Uncovering February 2026's Undiscovered Gems in Asia

As global markets grapple with AI disruption concerns and shifting economic indicators, Asian markets present unique opportunities for investors seeking growth in less saturated sectors. In this dynamic environment, identifying promising small-cap stocks requires a keen eye for companies that demonstrate resilience, innovation, and potential to thrive amid evolving market conditions.

Top 10 Undiscovered Gems With Strong Fundamentals In Asia

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Jiangsu JIXIN Wind Energy Technology | 2.36% | -10.41% | -23.28% | ★★★★★★ |

| Tibet Development | 13.94% | -0.13% | 42.61% | ★★★★★★ |

| Sichuan Haite High-techLtd | 33.85% | 9.98% | -37.61% | ★★★★★★ |

| Sichuan Fulin Transportation Group | 21.07% | 6.25% | 17.69% | ★★★★★☆ |

| Guangzhou Jet Bio-Filtration | 30.44% | -4.59% | -20.48% | ★★★★★☆ |

| ITCENGLOBAL | 63.28% | 18.49% | 32.80% | ★★★★★☆ |

| Zhejiang Chinastars New Materials Group | 42.04% | 1.78% | 6.47% | ★★★★★☆ |

| Anfu CE LINK | 70.49% | 7.92% | -8.47% | ★★★★☆☆ |

| Wuhan Huakang Century Clean Technology | 54.19% | 21.27% | 6.99% | ★★★★☆☆ |

| Tibet TourismLtd | 21.50% | 10.05% | 27.69% | ★★★★☆☆ |

Let's uncover some gems from our specialized screener.

Guanze Medical Information Industry (Holding) (SEHK:2427)

Simply Wall St Value Rating: ★★★★★★

Overview: Guanze Medical Information Industry (Holding) Co., Ltd. is an investment holding company that offers medical imaging solutions in the People’s Republic of China, with a market capitalization of HK$2.84 billion.

Operations: Guanze Medical derives its revenue primarily from the sale of medical imaging film products (CN¥109.88 million) and software (CN¥32.94 million), with a smaller contribution from medical imaging cloud services (CN¥4.74 million).

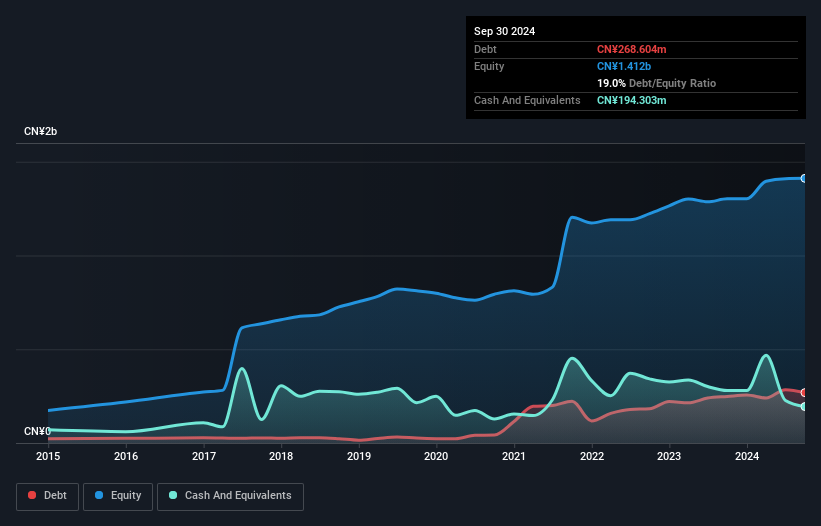

Guanze Medical Information Industry, a smaller player in the healthcare sector, has shown impressive earnings growth of 80.9% over the past year, outpacing the industry average. The company's debt management appears strong with a reduction in its debt-to-equity ratio from 51% to 5.7% over five years and interest payments well covered by EBIT at 35 times. Recent developments include Cheung Chun and Tao Meiying acquiring full ownership through a HKD 62.71 million transaction for an additional stake, reflecting confidence in Guanze's potential despite recent insider selling activities that might raise some eyebrows among investors.

Luyuan Group Holding (Cayman) (SEHK:2451)

Simply Wall St Value Rating: ★★★★★☆

Overview: Luyuan Group Holding (Cayman) Limited focuses on the development, manufacture, and sale of electric vehicles and related accessories in Mainland China, with a market capitalization of approximately HK$6.23 billion.

Operations: Luyuan Group generates revenue primarily from the development, manufacture, and sale of electric vehicles and related accessories, totaling CN¥5.63 billion. The company's financial performance is characterized by a notable focus on its gross profit margin.

