A Look At New Oriental Education & Technology Group (EDU) Valuation After Recent Mixed Share Price Performance

What recent performance says about New Oriental Education & Technology Group

New Oriental Education & Technology Group (EDU) has drawn investor attention after a period where the stock moved roughly 6% over the past month and about 10% over the past 3 months.

Those returns sit alongside a 1 day decline of about 2.6% and a 7 day decline of roughly 2.3%. This combination can prompt investors to look more closely at the company’s fundamentals and recent financial metrics.

See our latest analysis for New Oriental Education & Technology Group.

At a share price of US$58.70, New Oriental Education & Technology Group sits after a 30 day share price return of 6.36% and a 90 day share price return of 9.84%, while its 1 year total shareholder return of 6.98% contrasts with a much stronger 3 year total shareholder return of 43.43% and a weaker 5 year total shareholder return of 67.51%. This suggests that momentum has cooled recently after a stronger multi year period.

If this mixed performance has you looking for other ideas, you might want to scan our screener of 23 top founder-led companies as a way to uncover fresh opportunities beyond the education sector.

With revenue of US$5,140.63m, net income of US$380.53m and an estimated intrinsic value and analyst target that both sit above the current US$58.70 share price, is there a genuine entry point here, or is the market already pricing in future growth?

Most Popular Narrative: 9% Undervalued

With New Oriental Education & Technology Group’s fair value estimate at US$64.49 against a last close of US$58.70, the most followed narrative frames the current price as leaving some room to the upside while still relying on steady execution rather than aggressive projections.

Strong momentum and high year over year growth in new non academic tutoring and AI powered learning products reflects growing consumer demand for enrichment and personalized education, positioning the company to benefit from continued societal prioritization of premium educational services. This should support long term revenue growth and improve blended margins due to scale and higher retention.

Want to see what sits behind that confidence in higher margins and recurring demand? The narrative leans on measured revenue growth, rising profitability and a future earnings multiple that assumes the market keeps rewarding this business model. The detailed projections join those threads into a single fair value number.

Result: Fair Value of $64.49 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, you still need to weigh risks such as tougher competition in K 12 and non academic segments, as well as potential setbacks in newer tourism and cultural businesses.

Find out about the key risks to this New Oriental Education & Technology Group narrative.

Another angle on valuation

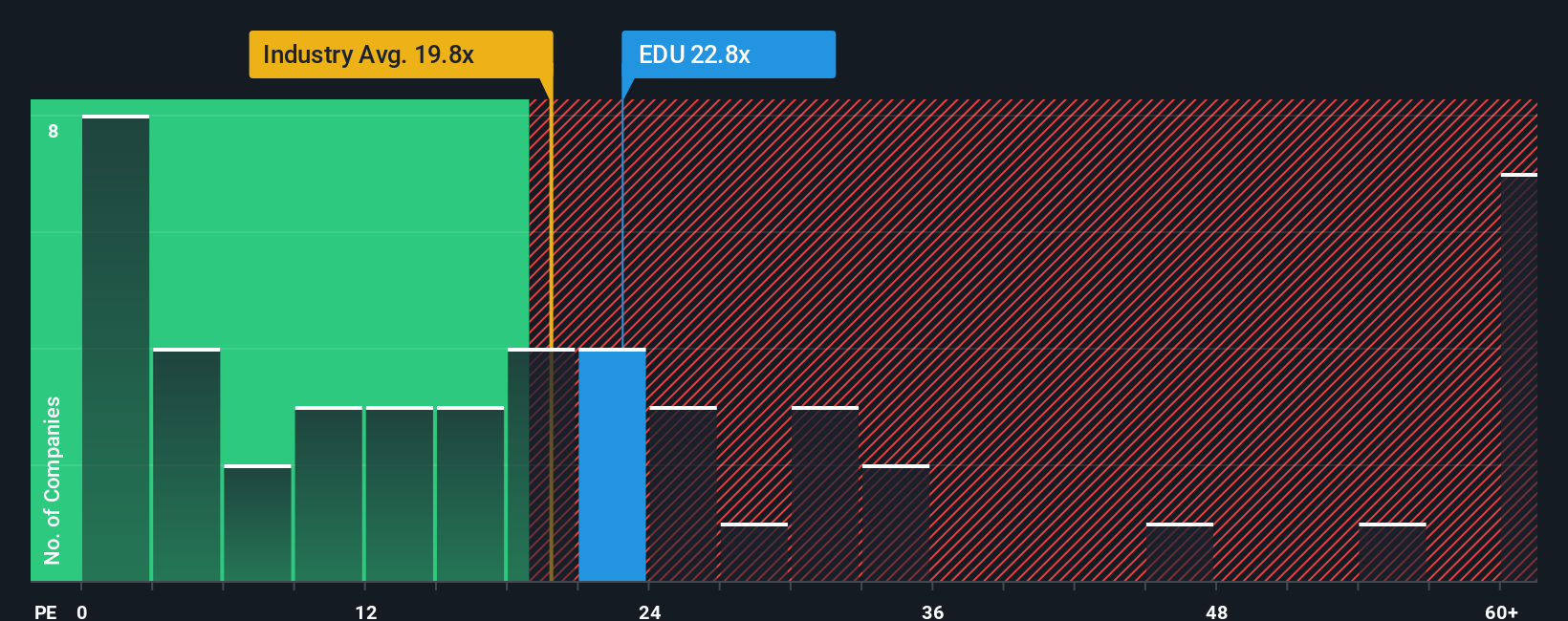

The fair value narrative has New Oriental Education & Technology Group trading about 15.9% below an intrinsic estimate based on future cash flows, which points to an undervalued setup. The market P/E of 24.5x, however, is higher than the US Consumer Services average of 17.7x and the 20.7x peer average, even if it is close to the 24.9x fair ratio. That mix of discount on one model and premium on earnings multiples raises a simple question: which signal do you think matters more for your own risk tolerance?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own New Oriental Education & Technology Group Narrative

If this story does not quite match your view, or you would rather rely on your own research, you can review the same data, shape your own thesis and Do it your way in just a few minutes.

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding New Oriental Education & Technology Group.

Looking for more investment ideas?

If you stop with just one company, you will miss plenty of other potential opportunities, so put the same curiosity to work across a broader watchlist right now.

- Spot potential value candidates early by scanning our 54 high quality undervalued stocks and see which companies the numbers suggest could be trading below their fundamentals.

- Strengthen your downside protection by checking the solid balance sheet and fundamentals stocks screener (44 results) that highlight businesses with support from cash flows and resilient financial positions.

- Turn your watchlist into an income shortlist by reviewing the 13 dividend fortresses that focus on higher yielding companies with an emphasis on stability.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English