Shanghai MicroPort MedBot (SEHK:2252) Valuation After Global Toumai Robot Orders And Remote Surgery Progress

Shanghai MicroPort MedBot (Group) (SEHK:2252) is back on investors’ radar after reporting more than 200 commercial orders for its Toumai laparoscopic surgical robot, with around 130 systems installed across nearly 50 countries and regions.

See our latest analysis for Shanghai MicroPort MedBot (Group).

The recent Toumai order momentum and remote surgery progress come as the shares trade at HK$29.0, with an 11.71% 1 day share price return and 22.99% 90 day share price return, alongside a 50.57% 1 year total shareholder return that contrasts with a 3 year total shareholder return decline of 8.52%. This suggests sentiment has improved in the shorter term.

If this story around surgical robotics has caught your attention, it could be a good moment to see what else is emerging in the space through our 30 robotics and automation stocks.

So with the shares at HK$29.0, recent returns firmly in the green and Toumai gaining global traction, is Shanghai MicroPort MedBot still trading at a discount or are markets already pricing in its future growth potential?

Price to Book of 49.4x: Is it justified?

Right now, Shanghai MicroPort MedBot is trading on a P/B ratio of 49.4x, compared with a peer average of 7.4x and a Hong Kong Medical Equipment industry average of 1.8x, which points to a rich valuation on this metric.

The P/B ratio compares the company’s market value with its book value. A higher figure often reflects strong expectations for future returns on the asset base. For a business that is still loss making, such as Shanghai MicroPort MedBot with a reported loss of CN¥478.596m on revenue of CN¥333.701m, a very high P/B usually signals that investors are focusing on future potential rather than current profitability.

Those expectations are also visible in other data points, including forecasts that earnings are expected to grow very quickly and that return on equity is forecast to reach 23.7% in three years. At the same time, the company’s current return on equity is negative at 93.82% and it remains unprofitable, so the gap between today’s financials and what the market appears to be pricing in is wide.

Compared with both its direct peers on 7.4x P/B and the broader Hong Kong Medical Equipment group on 1.8x, Shanghai MicroPort MedBot’s 49.4x multiple stands out as very expensive. That difference suggests the market is assigning a premium that is far above sector norms and leaves little room for disappointment if the expected improvement in financial performance takes longer than anticipated.

See what the numbers say about this price — find out in our valuation breakdown.

Result: Price to book of 49.4x (OVERVALUED)

However, there are clear risks here, including the company’s continued CN¥478.596m loss and a valuation multiple far above both peers and the wider industry.

Find out about the key risks to this Shanghai MicroPort MedBot (Group) narrative.

Another view, DCF points the other way

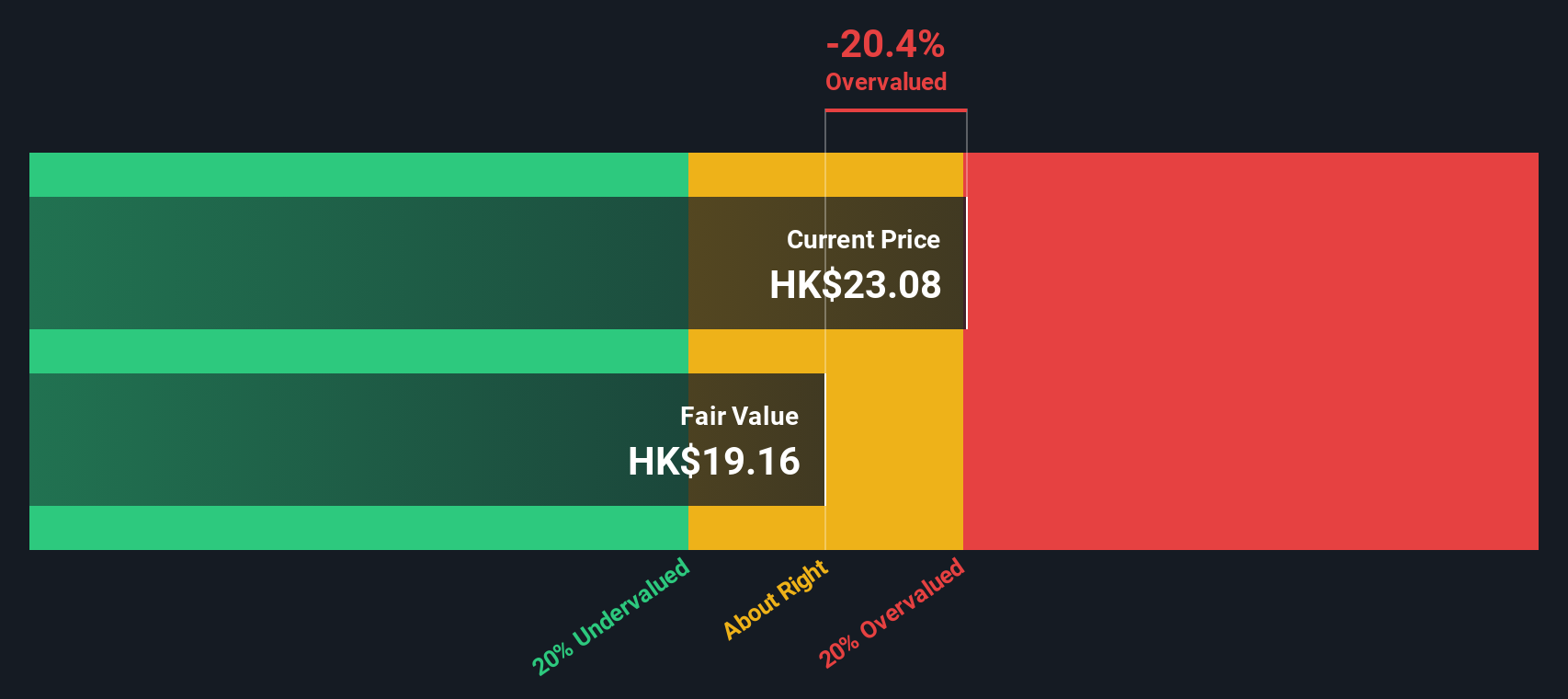

The rich 49.4x P/B might make Shanghai MicroPort MedBot look stretched, but our DCF model actually tells a different story. On that basis, the shares at HK$29.0 are indicated as trading around 22.5% below an estimated fair value of HK$37.44, which paints a more supportive picture.

Both signals cannot be right in the long run. The key question for you is whether book value or long term cash flows will prove to be the stronger anchor for this stock.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Shanghai MicroPort MedBot (Group) for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 231 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Shanghai MicroPort MedBot (Group) Narrative

If you see the numbers differently or prefer to test your own assumptions, you can build a complete view in just a few minutes: Do it your way.

A great starting point for your Shanghai MicroPort MedBot (Group) research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If you are serious about refining your watchlist, now is the moment to cast the net wider with a few focused screeners that surface different kinds of opportunities.

- Spot potential turnarounds by scanning 219 elite penny stocks with strong financials that already show stronger financials than many expect at their price range.

- Hunt for value by checking 231 high quality undervalued stocks where solid fundamentals and pricing leave room for your own judgement.

- Prioritise resilience with 320 resilient stocks with low risk scores so you are not relying on just one stock when conditions become uncomfortable.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English