Asian Growth Stocks With Strong Insider Ownership

As global markets navigate concerns over AI disruption and fluctuating economic indicators, Asia's stock markets have shown resilience, with Japan experiencing significant gains following political developments and China maintaining steady growth despite deflationary pressures. In this climate of uncertainty, investors often look for companies with strong insider ownership as it can signal confidence in the company's prospects by those who know it best.

Top 10 Growth Companies With High Insider Ownership In Asia

| Name | Insider Ownership | Earnings Growth |

| UTI (KOSDAQ:A179900) | 24.7% | 120.7% |

| Suzhou Dongshan Precision Manufacturing (SZSE:002384) | 26.5% | 73.8% |

| Seers Technology (KOSDAQ:A458870) | 32% | 80% |

| Modetour Network (KOSDAQ:A080160) | 12.3% | 41.8% |

| Laopu Gold (SEHK:6181) | 34.7% | 34.9% |

| J&V Energy Technology (TWSE:6869) | 17.9% | 27.1% |

| HUMAN MADE (TSE:456A) | 12.3% | 22.8% |

| Guangzhou Tinci Materials Technology (SZSE:002709) | 39.1% | 83.3% |

| Gold Circuit Electronics (TWSE:2368) | 31.3% | 39.1% |

| Fulin Precision (SZSE:300432) | 10.6% | 80% |

Let's take a closer look at a couple of our picks from the screened companies.

Shenzhen Dobot (SEHK:2432)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Shenzhen Dobot Corp Ltd is an investment holding company involved in the design, development, manufacturing, commercialization, and sale of robots across Mainland China, Hong Kong, Macau, Taiwan, and internationally with a market cap of HK$17.69 billion.

Operations: The company's revenue primarily comes from its Industrial Automation & Controls segment, generating CN¥406.30 million.

Insider Ownership: 18.3%

Revenue Growth Forecast: 32% p.a.