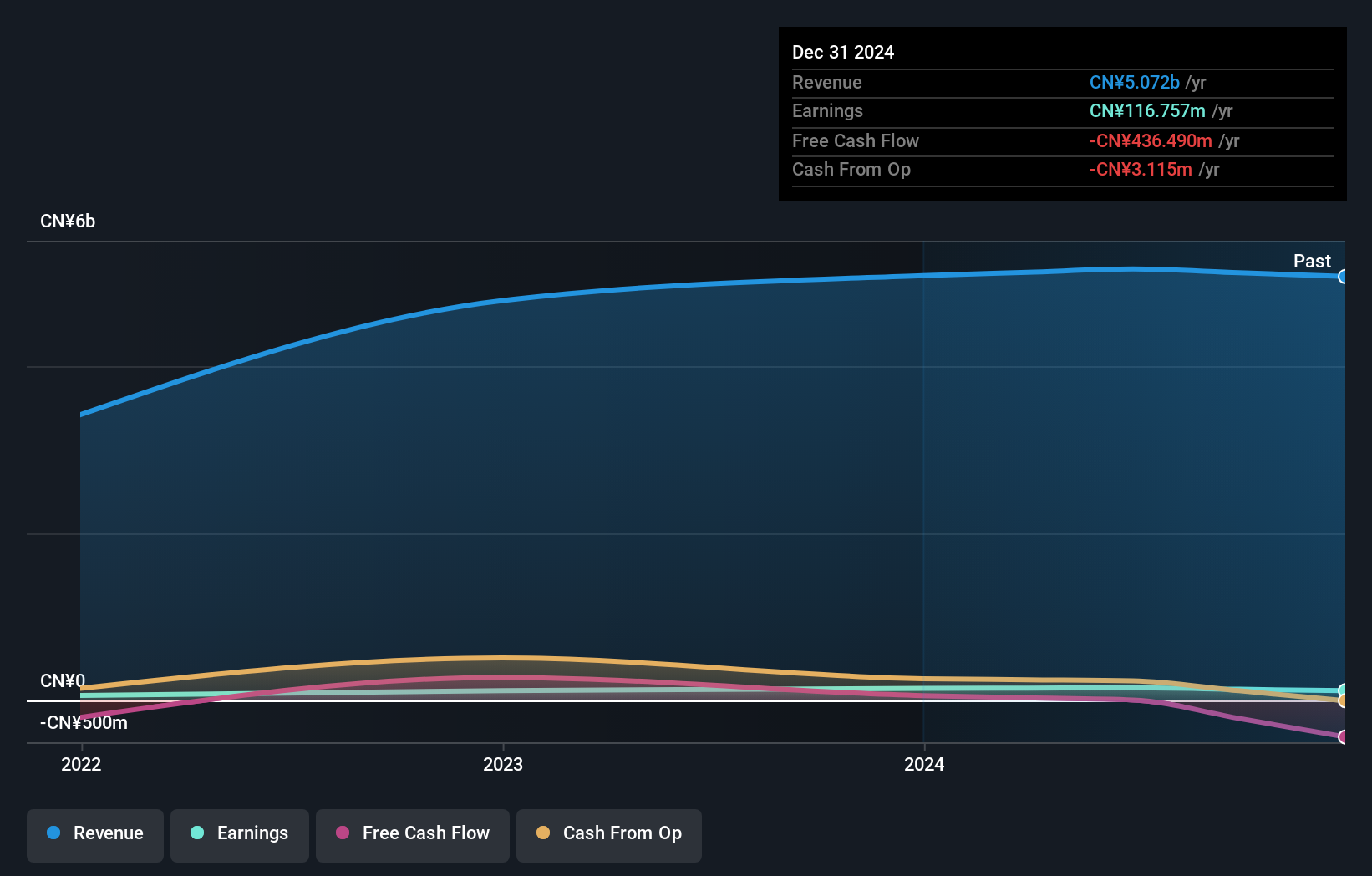

Luyuan Group Holding, a compact player in the auto sector, has shown resilience with earnings climbing 6.3% over the past year, surpassing the industry average of -7.8%. The company is financially sound, boasting more cash than its total debt and maintaining profitability without concerns over its cash runway. Despite a recent dip in levered free cash flow to US$-436 million at the end of 2024, it rebounded to US$379 million by mid-2025. With revenue projected to grow annually by 16.48%, Luyuan seems poised for potential growth within its market niche.

EmbedWay Technologies (Shanghai) (SHSE:603496)

Simply Wall St Value Rating: ★★★★★☆

Overview: EmbedWay Technologies (Shanghai) Corporation provides network visibility, intelligent system platforms, and intelligent computing solutions and services in China, with a market capitalization of approximately CN¥9.67 billion.

Operations: EmbedWay Technologies generates revenue primarily from the manufacturing of computer, communication, and other electronic equipment, amounting to approximately CN¥1.05 billion. The company's financial performance is influenced by its ability to manage costs within this segment.

EmbedWay Technologies, a smaller player in the tech scene, showcases both strengths and challenges. Despite sales slipping to CNY 1.05 billion from CNY 1.12 billion last year, net income rose to CNY 29.69 million from CNY 22.26 million, indicating improved profitability with earnings per share climbing to CNY 0.11 from CNY 0.08. The company is profitable and has more cash than total debt, which suggests financial stability despite a rising debt-to-equity ratio over five years (14% to 21%). Earnings growth at 10% trailed the industry’s pace but holds promise with forecasts of substantial future expansion at over 72%.

Turning Ideas Into Actions

- Dive into all 2501 of the Asian Undiscovered Gems With Strong Fundamentals we have identified here.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English