Carriage Services’s (NYSE:CSV) Q4 CY2025 Sales Top Estimates

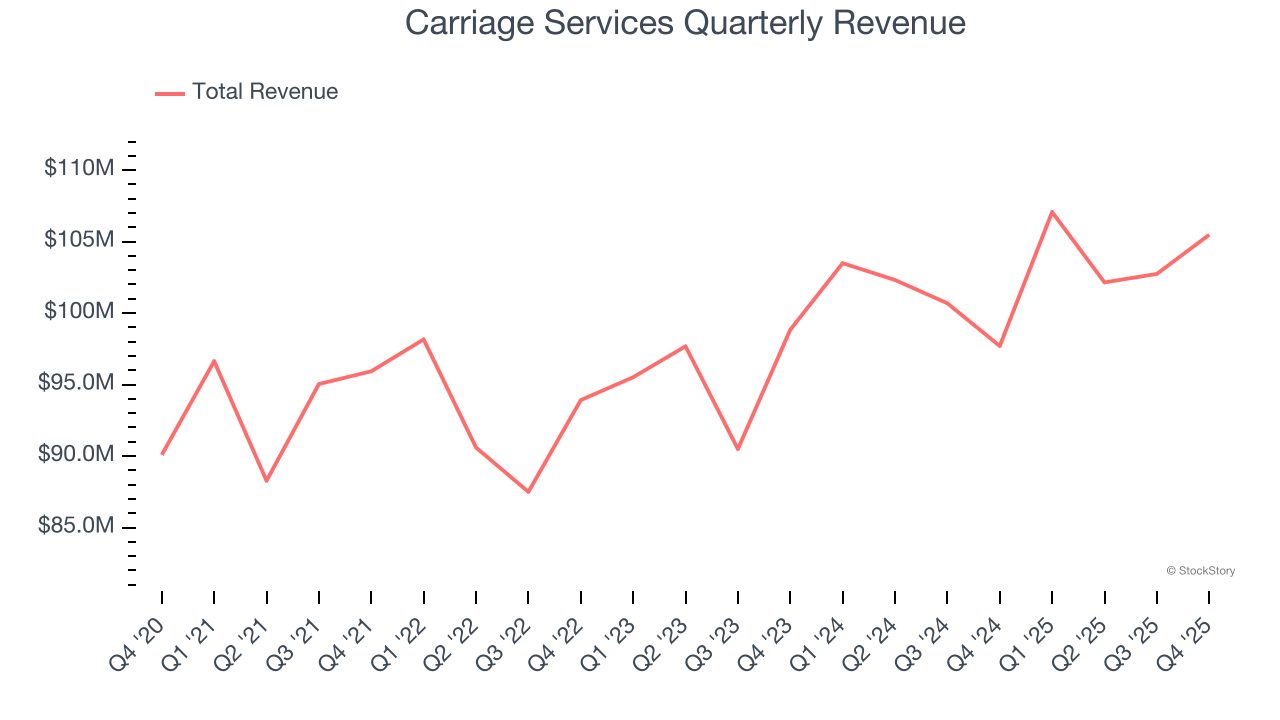

Funeral services company Carriage Services (NYSE:CSV) reported revenue ahead of Wall Street’s expectations in Q4 CY2025, with sales up 8% year on year to $105.5 million. The company’s full-year revenue guidance of $445 million at the midpoint came in 3.7% above analysts’ estimates. Its non-GAAP profit of $0.75 per share was 7.2% below analysts’ consensus estimates.

Is now the time to buy Carriage Services? Find out by accessing our full research report, it’s free.