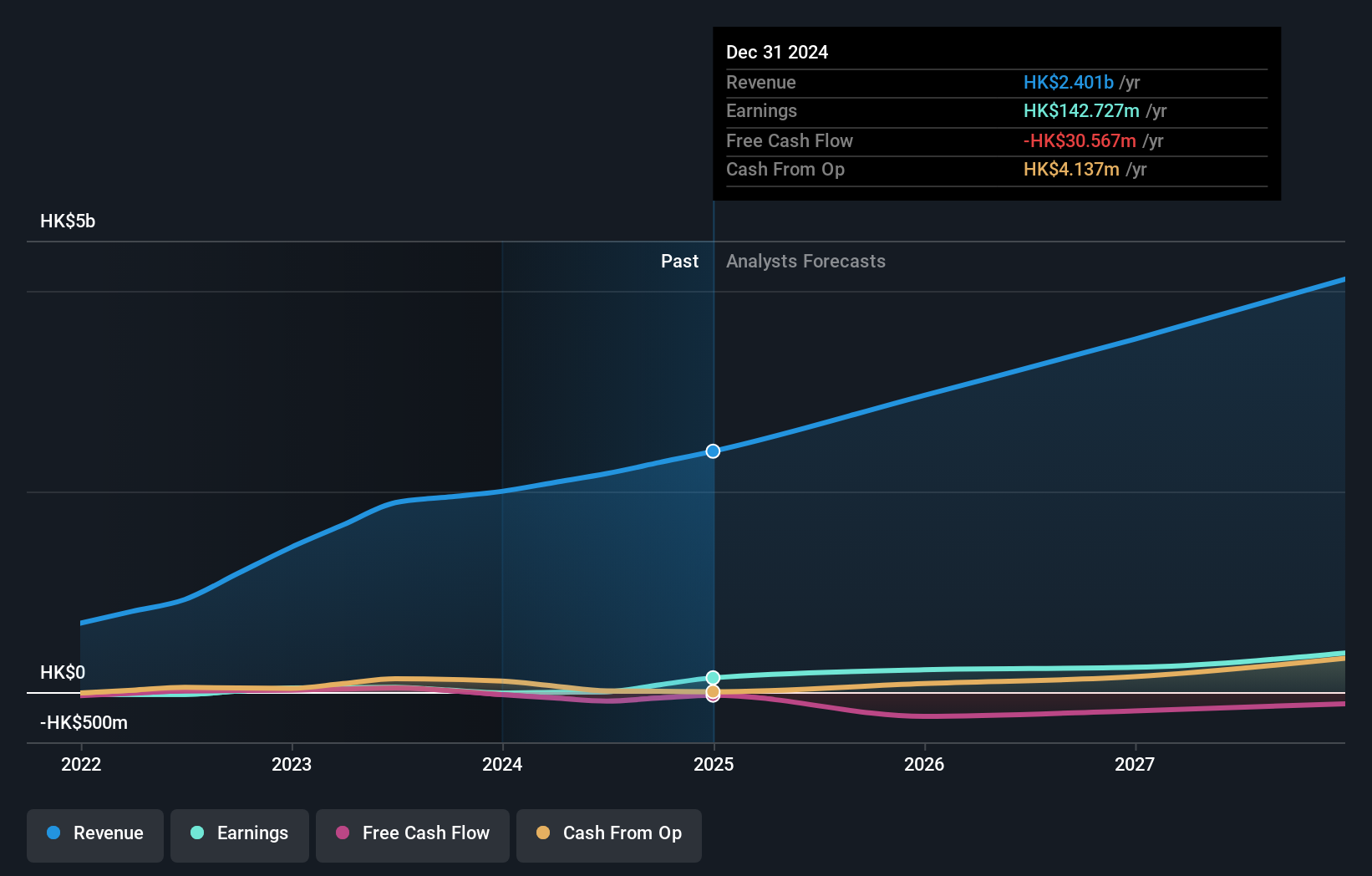

Shenzhen Dobot is poised for significant growth, with revenue expected to increase by 32% annually, surpassing the Hong Kong market's average. Despite substantial insider selling over the past quarter, analysts anticipate a 70.6% rise in stock price. The company plans governance changes and capital adjustments following a recent share placement. Profitability is forecast within three years, although return on equity remains low at 0.4%. Recent meetings indicate active corporate restructuring efforts.

- Click here and access our complete growth analysis report to understand the dynamics of Shenzhen Dobot.

- Insights from our recent valuation report point to the potential overvaluation of Shenzhen Dobot shares in the market.

Vobile Group (SEHK:3738)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Vobile Group Limited is an investment holding company offering software as a service for digital content asset protection and transactions across the United States, Mainland China, and internationally, with a market cap of HK$14.84 billion.

Operations: The company generates revenue from its software as a service offering, amounting to HK$2.68 billion.

Insider Ownership: 20.8%

Revenue Growth Forecast: 23% p.a.

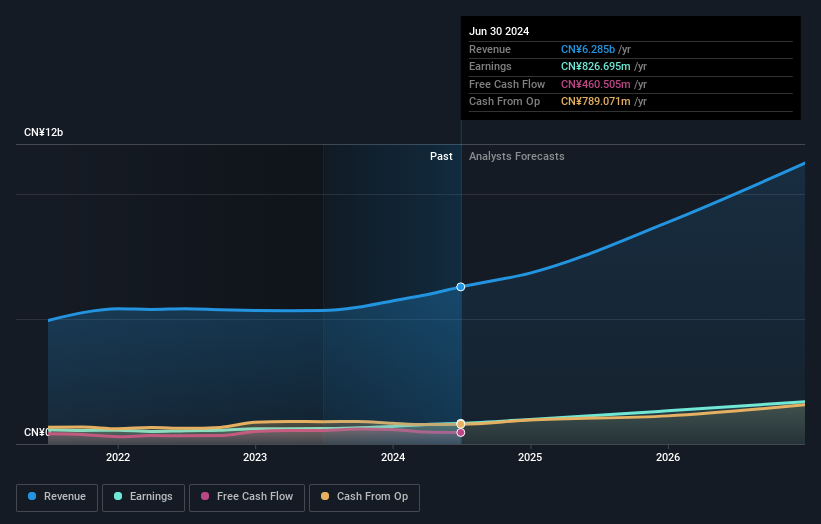

Vobile Group is projected to experience significant growth, with earnings anticipated to rise by 32.7% annually, outpacing the Hong Kong market. Revenue is also expected to grow at a robust 23% per year. Despite recent share price volatility and low forecasted return on equity of 12.8%, analysts predict a potential stock price increase of 26.8%. Insider trading activity has been stable over the past three months, with no substantial buying or selling reported.

- Get an in-depth perspective on Vobile Group's performance by reading our analyst estimates report here.

- According our valuation report, there's an indication that Vobile Group's share price might be on the expensive side.

ShenZhen Woer Heat-Shrinkable MaterialLtd (SZSE:002130)

Simply Wall St Growth Rating: ★★★★★★

Overview: ShenZhen Woer Heat-Shrinkable Material Co., Ltd. and its subsidiaries offer heat shrink products both in China and internationally, with a market cap of CN¥36.66 billion.

Operations: The company generates revenue through its provision of heat shrink products across domestic and international markets.

Insider Ownership: 16.7%

Revenue Growth Forecast: 33.2% p.a.

ShenZhen Woer Heat-Shrinkable Material Ltd. is poised for substantial growth, with earnings expected to increase significantly at 41.7% annually, surpassing the broader Chinese market. Revenue is forecasted to grow robustly at 33.2% per year, also outpacing market averages. Despite a recent follow-on equity offering raising HK$2.81 billion, the stock trades at a favorable price-to-earnings ratio of 37.4x compared to peers and industry benchmarks, indicating good relative value for investors seeking growth opportunities in Asia.

- Dive into the specifics of ShenZhen Woer Heat-Shrinkable MaterialLtd here with our thorough growth forecast report.

- The analysis detailed in our ShenZhen Woer Heat-Shrinkable MaterialLtd valuation report hints at an deflated share price compared to its estimated value.

Seize The Opportunity

- Investigate our full lineup of 558 Fast Growing Asian Companies With High Insider Ownership right here.

- Want To Explore Some Alternatives? This technology could replace computers: discover the 23 stocks are working to make quantum computing a reality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English