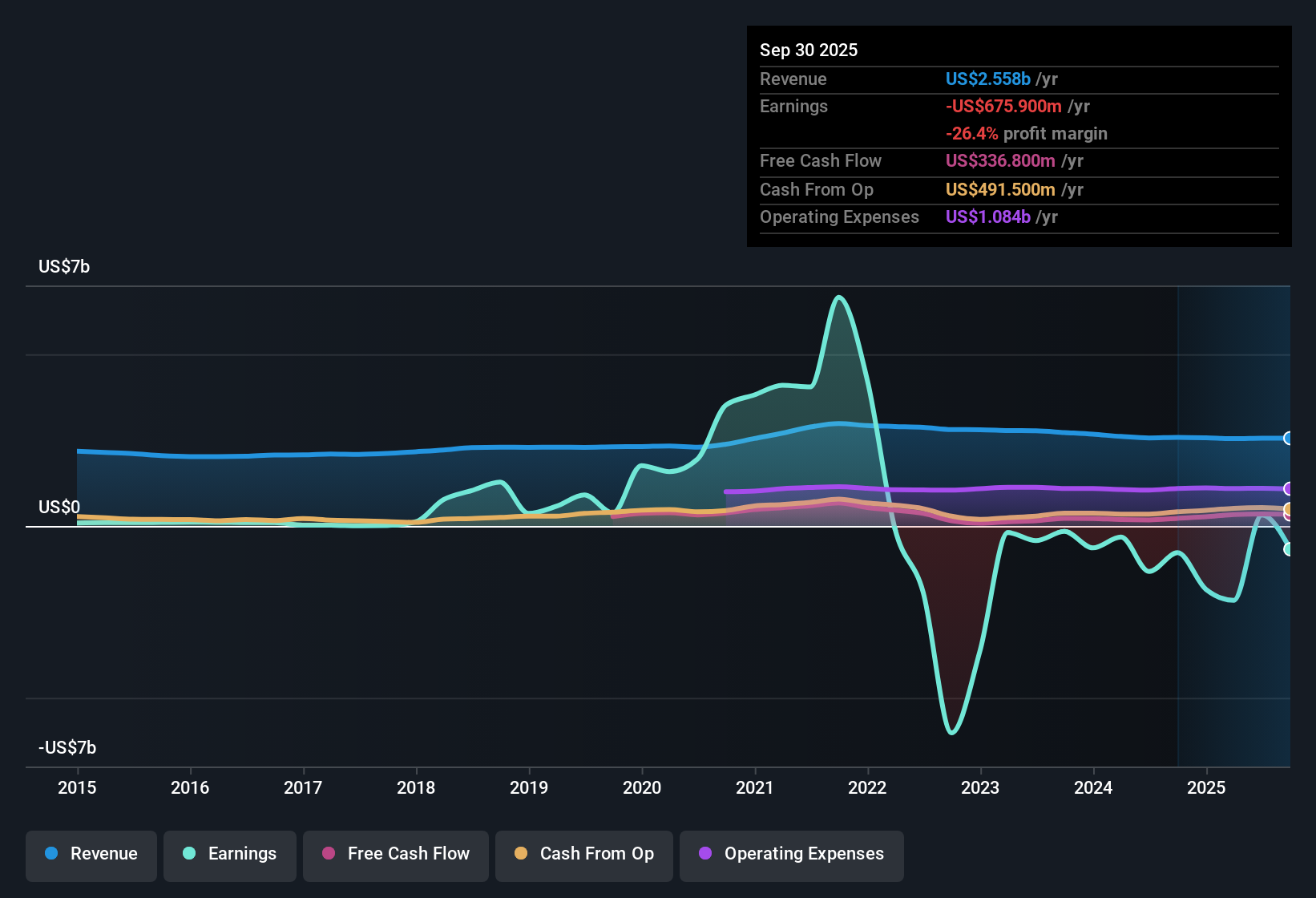

- On a trailing 12 month basis, Bio Rad reported a net loss of US$675.9 million on about US$2.6b of revenue, with basic EPS at a loss of US$24.56.

- Consensus narrative points to expansion in advanced diagnostics and stronger consumables as long term supports. However, the large trailing loss and swing from quarterly profit of US$317.8 million in Q2 FY 2025 to a loss of US$341.9 million in Q3 FY 2025 shows that any case for a smoother earnings profile still has to contend with very uneven recent profitability.

- The consensus view highlights higher margin recurring consumables as a stabiliser. At the same time, the last six reported quarters include several large losses, so investors may question how quickly that stabilising effect shows up in EPS.

- Forecast earnings growth of 5.46% per year and an expected return to profitability within three years sit against a 5 year history where losses have increased at about 51.5% annually. This keeps execution risk front and centre for this narrative.

Revenue steady around US$2.6b while growth forecast at 1.9%

- Revenue over the last 12 months has been fairly stable, sitting between US$2.5b and US$2.6b, and is projected in the data to grow at about 1.9% per year, below the referenced 10.3% for the broader US market.

- Bulls argue that digital PCR platforms and process chromatography can drive stronger top line momentum. However, the recent quarterly range of US$585.4 million to US$667.5 million and the modest 1.9% revenue growth forecast suggest the current run rate has not yet reflected the higher growth path that the bullish story leans on.

- Bullish expectations around accelerated adoption of ddPCR and biopharma demand imply a lift from the current roughly US$2.6b revenue base, while the forecast growth rate in the data remains low compared with the wider market.

- That gap means supporters of the bullish view may focus closely on future quarters for signs that revenue can move meaningfully above the recent US$585 million to US$667 million quarterly band.

Unprofitable today, but pricing in recovery

- At a current share price of US$256.56, Bio Rad sits below the DCF fair value of about US$286.41 and below the single allowed analyst price target of US$328.00, while the company remains unprofitable over the last 12 months.

- Bears point to rising losses over five years, at around 51.5% per year, and only 1.9% forecast revenue growth as reasons to question how much recovery is already reflected in valuation, even though the P/S multiple of 2.7x is below peers at 4.4x and roughly in line with the US Life Sciences industry at 2.8x.

- The lower P/S can be read as the market already baking in weaker growth and profitability than peers, which aligns with the cautious view. The discount to the DCF fair value and to the US$328.00 target suggests some investors still see room for upside if forecasts play out.

- For the bearish narrative to hold, the combination of continued losses and below market revenue growth would need to outweigh that apparent valuation gap on sales, keeping pressure on the share price despite the current discount to those reference values.

Next Steps

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Bio-Rad Laboratories on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

See the numbers differently? If this data is pointing you in another direction, shape that view into your own narrative in just a few minutes: Do it your way

A good starting point is our analysis highlighting 4 key rewards investors are optimistic about regarding Bio-Rad Laboratories.

See What Else Is Out There

Bio-Rad is wrestling with large recent losses, modest 1.9% revenue growth and uneven profitability, even as some investors frame the shares as a potential recovery story.

If that mix of rising losses and uncertain earnings makes you cautious, it could be a good moment to compare with 86 resilient stocks with low risk scores that score better on consistency and downside protection.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English