Carriage Services (CSV) Q4 CY2025 Highlights:

- Revenue: $105.5 million vs analyst estimates of $103.6 million (8% year-on-year growth, 1.8% beat)

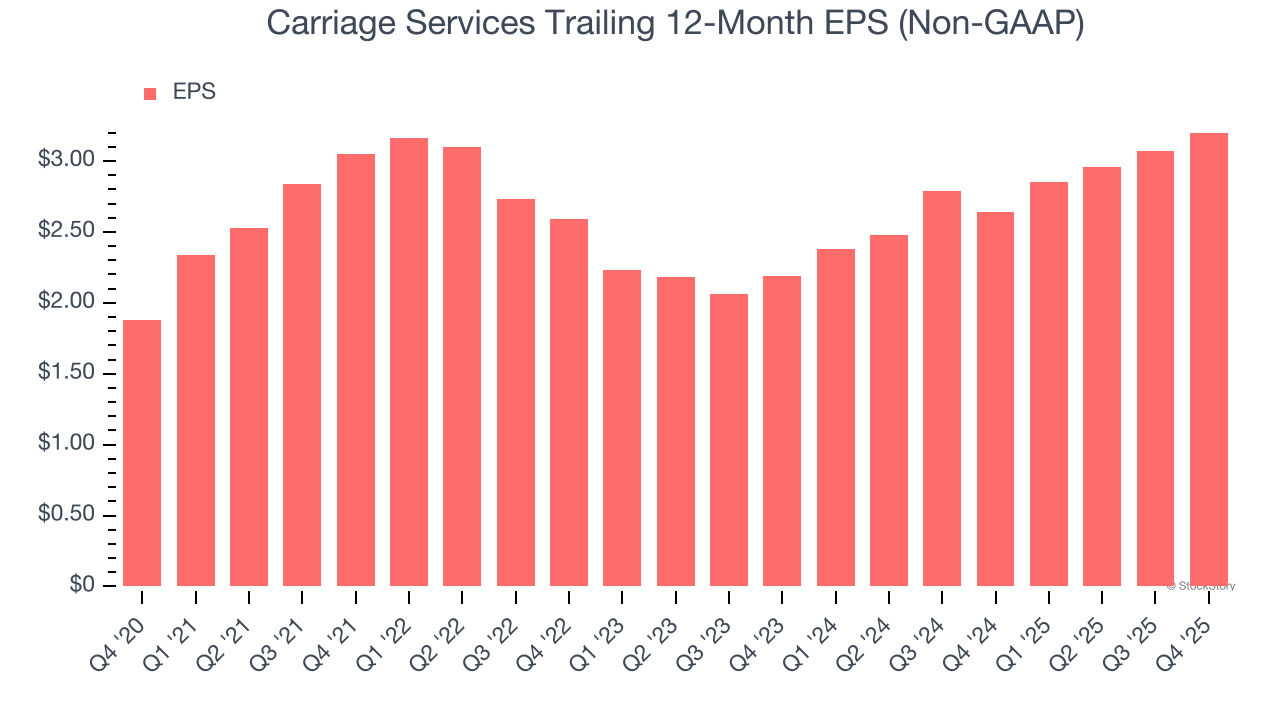

- Adjusted EPS: $0.75 vs analyst expectations of $0.81 (7.2% miss)

- Adjusted EBITDA: $32.5 million vs analyst estimates of $33.03 million (30.8% margin, 1.6% miss)

- Adjusted EPS guidance for the upcoming financial year 2026 is $3.45 at the midpoint

- EBITDA guidance for the upcoming financial year 2026 is $137.5 million at the midpoint, in line with analyst expectations

