Assessing Sinofert Holdings (SEHK:297) Valuation After The Chairman Transition To Zhang Xuegong

Sinofert Holdings (SEHK:297) has announced a leadership reshuffle, with long serving chairman Su Fu stepping down and industry veteran Zhang Xuegong becoming chairman and executive director. This governance change is one that investors will likely watch closely.

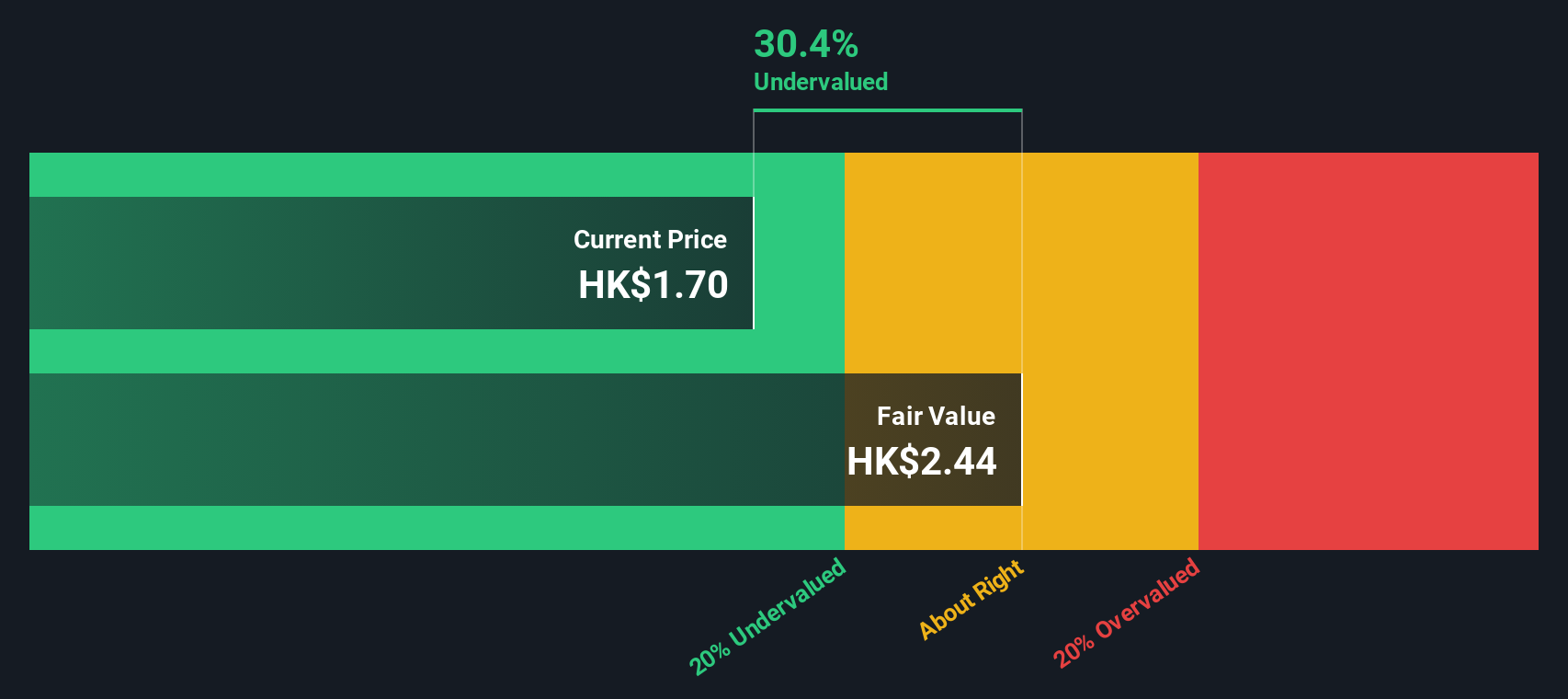

See our latest analysis for Sinofert Holdings.

At a share price of HK$1.62, Sinofert Holdings has seen a 6.58% 1 month share price return and a 4.52% year to date share price return. Its 1 year total shareholder return of 61.09% and 3 year total shareholder return of 95.66% point to strong longer term momentum that recent leadership news may now test or reinforce.

If this leadership change has you thinking about where capital could work hardest next, it might be worth scanning our 104 top founder-led companies as a fresh source of ideas.

With Sinofert trading at HK$1.62, which is only a small discount to the latest analyst target but shows a much larger gap to one intrinsic value estimate, you have to ask whether there is still mispricing here or if the market is already baking in future growth.

Price to Earnings of 9x: Is it justified?

On a P/E of 9x, Sinofert Holdings is being priced below both peers and the wider Hong Kong chemicals industry, while still sitting close to the latest analyst target.

The P/E ratio compares the current share price with earnings per share, so a lower P/E can mean the market is placing a lower value on each unit of profit. For Sinofert, that 9x multiple sits below the peer average of 13.6x and slightly below the Hong Kong chemicals industry average of 9.5x, which suggests the market is not paying up for its recent earnings profile.

In contrast, our fair P/E estimate of 15x indicates a higher level the valuation could gravitate toward if earnings quality and growth trends stay aligned with what the SWS fair ratio work implies. With earnings having grown over the past year and forecast to grow further, the current 9x P/E looks conservative compared to both industry norms and this fair ratio benchmark.

Explore the SWS fair ratio for Sinofert Holdings

Result: Price-to-Earnings of 9x (UNDERVALUED)

However, you still need to factor in execution risk from the leadership reshuffle, as well as the possibility that current P/E discounts reflect concerns about future earnings resilience.

Find out about the key risks to this Sinofert Holdings narrative.

Another View: What Does The Cash Flow Say?

While the 9x P/E hints at value, our DCF model presents an even lower valuation, with Sinofert at HK$1.62 compared with an estimated future cash flow value of HK$2.72. That gap suggests the market may be heavily discounting execution and earnings risks, raising the question of what it might be pricing in that you are not considering.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Sinofert Holdings for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 223 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

The mix of upside and caution in this story is pretty clear. If you want to move quickly and shape your own view, it is worth weighing the 4 key rewards and 1 important warning sign before deciding what this leadership change and valuation gap really mean for you.

Looking for more investment ideas?

If you are weighing what to do next, do not stop with just one company. Use a few targeted stock lists to spot opportunities that fit your style.

- Spot potential value early by scanning screener containing 572 high quality undiscovered gems that combine solid fundamentals with under the radar profiles.

- Focus on resilience first and check out 322 resilient stocks with low risk scores that score well on our risk filters before you commit fresh capital.

- Aim for quality at a sensible entry point with 223 high quality undervalued stocks that pair stronger balance sheets and cash flows with lower valuations.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English