Is Perella Weinberg (PWP) Quietly Redefining Earnings Resilience Despite a Modest Revenue Decline?

- Perella Weinberg Partners recently reported quarterly revenues of US$219.2 million, a 2.9% year-on-year decline that still exceeded analyst estimates by a very large margin, alongside an earnings beat.

- The results highlight how the firm’s operational execution outpaced expectations even as headline revenue slipped, offering a more nuanced picture of performance for investors.

- Next, we’ll examine how this better-than-expected revenue performance shapes Perella Weinberg Partners’ investment narrative and its perceived earnings resilience.

We've uncovered the 15 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

What Is Perella Weinberg Partners' Investment Narrative?

To own Perella Weinberg Partners, you have to believe in the durability of its advisory franchise, its ability to turn fee volatility into consistent profitability, and the discipline behind its capital returns. The latest quarter, with US$219.2 million in revenue modestly lower year on year but far ahead of expectations, reinforces the near term catalyst that matters most: evidence that the firm can beat a conservative profit bar even when activity is mixed. That sits alongside a still-young management team, a relatively high earnings multiple, and recent share price weakness despite an earnings beat, which together sharpen the risk that sentiment can swing quickly if deal flow or margins soften. For now, the new results look more sentiment reset than thesis changer.

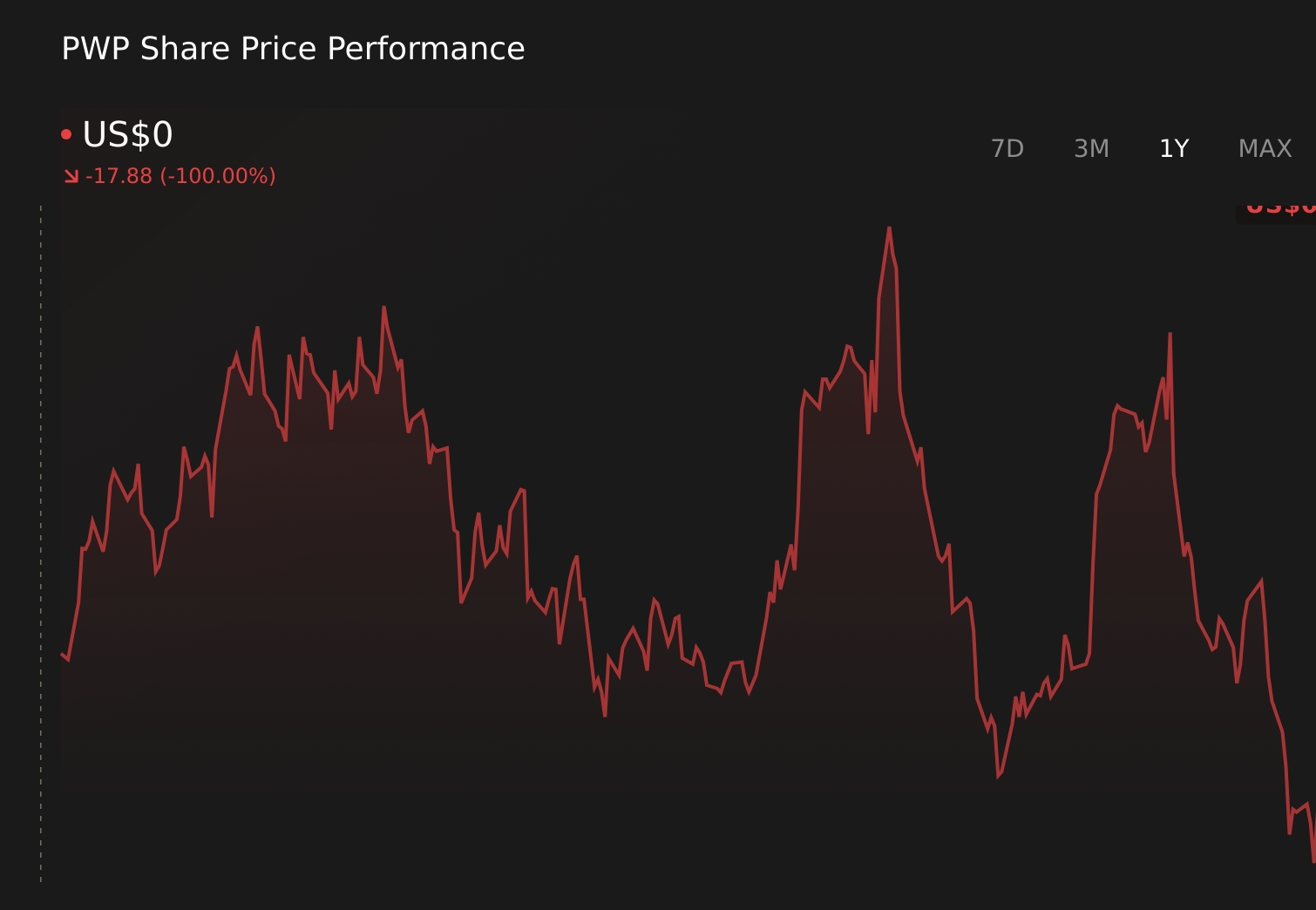

However, one key risk around valuation and execution is easy to miss at first glance. Perella Weinberg Partners' share price has been on the slide but might be dropping deeper into value territory. Find out whether it's a bargain at this price.Exploring Other Perspectives

Explore another fair value estimate on Perella Weinberg Partners - why the stock might be worth just $25.62!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Perella Weinberg Partners research is our analysis highlighting 2 key rewards that could impact your investment decision.

- Our free Perella Weinberg Partners research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Perella Weinberg Partners' overall financial health at a glance.

Contemplating Other Strategies?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- The future of work is here. Discover the 30 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Uncover the next big thing with 31 elite penny stocks that balance risk and reward.

- The latest GPUs need a type of rare earth metal called Dysprosium and there are only 31 companies in the world exploring or producing it. Find the list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Contact Us

Contact Number :+852 3852 8500Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English