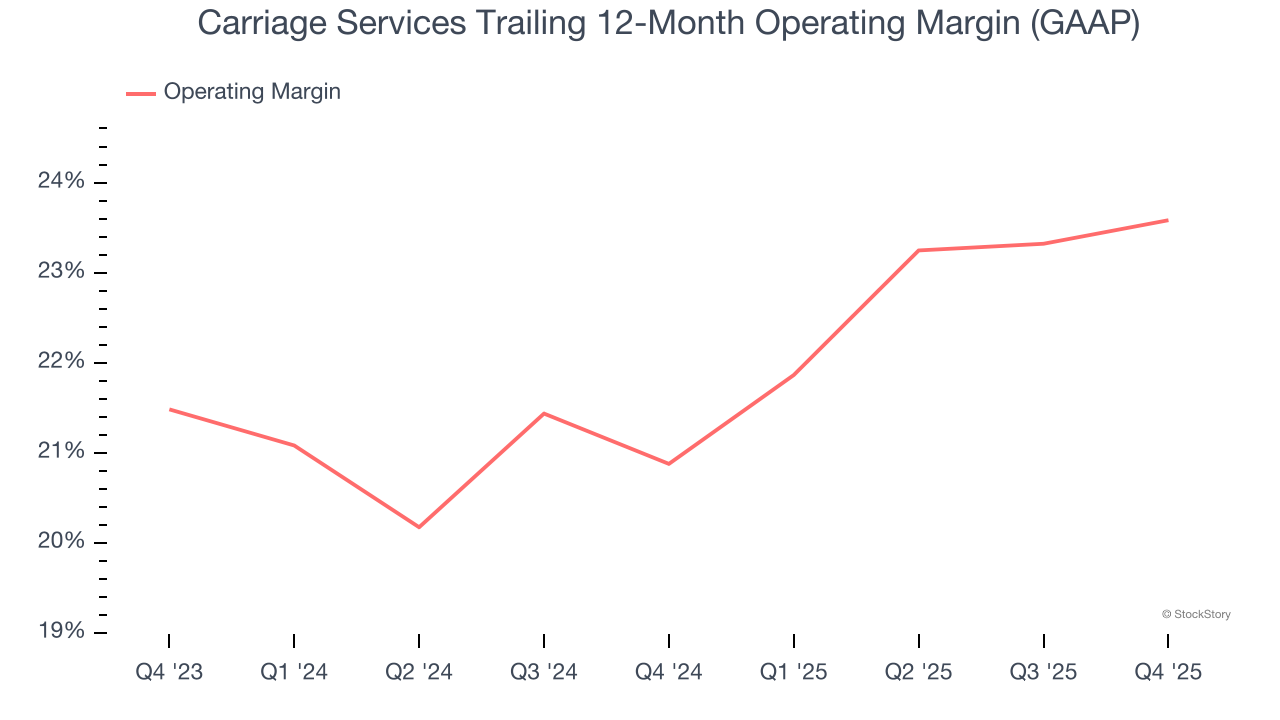

- Operating Margin: 23.3%, up from 22.2% in the same quarter last year

- Free Cash Flow Margin: 5.9%, down from 9.1% in the same quarter last year

- Market Capitalization: $701 million

Carlos Quezada, Vice Chairman and CEO, stated, "We are very pleased with our 2025 fourth quarter and full year performance. In the fourth quarter, total funeral operating revenue increased by 9.6%, primarily reflecting growth in funeral operating contract volume, while total cemetery operating revenue grew 18.4%, primarily driven by a strong performance in preneed cemetery sales production. Operating income grew 16.8% and adjusted consolidated EBITDA grew by 11.0%, while adjusted consolidated EBITDA margin grew by 80 bps to 30.8%, all versus the same quarter last year.

Company Overview

Established in 1991, Carriage Services (NYSE:CSV) is a provider of funeral and cemetery services in the United States.

Revenue Growth

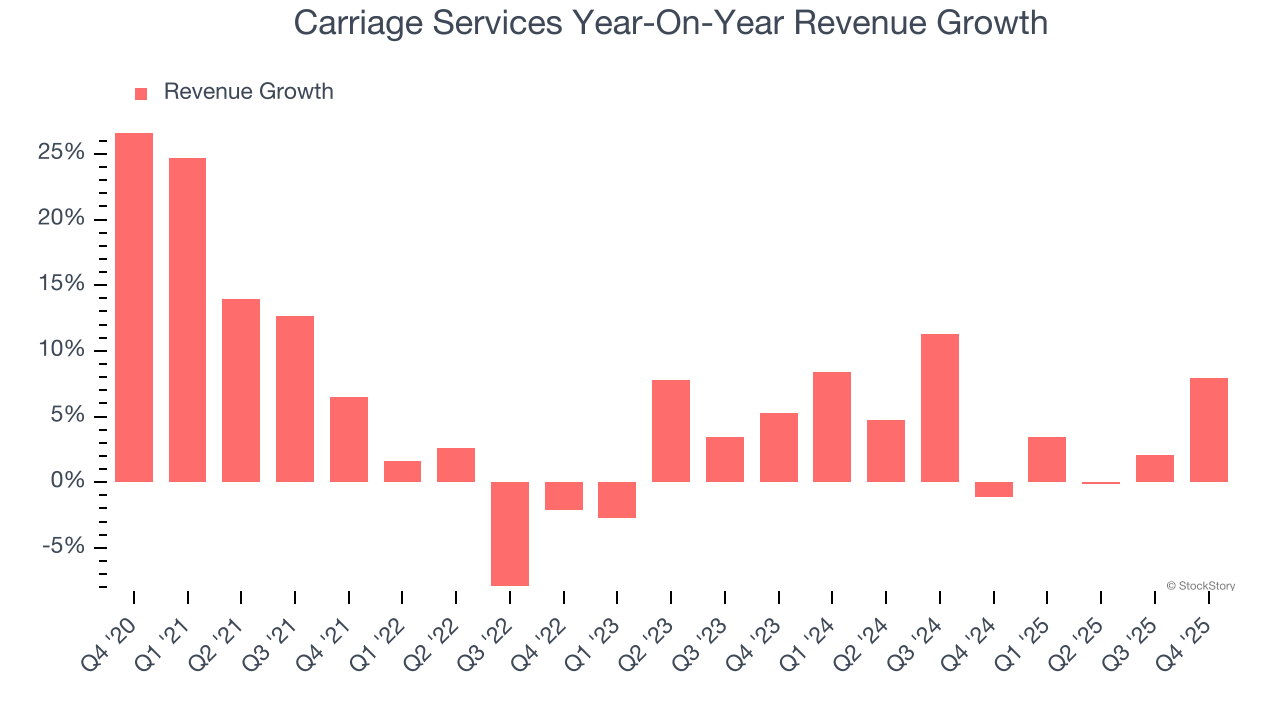

A company’s long-term sales performance can indicate its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Regrettably, Carriage Services’s sales grew at a weak 4.8% compounded annual growth rate over the last five years. This was below our standard for the consumer discretionary sector and is a rough starting point for our analysis.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Carriage Services’s annualized revenue growth of 4.5% over the last two years aligns with its five-year trend, suggesting its demand was consistently weak.

This quarter, Carriage Services reported year-on-year revenue growth of 8%, and its $105.5 million of revenue exceeded Wall Street’s estimates by 1.8%.

Looking ahead, sell-side analysts expect revenue to grow 3.8% over the next 12 months, similar to its two-year rate. This projection is underwhelming and indicates its newer products and services will not lead to better top-line performance yet.

Microsoft, Alphabet, Coca-Cola, Monster Beverage—all began as under-the-radar growth stories riding a massive trend. We’ve identified the next one: a profitable AI semiconductor play Wall Street is still overlooking. Go here for access to our full report.

Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Carriage Services’s operating margin has been trending up over the last 12 months and averaged 22.3% over the last two years. The company’s higher efficiency is a breath of fresh air, but its suboptimal cost structure means it still sports lousy profitability for a consumer discretionary business.

In Q4, Carriage Services generated an operating margin profit margin of 23.3%, up 1.1 percentage points year on year. This increase was a welcome development and shows it was more efficient.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Carriage Services’s EPS grew at a weak 11.2% compounded annual growth rate over the last five years. This performance was better than its flat revenue but doesn’t tell us much about its business quality because its operating margin didn’t improve.

In Q4, Carriage Services reported adjusted EPS of $0.75, up from $0.62 in the same quarter last year. Despite growing year on year, this print missed analysts’ estimates. Over the next 12 months, Wall Street expects Carriage Services’s full-year EPS of $3.20 to grow 7.4%.

Key Takeaways from Carriage Services’s Q4 Results

We were impressed by Carriage Services’s optimistic full-year revenue guidance, which blew past analysts’ expectations. We were also happy its revenue outperformed Wall Street’s estimates. On the other hand, its EBITDA and EPS both missed. Overall, this print was mixed. The market seemed to be hoping for more, and the stock traded down 2.2% to $43.22 immediately after reporting.

Big picture, is Carriage Services a buy here and now? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English